Every year, thousands of European retirees make the leap: they leave their home country to settle in more tax-friendly jurisdictions. Portugal, Dubai, Monaco, Switzerland… destinations vary, but the motivation often remains the same. Optimize your tax situation to protect your assets at a time when income streams are stabilizing.

For those holding crypto assets, this reflection on protecting retirement savings and changing tax residence takes on an additional dimension. Potential capital gains can be substantial, and applicable tax regimes vary dramatically from one country to another. Some countries tax heavily, others apply preferential treatment, and a few don't tax capital gains on digital assets at all. This wealth optimization, however, requires a nuanced understanding of international tax mechanisms.

But beware: what looks like an obvious optimization on paper can turn into a tax trap if the rules aren't perfectly understood. Tax residency isn't declared—it's proven. And tax authorities, increasingly sophisticated, now scrutinize these movements closely.

The 183-day rule: a simple principle, complex applications

You often hear this magic formula: "You just need to spend more than 183 days a year in a country to become tax resident there." It's both true and dangerously oversimplified. The 183-day rule sits at the heart of many tax residence change strategies, but its practical application is far more complex than it appears.

The 183-day principle does exist in most international tax conventions. If you reside more than half the year in a country, you're generally considered tax resident there. But this quantitative criterion is only one element considered. Authorities also examine your "center of vital interests": where your family is, where your principal real estate is located, where your income comes from, and whether you carry out professional activity there.

Let's take a concrete example. A French retiree holds a substantial crypto portfolio, acquired several years ago. He decides to move to Portugal, where the Non-Habitual Resident (NHR) regime can offer an exemption on certain foreign income for ten years. He rents an apartment in Lisbon, spends eight months a year there, and obtains his NIF (Portuguese tax number). Everything appears to be in order.

Except his wife remains in France with their grandchildren. Their main bank accounts are French. Their secondary residence—their real family home—is in Brittany. If the French tax authority decides to challenge his Portuguese residence, it has solid arguments. The debate won't focus solely on the number of days, but on his entire personal situation.

Crypto assets and tax mobility: a combination to handle with care

Crypto assets further complicate the equation. Their dematerialized nature creates an illusion: that they naturally escape tax authorities' radar. This is increasingly untrue, particularly with new regulations transforming tax treatment across residence jurisdictions.

Since 2023, the European DAC8 directive requires exchange platforms to automatically report transaction information on their customers' activities to tax authorities. If you're a French resident and trading on Coinbase, Binance, or Kraken, the French tax authority already receives your data. A change in tax residence doesn't erase the history of your past transactions.

Now imagine you do actually change your tax residence. You move to a country with favorable crypto taxation—say Dubai, which doesn't tax personal capital gains. You sell a significant portion of your Bitcoin portfolio six months after relocating. Technically, this gain should be taxed in the UAE—that is, not at all.

But if your former country of residence believes you were still tax resident at the time of the sale, it will claim its share. And proving otherwise requires far more than a rental lease and some passport stamps. You'll need to demonstrate that your life actually relocated there: local service contracts, health insurance cards, professional or associational memberships, bank movements consistent with living on-site. This wealth protection demands meticulous documentation.

Exit tax: a final fiscal hurdle

For substantial wealth, France (like other European countries) applies an "exit tax" on unrealized capital gains. If you hold more than €800,000 in financial assets and cease to be tax resident, the French authorities can immediately tax unrealized gains on your substantial holdings.

The question arises: do crypto assets count toward this threshold? The answer isn't yet entirely settled in case law, but regulatory trend leans toward inclusion. In other words, a substantial crypto portfolio could trigger this taxation upon departure, even if you haven't sold anything yet. This issue is comparable to risks from poorly anticipated decentralized governance: an apparently simple mechanism that reveals complex vulnerabilities.

Deferral or postponement mechanisms exist, particularly if you're moving to another EU country. But they require specific declarations, annual monitoring, and don't exempt you from tax if you eventually realize your gains.

Build a coherent strategy rather than seek a miraculous escape

So should you abandon optimizing your tax situation in retirement when holding crypto assets? Absolutely not. But you must do it methodically, on solid ground, and with substantial advance planning. Optimizing your crypto retirement involves a comprehensive wealth strategy.

The first step is clarifying your actual objectives. Are you simply looking to reduce future tax on gains you plan to realize? Do you want to pass your crypto wealth to your children under optimal tax conditions? Do you wish to live elsewhere primarily for quality of life, with taxes being just one factor among others?

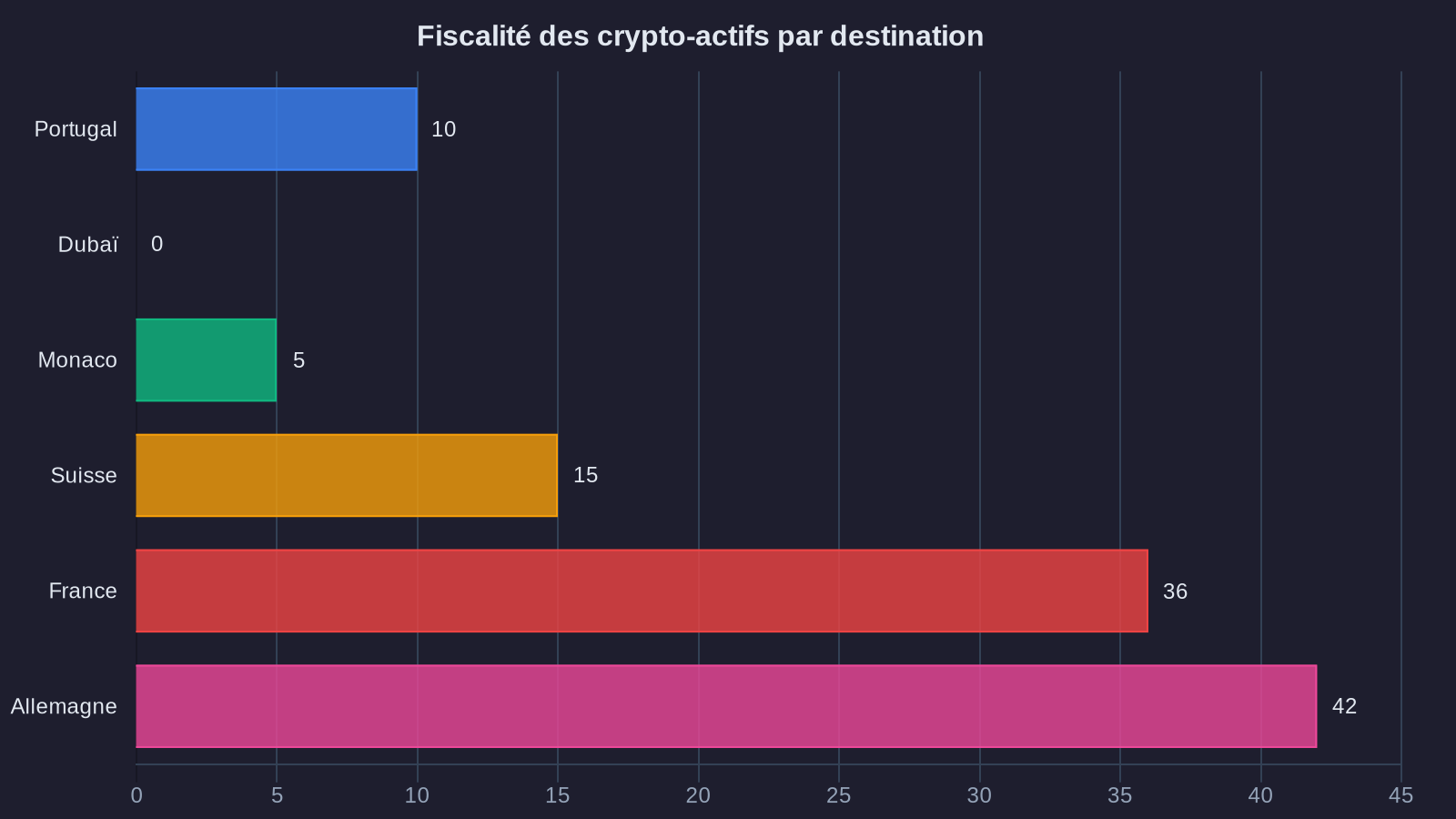

These questions determine the relevant destination country. Portugal offers interesting advantages but now taxes crypto for newcomers. Dubai or Singapore offer near-zero taxation but involve significant cultural and geographic upheaval. Switzerland combines stability and reasonable tax treatment, but with high living costs. Each destination has its trade-offs.

Next, you must prepare the ground well before your actual move. This means meticulously documenting your situation: keeping a journal of days spent in each country, preserving all proof of your relocation (leases, utilities, registrations), organizing your finances consistently with your new residence.

Mistakes never to make

Certain practices are particularly risky. Declaring tax residence in a country where you don't actually live, betting on weak cross-border controls. Using opaque offshore structures to "hide" your crypto assets while remaining the beneficial owner. Orchestrating constant back-and-forth between countries to stay just below residency thresholds.

These strategies might work for a few years. But they create permanent vulnerability. A tax authority inquiry, a legislative change, a tax audit in the context of an inheritance, and the entire structure collapses. With penalties reaching 80% of amounts involved, plus late-payment interest.

There are also more subtle mistakes. For example, changing tax residence just before realizing substantial gains. This sequence immediately attracts attention and will be scrutinized closely. Better to establish yourself solidly in your new country for at least a year, create real presence, then only afterward consider significant operations on your crypto portfolio.

Toward comprehensive wealth planning

Beyond purely tax aspects, changing residence in retirement with substantial crypto wealth raises questions about asset protection and succession planning.

How can you ensure your heirs can access your crypto assets if something happens to you in your new country of residence? Succession laws vary considerably. Some countries apply community property regimes, others strict separation of assets. Is your French will recognized in your new country? Are your private keys sufficiently secure while remaining accessible to trusted loved ones?

These questions transcend immediate tax optimization. They touch on the longevity of your wealth and your peace of mind. It would be paradoxical to optimize taxes on crypto assets while creating a total loss risk through inadequate succession planning. Securing your digital assets requires the same vigilance observed in stablecoin protection mechanisms.

Similarly, protection against geopolitical risks deserves consideration. A fiscally attractive country today can radically shift policy tomorrow. Some countries have changed rules overnight, sometimes retroactively. Diversifying your residences, maintaining fallback options, keeping solid ties to your country of origin—all this forms part of a robust wealth strategy.

Conclusion: enlightened optimization rather than risky evasion

Tax mobility is a right. Choosing to settle in a country where taxation better suits your wealth situation is perfectly legitimate. But this choice must be embraced fully, with all its practical and personal implications.

For crypto asset holders approaching retirement, the challenge is building a coherent strategy combining tax optimization, legal security, and quality of life. Protecting your retirement against tax residence changes requires surrounding yourself with specialized advice—tax lawyers knowledgeable about crypto, international mobility experts, notaries capable of navigating multiple legal systems.

The age of improvisation has ended. Tax authorities have developed sophisticated information-sharing tools. Crypto assets are no longer in a gray zone. Changing tax residence remains a powerful option for wealth optimization, but it demands rigorous preparation and flawless execution.

Before packing your first box, ask yourself: Am I ready to actually live elsewhere, or am I simply seduced by theoretical optimization? Your answer to this question will determine the success or failure of your wealth strategy.

```