The annual returns advertised on DeFi platforms turn heads: 8%, 15%, sometimes 50% or more. Faced with savings accounts struggling to exceed 3%, the temptation is strong. Yet behind these figures lies a far more nuanced reality than the colorful interfaces suggest.

Passive income on crypto-assets is no miracle investment. It's a set of strategies, each with its own mechanics, specific risks, and operational constraints. Understanding these elements allows you to build a coherent approach, aligned with your wealth objectives and optimize your blockchain passive income strategy.

The economic fundamentals of crypto-asset passive income

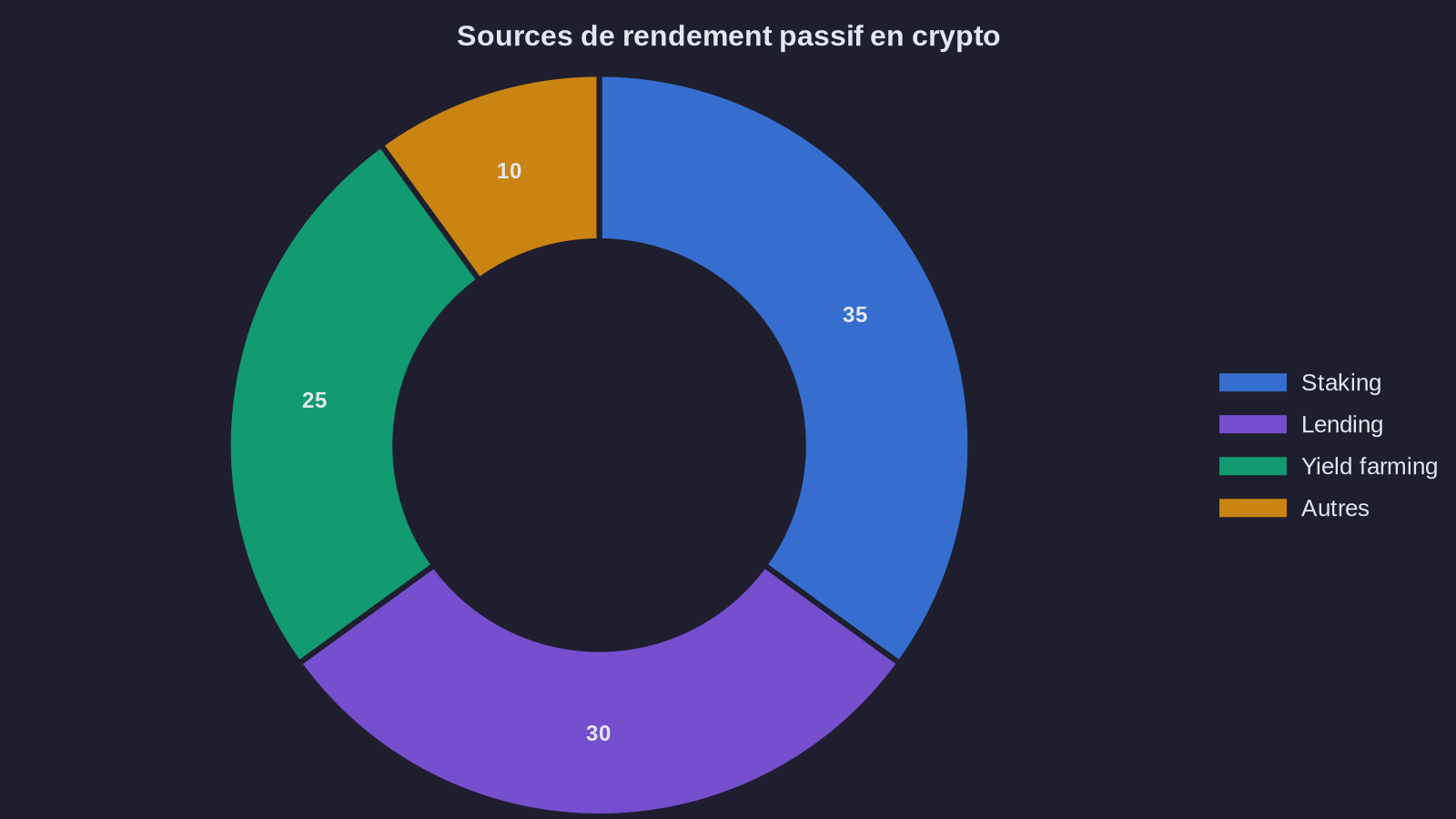

Contrary to popular belief, crypto returns don't appear out of thin air. They correspond to precise economic functions within blockchain protocols. Staking, for example, rewards the validation of transactions and network security. Lending compensates for the counterparty risk assumed by the lender. Yield farming captures a portion of the exchange fees generated by liquidity pools.

This distinction is fundamental. It allows you to identify the true source of returns and, by extension, the associated risks. An 8% rate on Ethereum staking corresponds to network inflation and transaction fees distributed to validators. A 15% rate on a stablecoin loan reflects strong borrowing demand, often linked to leveraged trading strategies. A 50% rate on an exotic liquidity pool typically signals a combination of temporary protocol incentives and considerable volatility in the underlying assets.

Experienced investors always start with this question: where does this return come from? The answer determines the sustainability of the strategy and its risk profile.

Crypto staking returns: compensating for network security

Staking represents the strategy most similar to a traditional investment, at least in its logic. You lock up tokens to participate in validating transactions on a Proof-of-Stake blockchain, and you receive rewards in the form of newly issued tokens and transaction fees.

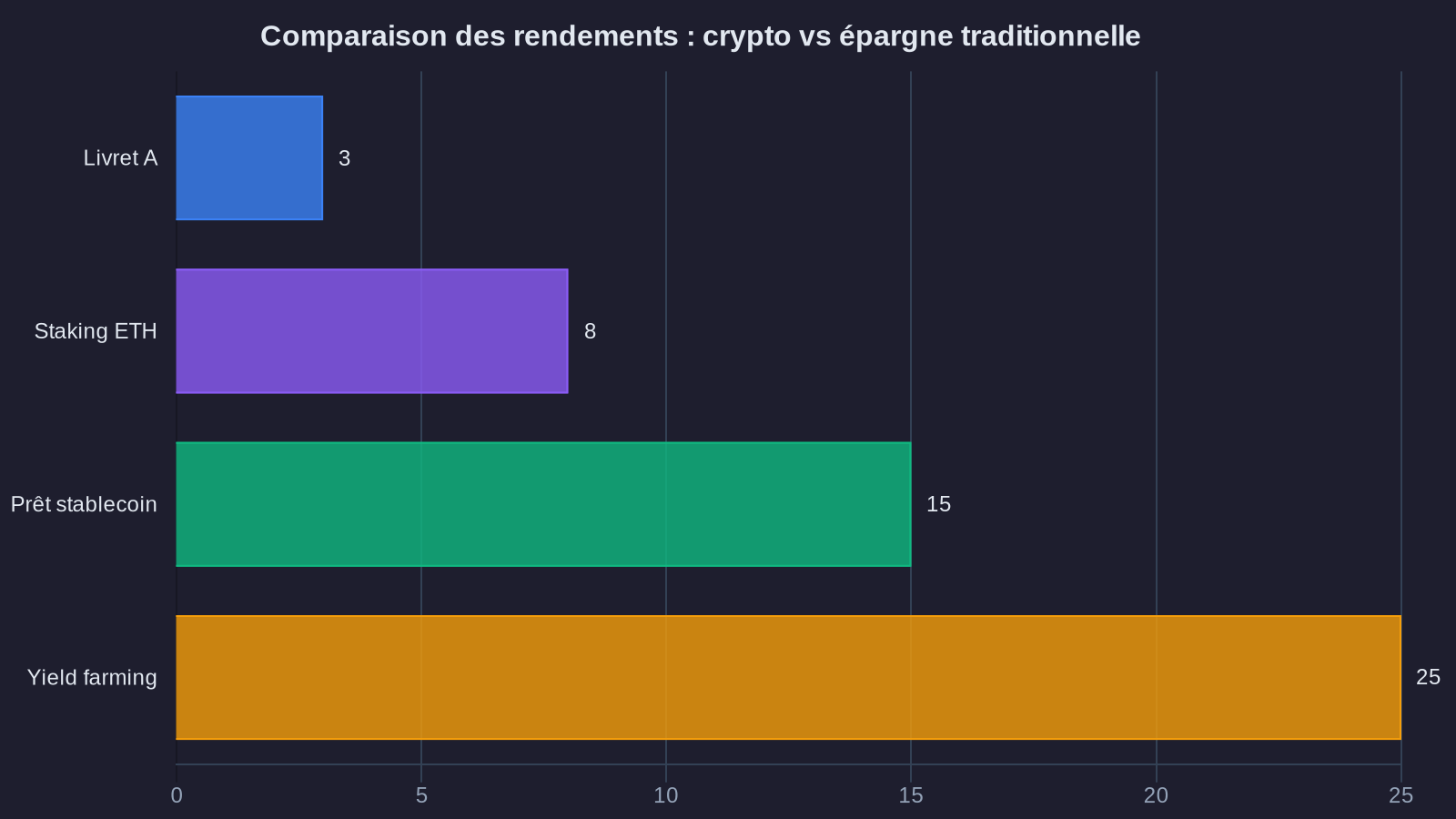

Returns vary considerably across protocols. Ethereum currently shows annual rates between 3% and 4%, reflecting the maturity of the network and its broad adoption. Newer or less established blockchains often offer higher returns, sometimes exceeding 10%, to attract validators and secure their network.

This variance reflects a clear risk-return equation. A high rate on an emerging blockchain may signal the risk of token devaluation through excessive inflation, uncertain protocol adoption, or undiscovered technical vulnerabilities. Conversely, Ethereum's more modest returns come with substantial market capitalization, a developed ecosystem, and thorough security audits.

Staking also involves specific operational constraints. Staked tokens are generally locked for a defined period during which you cannot sell or transfer them. This temporary illiquidity exposes you to market risk: if the token loses 30% of its value during the lock-up period, staking returns obviously won't offset this capital loss.

Some protocols offer liquid staking solutions that circumvent this constraint by issuing tokens representing the staked position, freely exchangeable. Lido, for example, issues stETH in exchange for staked ETH. This innovation adds, however, another layer of complexity and additional risk: the smart contract risk of the liquid staking protocol itself, and the depeg risk between the derivative token and the underlying asset, as observed during certain market stress periods.

Lending and borrowing: DeFi returns in action

Decentralized lending protocols like Aave or Compound allow you to lend your crypto-assets to borrowers in exchange for interest. The rate you receive depends directly on the supply and demand for each asset: the stronger the borrowing demand, the higher the return rate for lenders.

This market mechanism creates yield volatility that investors must account for in their planning. The rate on a USDC loan can swing between 2% and 15% depending on market phases. During bull markets, borrowing demand explodes, driven by traders wanting to increase their exposure with leverage. During bear markets, this demand collapses and rates plummet.

Lending in stablecoins often represents the preferred entry point for investors who want to avoid crypto-asset volatility while generating returns. You maintain exposure to the dollar with a return generally superior to traditional money market investments. However, this approach is not risk-free.

Smart contract risk remains the most critical. A bug in the protocol's code, a security vulnerability exploited by an attacker, can result in total loss of deposited funds. Established protocols have generally undergone multiple audits and are covered by decentralized insurance, but zero risk doesn't exist. Savvy investors limit their exposure to each individual protocol and favor those with a proven track record over several years.

Counterparty risk, though different from traditional finance, also exists. In decentralized lending protocols, borrowers must provide substantial collateralization, typically between 120% and 200% of the borrowed amount. If this collateral's value drops, the protocol automatically liquidates the position to protect lenders. This mechanism works well in theory, but massive liquidations during sharp market movements can create situations where lenders are not fully repaid.

Yield farming strategy: advanced opportunity or unnecessary complexity?

Yield farming pushes the passive income logic to its limits. It involves providing liquidity to decentralized exchanges (DEXs) by depositing token pairs into pools. In return, you receive a share of the exchange fees generated by these platforms, often supplemented by governance tokens from the protocol.

Displayed returns can reach impressive levels, sometimes exceeding 100% annually. These figures, however, require rigorous analysis. A significant portion often comes from the issuance of governance tokens whose valuation is uncertain and liquidity limited. Calculating real returns requires distinguishing fees actually captured from token incentives, then evaluating the ability to convert these tokens into real value.

Yield farming also introduces a specific risk not encountered in other strategies: impermanent loss. When you provide liquidity on a pair like ETH/USDC, you're exposed to relative price variations between the two assets. If ETH appreciates 50% against the dollar, the pool mechanism automatically rebalances the position by selling ETH and buying USDC. When you withdraw, you end up with fewer ETH than you initially deposited. This loss is only permanent if you withdraw your liquidity, hence the term impermanent, but it can be substantial.

For yield farming to be profitable, the fees captured and tokens received must compensate for this potential loss. This equation generally works well on stable or correlated pairs (ETH/wstETH for example), where relative variations remain limited. It becomes far riskier on volatile pairs, where impermanent loss can significantly exceed displayed returns.

Yield farming strategies also require active management. Returns fluctuate based on exchange volumes, the issuance of new incentive tokens, and the evolution of competing pools. What offered 40% returns last week might drop to 8% today if many participants have joined the pool. This dynamic transforms yield farming into a time-consuming activity, poorly compatible with a truly passive approach.

Building a coherent crypto-asset passive income strategy

Faced with this diversity of options, how do you structure a rational approach? Experience shows that investors who achieve the best results follow a few guiding principles.

Diversifying across protocols limits smart contract risk. Rather than concentrating €100,000 on a single lending protocol, you spread it across three or four established ones. This approach reduces exposure to a single technical failure without significantly diluting returns.

Progressive allocation allows you to test mechanisms before committing substantial amounts. Starting with 5% of your crypto allocation on a new strategy lets you understand operational subtleties, evaluate return stability, and detect any issues before they significantly impact your wealth.

Consistency with your risk tolerance remains fundamental. An investor who loses sleep when their portfolio moves 10% probably has no business in yield farming on volatile tokens. Conversely, staking Ethereum or lending stablecoins on established protocols can naturally integrate into a diversified wealth strategy.

Tax considerations also merit attention. In most jurisdictions, generated returns are taxable. Yield farming strategies, with their multiple transactions and governance tokens, create considerable administrative complexity when filing taxes. This practical dimension influences strategy choice: sometimes a slightly lower return that's simpler to manage tax-wise proves more advantageous after taxes and time spent.

Beyond displayed returns

Passive income strategies on crypto-assets represent a real opportunity for investors who take the time to understand their mechanisms. They are neither a shortcut to rapid wealth creation nor a simple substitute for traditional investments.

Each strategy corresponds to a precise economic function, with its own risks and operational constraints. Staking offers exposure to blockchain protocol growth while contributing to their security. Lending generates returns on stablecoins with limited volatility, provided you remain vigilant about which protocols you use. Yield farming opens prospects for higher returns at the cost of increased complexity and active management requirements.

The most coherent approach is to align these strategies with your overall wealth objectives, your risk tolerance, and your appetite for active management. Rather than chasing the highest returns, you build a thoughtful allocation combining different strategies based on their risk-return profile and complementarity.

In an environment where disconnected promises abound, this analytical rigor makes all the difference between a sustainable strategy and a costly disappointment.