In 2022, Fidelity Investments crossed a symbolic milestone by authorizing crypto assets in its 401k plans. This decision opened the door to a $10 trillion market of American retirement savings. Three years later, the landscape of American crypto retirement has undergone profound transformation. What was still considered a bold experiment is gradually becoming a mainstream option for institutional investors.

This evolution raises strategic questions for the entire financial ecosystem. How does this integration reshape traditional portfolio balances? What returns can we reasonably anticipate over long horizons? And most importantly, how is this American trend influencing investment practices in Europe, where retirement savings vehicles remain largely closed to this asset class?

American retirement savings: a $10 trillion giant seeking returns

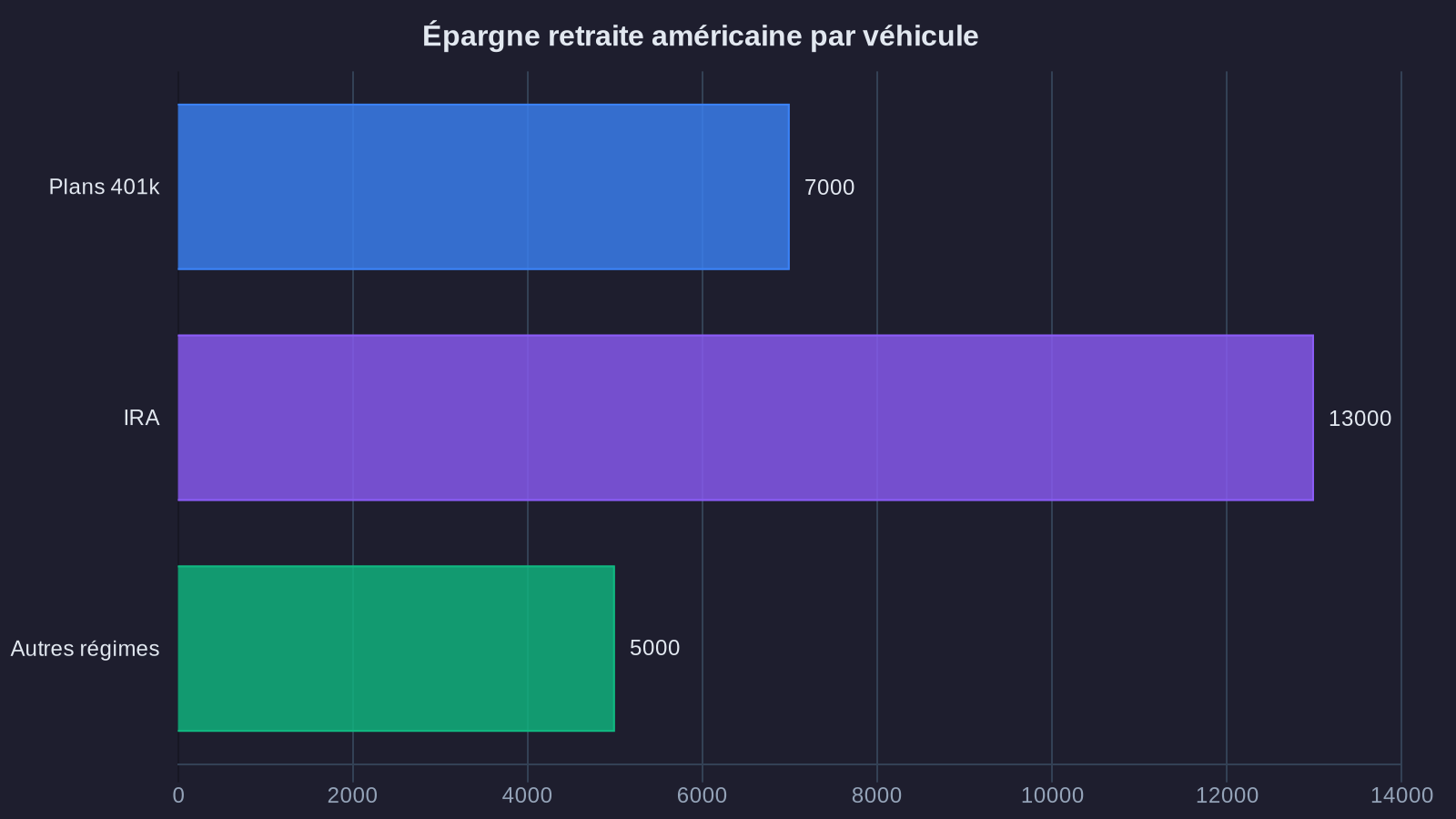

401k plans form the backbone of retirement savings in the United States. With nearly $7 trillion in assets under management in 401k plans alone, plus Individual Retirement Accounts (IRAs) accounting for approximately $13 trillion more, the scale is immense. These investment vehicles benefit from substantial tax advantages, making them preferred tools for building wealth over the long term.

The current environment makes this capital base particularly sensitive to return opportunities. Government bonds offer real rates that are often negative after inflation. Equity markets, following a decade of elevated valuations, show moderate return prospects according to consensus projections. Facing these constraints, plan managers are seeking uncorrelated sources of performance.

This is the context in which crypto assets began attracting attention. Not as a cure-all, but as a complementary building block in a diversified allocation. Historical data shows high short-term volatility, but also annualized returns that significantly exceed traditional asset classes over long holding periods—precisely the relevant horizon for a retirement crypto investment.

From tacit prohibition to progressive integration under 401k regulation

For a long time, the 401k plan industry viewed crypto assets as incompatible with the fiduciary obligations governing retirement savings management. The U.S. Department of Labor even issued explicit warnings in 2022, urging managers to exercise caution. This hesitation stemmed from several factors: extreme volatility, absence of stable regulatory framework, fraud risks, and lack of long-term performance track record.

The position evolved progressively under the pressure of 401k regulations. Fidelity, which manages approximately $2.5 trillion in its 401k plans, pioneered the way with a product allowing capped exposure of up to 20% of the portfolio. Other major players like Charles Schwab or Vanguard have adopted more cautious approaches, offering indirect exposure through ETFs or structured products rather than direct holdings.

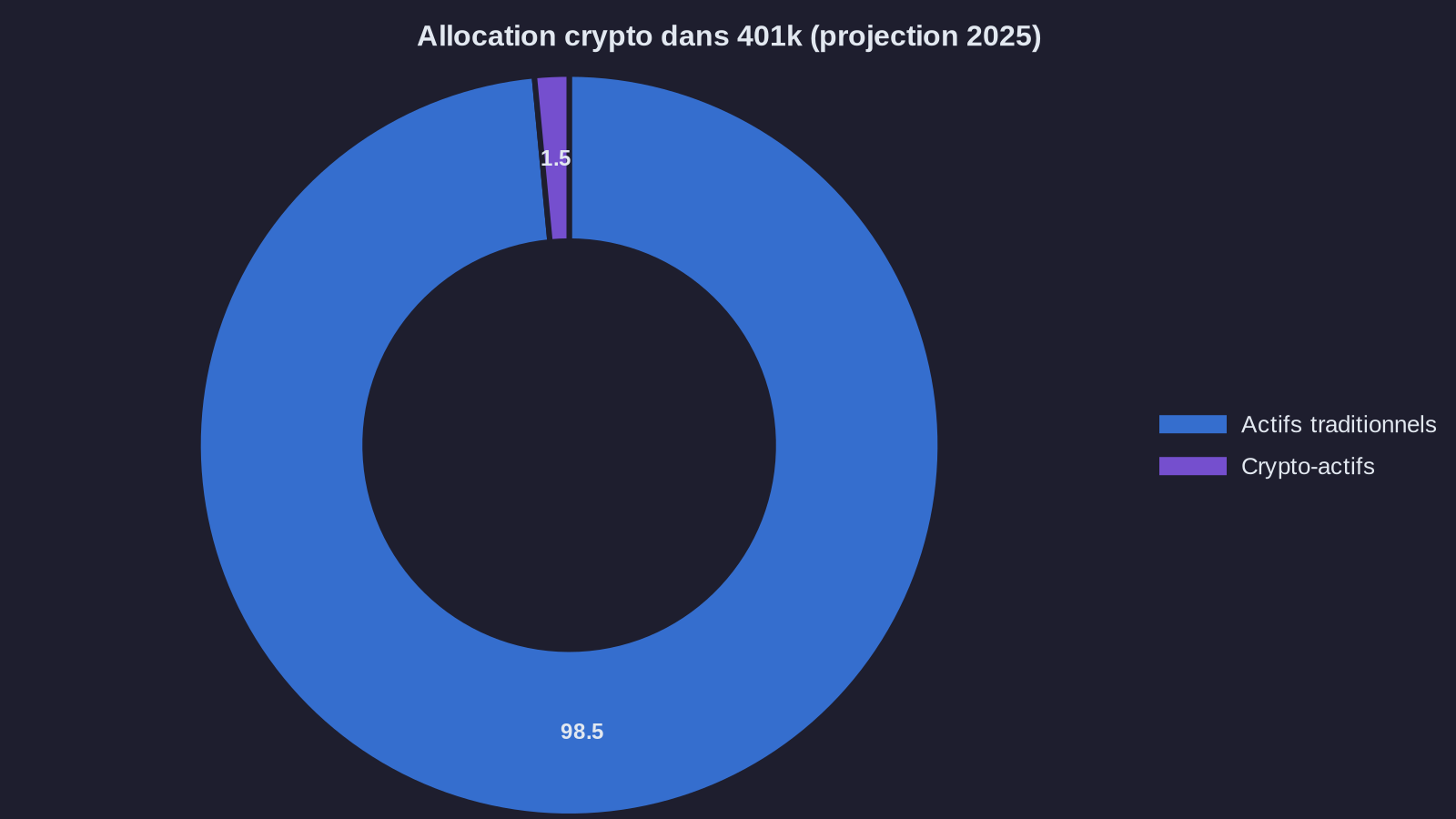

This diversity of approaches reflects a reality: there is no consensus on the optimal way to integrate these assets into a retirement portfolio. Some managers favor Bitcoin as a digital store of value, while others explore multi-asset strategies including Ethereum and selected DeFi protocols. Allocations generally remain limited to 1–5% of total portfolio, a weighting that allows capturing a portion of potential performance while managing overall risk, as illustrated by the challenges of genuine diversification.

Structural returns and portfolio balances

The central argument for crypto exposure in a retirement plan hinges on the historically low correlation with traditional asset classes. Over the 2015–2023 period, Bitcoin showed an average correlation of 0.2 with the S&P 500 and virtually none with bonds. This property makes these assets a potentially effective diversification tool, provided one understands the mechanisms governing their valuation.

Historical returns are impressive, no doubt about it. A $10,000 investment in Bitcoin at the start of 2015 was worth approximately $400,000 by end of 2023, despite several severe corrections. But these figures must be contextualized. Past trajectory guarantees nothing for the future, and growing institutional adoption could precisely reduce future volatility, thereby mechanically lowering potential returns.

What changes with integration into 401k plans is the investment discipline imposed by regular contribution mechanisms. An employee contributing monthly to their plan benefits from automatic price averaging, a strategy particularly effective for volatile assets. Simulations conducted by several consulting firms show that a 3–5% allocation to Bitcoin, maintained over 20 years with annual rebalancing, would have historically improved the return-risk profile of the overall portfolio.

The question of valuation framework remains. Unlike stocks or bonds, crypto assets don't generate predictable cash flows. Their valuation relies on anticipating growing adoption and their potential role as an alternative store of value. This nature makes projection particularly challenging, hence the importance of limiting exposure and maintaining rebalancing discipline.

Implications for European investors: digital assets IRAs and pension fund blockchain

American developments don't mechanically replicate in Europe, where retirement systems follow different logics. Vehicles like the PER (Plan d'Épargne Retraite) in France or Swiss pillar 3a accounts remain largely invested in traditional funds. European insurers and managers display marked caution, often justified by more restrictive regulatory frameworks and a different risk culture.

Yet several signals indicate progressive change in the adoption of digital assets IRAs. Specialized fintechs are beginning to offer solutions allowing crypto assets to be integrated into tax-advantaged wrappers, respecting local regulatory constraints. The arrival of Bitcoin and Ethereum ETFs on European markets also facilitates access for institutional investors seeking regulated exposure.

The central question for European investors isn't so much whether to replicate the American model, but rather how to adapt allocation principles to their own context. A French investor preparing for retirement over a 25-year horizon can legitimately consider whether modest exposure to uncorrelated and potentially performing assets makes sense. The answer depends on risk tolerance, overall wealth, and ability to maintain an allocation over the long term despite fluctuations.

ForYield observes that clients integrating a crypto component into their long-term savings strategy typically do so with allocations of 2–8%, complementing a diversified base of stocks and bonds. This approach allows capturing part of performance potential while preserving overall portfolio stability. Regular rebalancing, which periodically brings each asset class back to its target weight, becomes particularly important in this context.

Perspectives and new frontiers of pension fund blockchain

The progressive integration of crypto assets into American retirement savings probably marks a structural turning point. Beyond the $10 trillion theoretically accessible, institutional legitimation is what counts. When the world's largest asset managers accept integrating these assets into fiduciary products subject to strict regulatory constraints, it validates a certain market maturity.

This evolution comes with innovations in available products. Spot Bitcoin and Ethereum ETFs, approved by the SEC in 2024, collected tens of billions within months. Regulated staking solutions are starting to emerge, allowing additional yield generation on certain assets while respecting institutional custody requirements—a trend that institutional stablecoin adoption also illustrates. The boundary between traditional finance and crypto ecosystem is progressively becoming more porous.

Nevertheless, several challenges persist. Volatility remains elevated, though it tends to decrease with growing market capitalization. The regulatory framework continues evolving, with divergent approaches across jurisdictions. Security and custody questions require institutional standards that only a few players truly master. And public understanding remains limited, creating risk of mismatch between offered products and actual needs.

The challenge for coming years will be finding the right balance: enabling access to this asset class for those who understand its mechanisms and accept associated risks, while protecting less sophisticated savers against exposures ill-suited to their profile. American and European regulators are actively working on these questions, with approaches favoring either freedom of choice or strict protection.

One thing seems certain: crypto assets won't disappear from the institutional investment landscape. Their integration into 401k plans constitutes a step toward progressive normalization, likely accompanied by reduced volatility and greater ecosystem professionalization. For investors preparing for retirement today, the question is no longer whether these assets belong in an allocation, but rather what proportion and according to what strategy.