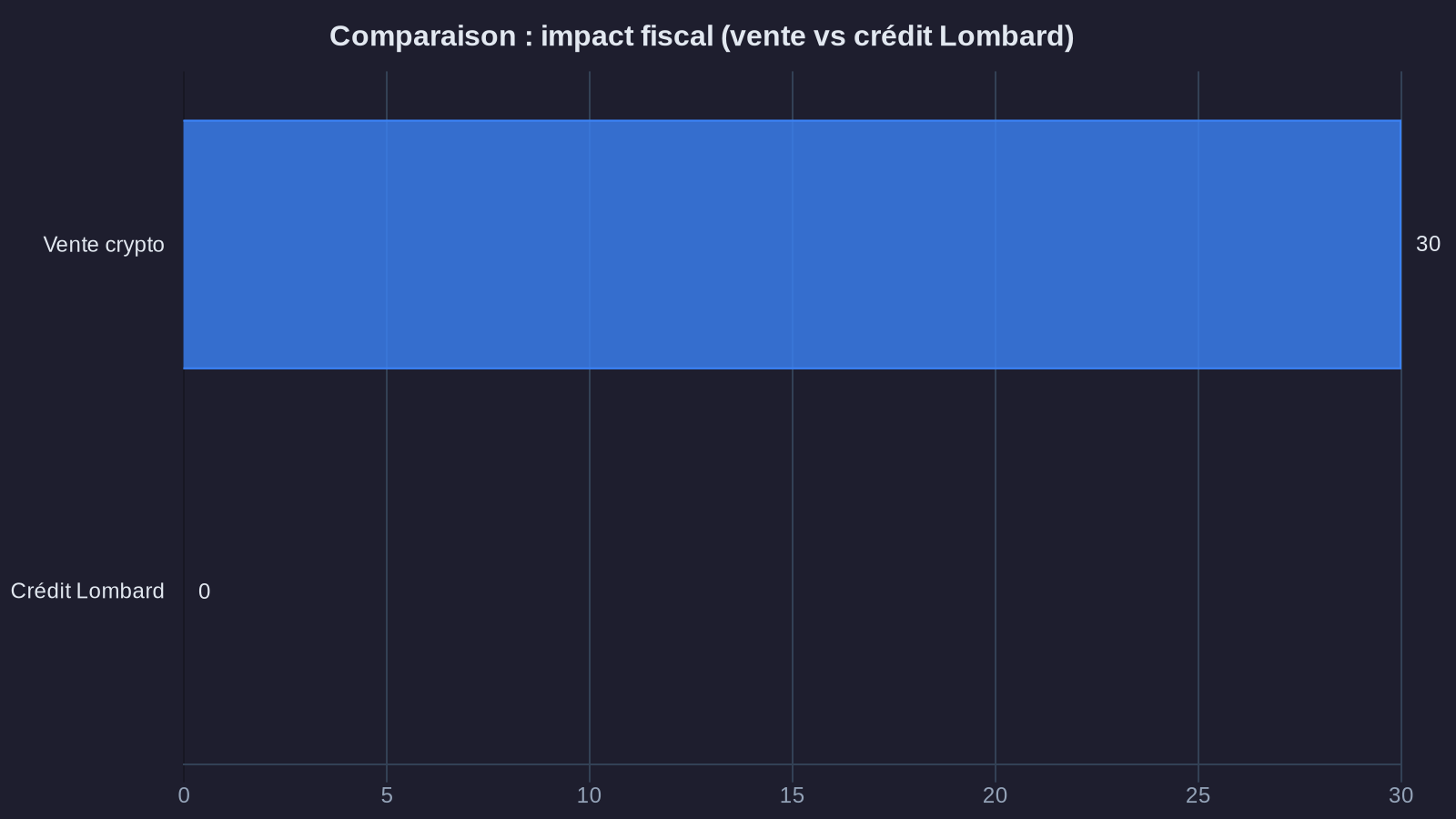

You hold crypto assets with significant unrealized gains. You'd like to tap into their value to finance a project, make a purchase, or simply cover your current expenses. The catch: the moment you sell, you trigger capital gains tax. At the shareholder rate of 30% (flat tax), selling €100,000 in gains costs you €30,000 in tax. This is precisely the tax mechanism that Ether.fi's payment card and Lombard lending legally circumvent.

These tools rest on a simple principle: you're only taxed when you actually sell your crypto. If you keep them as collateral and borrow against their value, no sale occurs. Therefore, no taxable event. French tax authorities, like most jurisdictions, consider that only converting to legal tender (euros, dollars) or exchanging for goods or services constitutes a taxable sale. Borrowing liquidity backed by your crypto is not.

This mechanism is neither a gray area nor aggressive tax planning. It's the straightforward application of Article 150 VH bis of the French General Tax Code, which defines the taxable event for capital gains on the sale of digital assets. Let's see how this works in practice.

Crypto Lombard lending: borrow without selling

Lombard lending has existed in traditional finance for a long time. It lets you borrow liquidity by pledging a portfolio of stocks or bonds, without having to sell them. The same mechanism now applies to crypto assets, with a few adjustments for their volatility.

Here's how it works: you deposit your crypto (typically Bitcoin, Ethereum, or stablecoins) on a specialized platform. The platform lends you a sum in fiat currency or stablecoin, up to a certain ratio of your collateral's value. This ratio, called LTV (Loan-to-Value), typically ranges between 30% and 70% depending on the volatility of the pledged asset. The more stable the asset, the higher the LTV.

Let's walk through a concrete example. You own 10 ETH purchased at €1,000 per unit, for a cost basis of €10,000. The current price is €3,500. Your portfolio is worth €35,000, with €25,000 in unrealized gains. If you sell, you owe €7,500 in tax (30% of €25,000). With a Lombard loan at 50% LTV, you can borrow €17,500 by pledging your 10 ETH as collateral. You have access to this liquidity immediately, without triggering any tax, since you haven't sold your ETH.

You then repay the loan with interest. Rates vary by platform and duration, but typically range between 5% and 12% annually. If your investment strategy expects your crypto to continue appreciating, or if you simply need cash without wanting to exit your position, this mechanism is tax-neutral.

The main risk is liquidation. If your collateral's price drops and your LTV ratio exceeds the maximum threshold, the platform can liquidate part of your crypto to repay the loan. Only at that moment, and only then, will you trigger capital gains tax, because an actual sale will have occurred. This underscores the importance of maintaining a comfortable safety margin and monitoring your position.

The Ether.fi card: spend without selling

The payment card backed by crypto, offered by Ether.fi and others, works on a similar but adapted principle for everyday spending. You deposit your crypto on the platform, and it issues you a Visa or Mastercard usable everywhere. When you pay with this card, your crypto isn't directly exchanged for the good or service. The platform advances the funds in fiat currency, using your crypto as collateral.

Again, as long as you don't actually sell your crypto, no taxable event is triggered. The transaction is treated as an instant loan secured by your portfolio. You repay this revolving credit either by reloading your account with stablecoins, or eventually by a partial sale of your crypto if you choose to. But you decide when and how to realize that sale, and thus when you trigger the tax.

Here's a use case. You use your Ether.fi card to pay €2,000 in monthly expenses. The platform advances the €2,000 and freezes part of your crypto collateral as security. At month-end, you have two options: either reload your account in stablecoin or euros to settle the debt, or let the platform convert the equivalent in crypto. If you reload with stablecoins acquired at their par value (1 USDT = 1 USD), there's no gain to report. If you let the platform sell your ETH to settle the debt, then you report the gain on the portion sold only.

This tool gives you total tax flexibility. You can choose never to sell your crypto gains, funding repayments from other income (salary, dividends, stablecoins). Or you can spread sales across multiple years to smooth your tax burden, or even wait for a year when your overall income is lower to benefit from a lower tax bracket if you've chosen the progressive scale.

Legal and tax risks to be aware of

This structure is legal, but not without risk. The first is recharacterization by tax authorities. If they determine that the card or Lombard mechanism actually constitutes a disguised sale, they can challenge your return and demand tax payment plus penalties and late fees.

To date, no French case law specifically addresses this issue. But tax authorities could invoke the doctrine of abuse of rights (Article L. 64 of the French Tax Procedures Code) if they consider the arrangement has no purpose other than tax avoidance. To mitigate this risk, it's essential that your use of Lombard lending or a crypto card have real economic logic: fund a project, smooth cash flow, avoid exiting a strategic position. If you borrow heavily only to immediately repurchase other crypto, authorities could view this as an artificial scheme.

The second risk is traceability. Most platforms offering these services are regulated and subject to KYC and tax reporting obligations. Ether.fi, for instance, will need to comply with the MiCA regulation upon full implementation. This means French tax authorities will have access, through automatic information exchange between jurisdictions, to your fund movements. Don't count on opacity to escape taxation. If you use these tools, document them properly and be prepared to justify your tax position.

The third point to watch concerns borrowing interest. Unlike a mortgage or business loan, interest paid on crypto Lombard lending is generally not tax-deductible in France, unless you can demonstrate the loan finances an income-generating activity (for example, a rental investment or business). For personal use, interest remains your burden without tax offset.

The key cautionary note

Absence of immediate sale doesn't mean absence of total tax. It means deferral. If you heavily use Lombard lending or a crypto card, you accumulate latent tax debt that materializes when you liquidate positions or make partial sales to repay. Anticipate this future liability in your wealth planning. Don't find yourself in a position where, to repay a loan, you must urgently sell in a bear market, triggering both capital loss and tax on previous unrealized gains.

One final point concerns tax residency. If you're a French tax resident, these rules apply. If you change tax residency, notably to a jurisdiction without capital gains tax on crypto, the situation changes dramatically. But beware: exit tax (Article 167 bis of the French Tax Code) may apply if you hold more than €800,000 in financial assets when departing. Crypto assets fall within this scope. Consult a tax attorney before any expatriation.

Checklist before using these tools

- Verify the platform is regulated in a recognized jurisdiction (EU, Switzerland, US)

- Clearly understand the LTV ratio and liquidation conditions

- Document the economic purpose of your borrowing (project, cash flow, wealth strategy)

- Maintain sufficient safety margin to avoid forced liquidations

- Track movements and keep a record of loans and repayments

- Anticipate future tax liability if you must sell to repay

- Consult a crypto-savvy accountant before any significant use

Lombard lending and crypto cards aren't magic solutions to permanently escape taxation. They're wealth management tools that give you flexibility in timing your sales. Used wisely, they let you smooth tax burden, maintain strategic positions, and use your crypto's value without destroying your capital. Like mortgages secured by crypto, these mechanisms demand rigor, anticipation, and deep understanding of the tax mechanics at play. If you hold a significant crypto portfolio, this analysis is worth conducting with a financial professional who knows crypto assets.