You've diversified your portfolio across fifteen different assets. European equities, government bonds, listed real estate, commodities, crypto assets. Historical correlations are low, even negative. On paper, your allocation is exemplary. Yet during the next market correction, you may find that all your positions decline simultaneously by 20 to 30%. How is this possible?

This situation is not theoretical. It happens regularly, even among sophisticated investors who have methodically built their portfolio allocation based on statistical correlations. The problem doesn't stem from a calculation error, but from a fundamental illusion: confusing apparent diversification with actual wealth resilience.

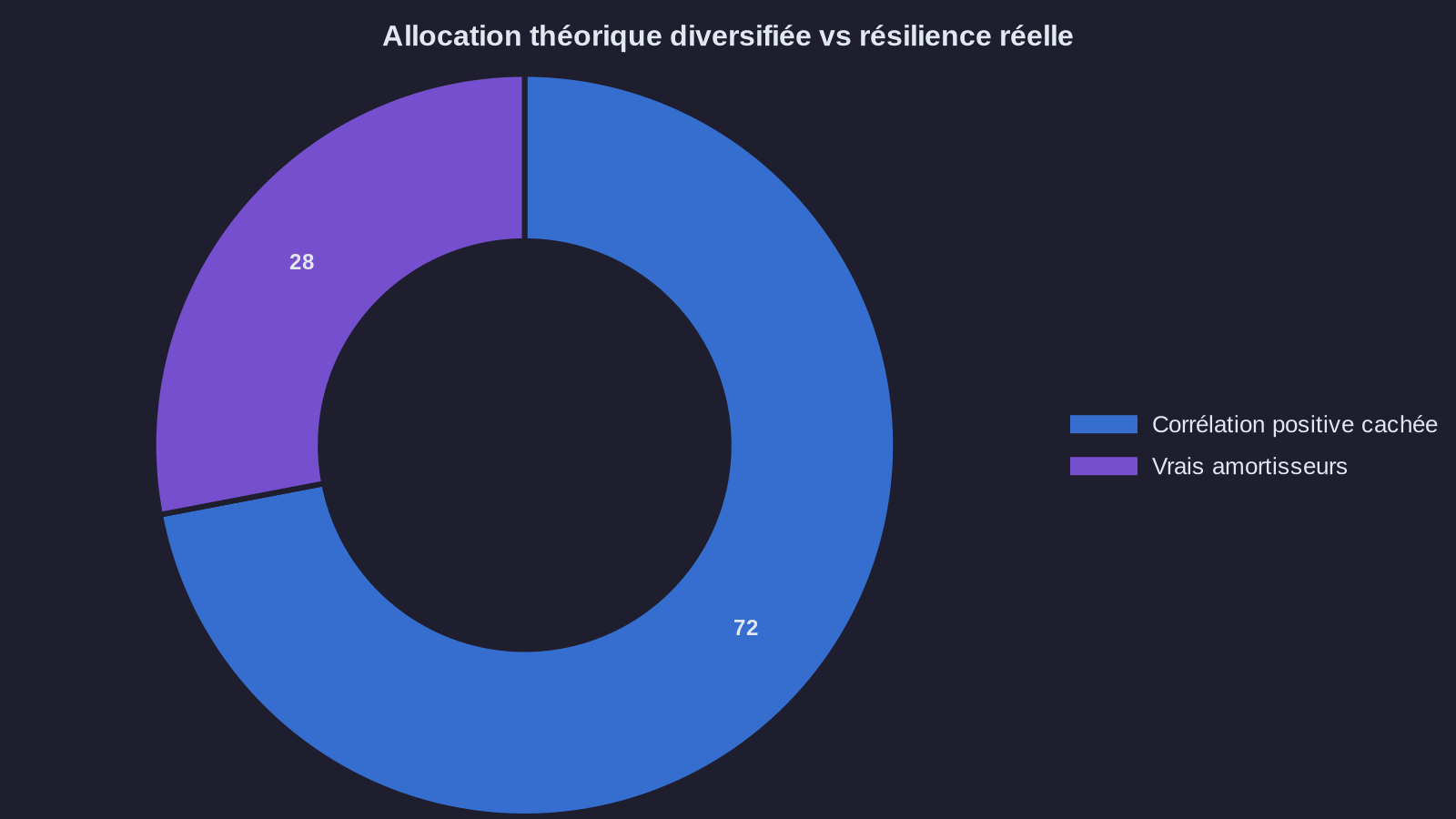

Let's take a concrete case that was recently analyzed in depth. Wick Capital, an active investment fund in the crypto ecosystem, displayed an allocation that seemed intelligently diversified: Bitcoin, Ethereum, first-generation DeFi protocols, stablecoins, positions on decentralized derivatives. Correlations between these assets, measured over 12 to 24 months, were moderate. Yet during the 2022-2023 bear cycle, the entire portfolio suffered a synchronized correction, with no position playing a counterbalance role. A situation that underscores the importance of securing your crypto portfolio holistically.

Correlation is not causation: what the numbers don't reveal

Asset correlation measures the degree of joint movement between two assets over a given period. A coefficient of 0.3 between two positions tells you they move relatively independently of each other. A coefficient of -0.2 even suggests slight decorrelation. It's mathematically accurate. It's insufficient for wealth preservation.

Why? Because correlation is a snapshot of the past under normal market conditions. It tells you nothing about what will happen when conditions become abnormal. Yet it's precisely in those moments—crashes, liquidity panics, systemic crises—that you need your diversification to actually work.

Let's revisit the Wick Capital case. During 2020-2021, correlations between Bitcoin and DeFi tokens were moderate (between 0.4 and 0.6). Bitcoin could rise 15% while a lending protocol remained stable, or vice versa. This apparent independence created the illusion of genuine diversification. But all these assets shared a common risk factor invisible in the correlations: overall liquidity in the crypto market.

When that liquidity contracted sharply in 2022—the Fed's monetary tightening, bankruptcy of several major players, a crisis of confidence—all positions fell simultaneously. The correlation between Bitcoin and DeFi tokens jumped from 0.5 to 0.9 in a matter of weeks. It's not that the assets suddenly became correlated. It's that the underlying risk factor, masked in normal times, became dominant.

An investor who allocated €100,000 to this type of portfolio in January 2022 could have found themselves with €35,000 to €40,000 by June 2023, despite "diversifying" across ten different assets. The loss would have been barely less severe than a concentrated position in Bitcoin alone.

Hidden risk factors: what actually moves your wealth

The real question isn't: "What's the correlation between my assets?" The real question is: "What are the common risk factors that could simultaneously affect my positions?"

Let me share three concrete examples I regularly encounter in wealth management.

First case: the "diversified" equity portfolio. An investor holds positions in fifteen different companies: Total, LVMH, Sanofi, BNP Paribas, Airbus, Schneider Electric, and so on. Sectors vary (energy, luxury, healthcare, finance, industry). Individual correlations are moderate. Yet all these positions share a systemic risk factor: exposure to the European economic climate. If the eurozone enters recession, all these stocks will fall together, regardless of their historical correlations.

Second case: the "diversified" real estate portfolio. Wealth spread across four rental properties: an apartment in Paris, another in Lyon, a house in Bordeaux, a studio in Marseille. Geographically diversified. Varied property types. But all these assets share the same risk factor: rising interest rates. When rates go from 1% to 4% in 18 months, all French real estate prices drop by 10 to 15%, regardless of the city. Geographic diversification protected no one.

Third case: the "prudent" crypto portfolio. An allocation of Bitcoin (50%), Ethereum (30%), staking stablecoins (15%), and some positions in established DeFi protocols (5%). Correlations between these assets are weak to moderate in normal times. But all depend on a common factor: confidence in the crypto infrastructure itself. If a systemic event occurs—major hack, regulatory ban, failure of a central platform—the entire portfolio is affected. Besides, generating passive income from crypto assets requires a nuanced understanding of these interdependent risks.

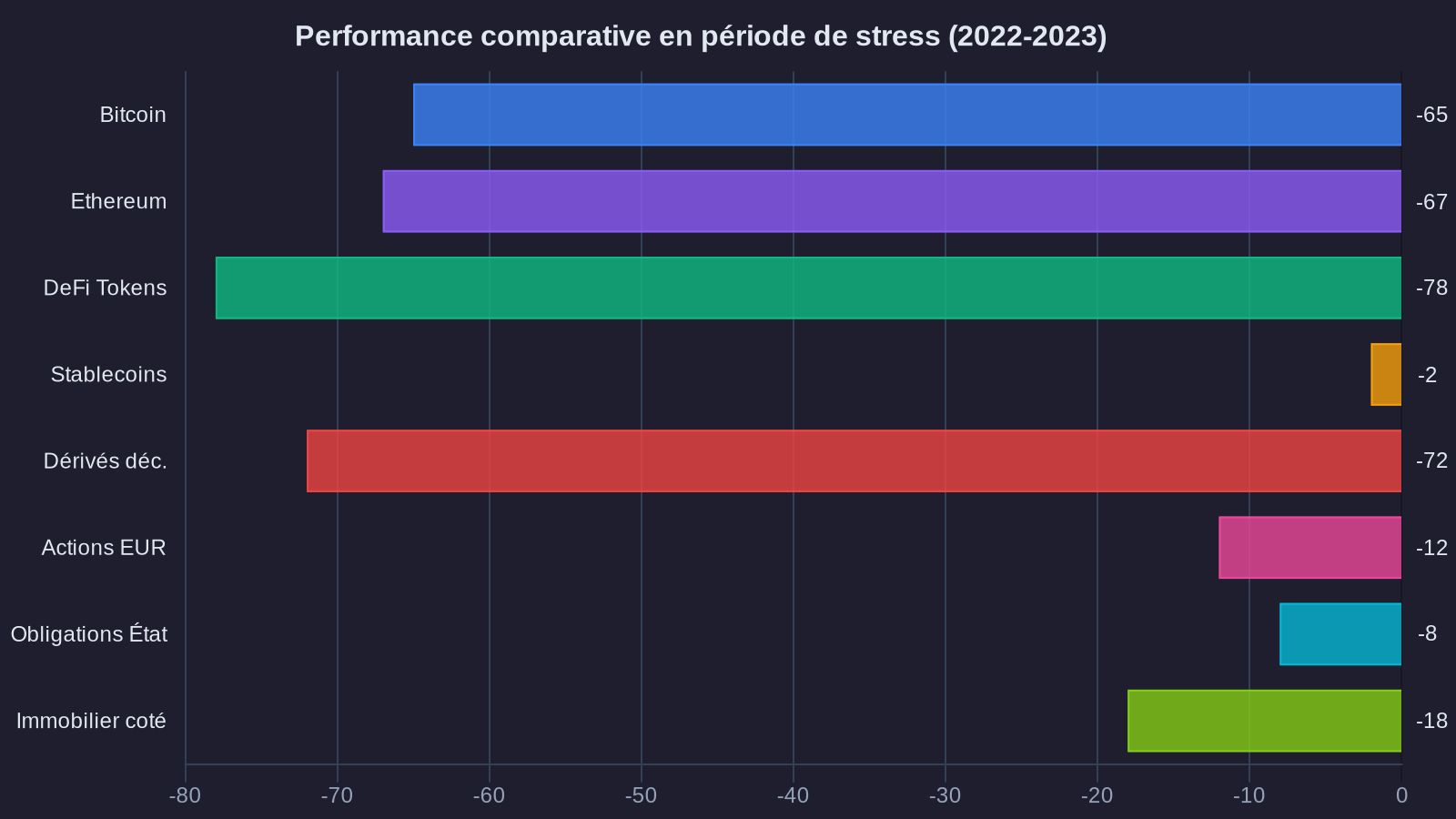

Back to the numbers. Let's take a €200,000 portfolio distributed as follows:

- €100,000 in Bitcoin

- €60,000 in Ethereum

- €30,000 in stablecoins (USDC) staked at 8% annually

- €10,000 in DeFi tokens (Aave, Uniswap, Curve)

Over the period January 2022 – June 2023, this portfolio would have lost approximately 55 to 60% of its value, despite holding stablecoins meant to provide stability. Why? Because even stablecoins suffered a confidence crisis (the case of USDC during the Silicon Valley Bank collapse in March 2023), and staking yields collapsed with overall market liquidity.

Compare this to a portfolio truly diversified across risk factors:

- €80,000 in French government bonds (10-year OAT)

- €50,000 in Bitcoin

- €30,000 in euro money market fund

- €20,000 in physical gold

- €20,000 in Ethereum

Over the same period, losses would have been limited to approximately 15 to 20%. Government bonds lost around 10% as rates rose, but gold advanced 8%, the money market fund remained stable, and crypto positions, though heavily down, represented only 35% of total allocation. Your wealth would have weathered the storm.

Building genuine diversification: beyond correlations

If correlation isn't enough, how do you build a truly resilient portfolio? By reasoning about risk factors, not about asset classes or historical statistics.

Start by identifying the risk factors your wealth is exposed to. Ask yourself this question for each position: "What could cause this asset to fall 20% or more?" The answers go beyond the intrinsic volatility of the asset. They touch on structural elements: market liquidity, interest rates, inflation, confidence in an infrastructure, economic conditions, regulation, etc.

Next, ensure your portfolio contains assets exposed to different, even opposing risk factors. A concrete example: if you hold crypto assets (risk factor = crypto liquidity + appetite for risk), add government bonds or gold (opposite risk factor = risk aversion + flight to quality). If you hold rental real estate in France (risk factor = interest rates + French economic conditions), add geographically and structurally uncorrelated assets: US equities, inflation-linked bonds, staking stablecoins with dollar exposure.

Let's take a standard wealth management example: a profile with €500,000 to allocate, a 10-year horizon, and moderate risk tolerance. Here's a portfolio allocation built on risk factors, not correlations:

- €150,000 in quality government bonds and bond funds (risk factor = interest rates, credit quality). Expected net return: 3.5% to 4% annually. Protection during recession or systemic crisis.

- €150,000 in globally diversified equities (risk factor = global economic growth, market sentiment). Expected return: 6% to 8% annually. Exposure to long-term value creation.

- €100,000 in established crypto assets (Bitcoin 60%, Ethereum 30%, staked stablecoins 10%). Risk factor = technology adoption, crypto liquidity. Expected return: 8% to 12% annually on average, with high volatility. Potential for structural appreciation.

- €50,000 in physical gold or gold ETFs (risk factor = inflation, geopolitical instability). Expected return: purchasing power protection, low correlation with other assets. Wealth insurance.

- €50,000 in cash or money market funds (risk factor = none). Current return: 3% to 3.5%. Reserve for opportunities and safety buffer.

This ETF and multi-asset diversification doesn't rely on correlations calculated from historical market data. It relies on a logic of opposing risk factors. If equities fall during recession, government bonds rise. If inflation picks up, gold protects. If crypto markets correct, cash allows you to buy at low prices. If rates spike, crypto staking or lending offers yields exceeding short-term bonds.

Over 10 years, with annual rebalancing, this type of allocation generates an average net return of 5% to 6.5% annually, with controlled volatility and resilience during shocks. A portfolio concentrated solely on crypto assets, even if "diversified" internally, would have higher return potential (10% to 15%), but with a risk of 50% to 70% capital losses during stress periods. The risk-adjusted return/risk ratio clearly favors diversification by factors.

What this means for your wealth

Correlation is a tool. It's not a strategy. You can build a portfolio that's perfectly uncorrelated by statistics, yet find yourself facing a 40% loss during the next crisis because all your assets share a common, hidden risk factor.

True diversification means identifying these risk factors and ensuring your wealth contains assets that react differently, even oppositely, to the same events. This requires more thought than simply consulting a correlation matrix. But it's what makes the difference between a portfolio that survives storms and one that sinks with the ship.

If you currently hold more than €100,000 in crypto assets, ask yourself this: what protects my wealth if crypto liquidity contracts sharply for 18 months? If the answer is "nothing," you're not diversified. You're exposed to a single risk factor, regardless of how diverse your positions appear.

Your wealth deserves better than a savings account. But it also deserves better than false diversification. I show you the path, backed by numbers.

```