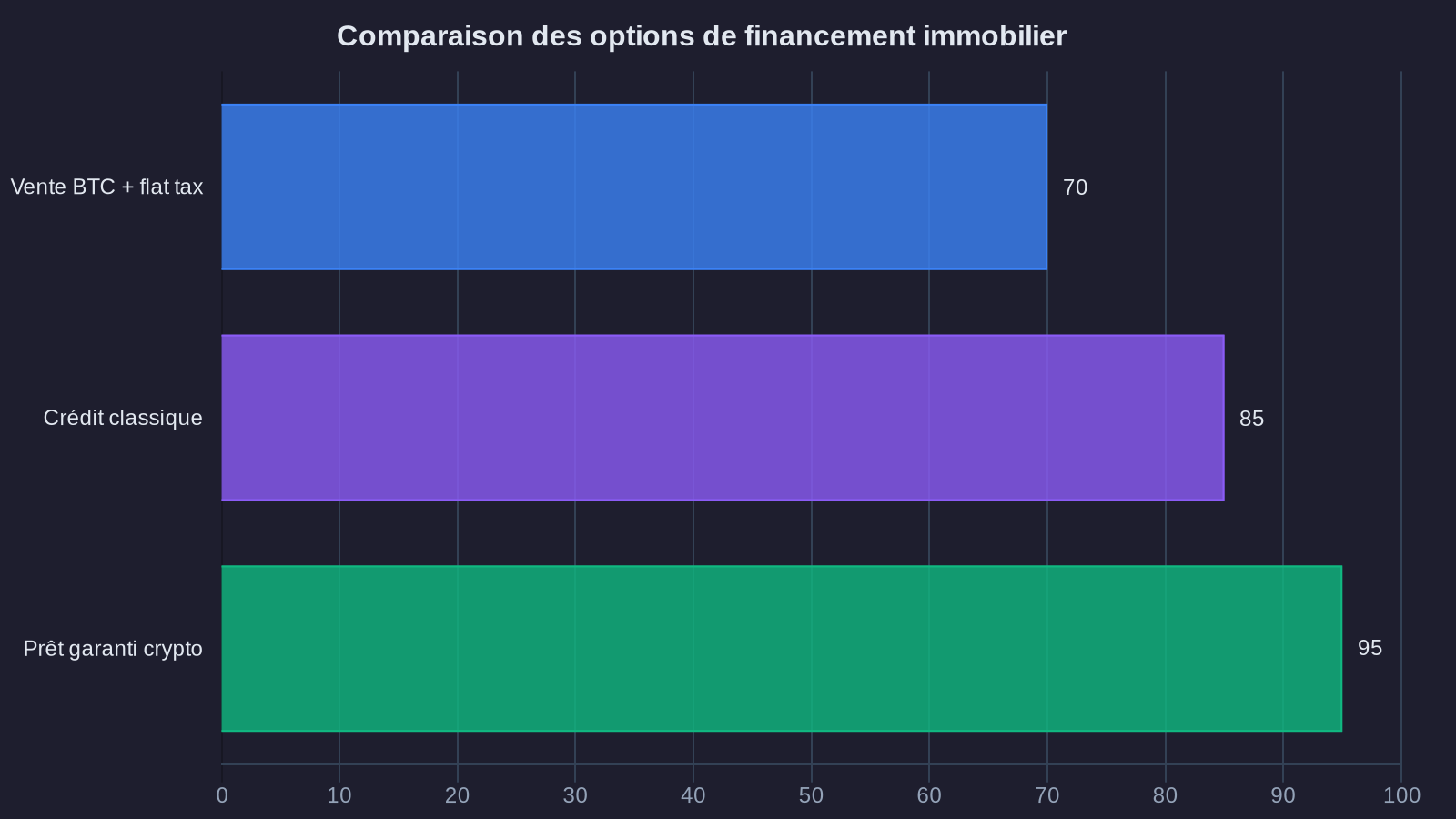

Picture this: you own 5 Bitcoin purchased in 2020, worth approximately €500,000 at current prices. You want to buy a primary residence for €400,000. Until now, you had two options: sell your Bitcoin (and pay 30% flat tax on the gains), or take out a traditional mortgage by putting down 10% in cash. Now, a third path is emerging across the Atlantic: use your crypto-assets as mortgage collateral without selling them.

Since December 2024, Coinbase, America's leading exchange platform listed on Nasdaq, has partnered with Figure Technologies to offer mortgage loans secured by Bitcoin and stablecoins. Meanwhile, Fannie Mae, the semi-public giant that guarantees 25% of U.S. mortgages, is testing the acceptance of crypto-assets in calculating borrower net worth. What seemed like science fiction two years ago is now becoming reality. And this quiet revolution is reshaping the contours of crypto real estate financing.

The mechanism: how crypto-secured mortgage loans work

The principle resembles a Lombard loan in private wealth management, a mechanism that family offices have used for decades to borrow against a stock portfolio. The difference? Here, the collateral is based on digital assets.

Let's take a concrete example. You own €300,000 in Bitcoin. You want to borrow €250,000 to finance a property. The lending institution (Coinbase via Figure Technologies, or other players like Ledn in Canada) will lock your Bitcoin in a secure multi-signature wallet. These Bitcoin remain your legal property, but they're pledged for the duration of the loan. The loan-to-value ratio (LTV) typically ranges from 50% to 70%: for every €100,000 in crypto deposited, you can borrow €50,000 to €70,000.

This haircut may seem significant. It's less so than it appears when compared to traditional real estate. In a standard transaction, you put down 10% equity and borrow 90%. Here, you put up 100% in crypto collateral, but you retain exposure to the potential upside of your assets. If Bitcoin appreciates by 30% during the loan term, your total wealth grows, unlike a scenario where you'd sold your positions to finance the purchase.

Interest rates range from 7% to 10% annually, or 2 to 3 percentage points higher than traditional mortgages in the United States (currently around 6.5% over 30 years). This risk premium reflects the volatility of underlying assets. In return, funds are released in 48 to 72 hours, versus 30 to 45 days for a traditional loan. Most importantly, there's no tax event: you're not selling anything, so no capital gains taxation.

Institutional validation: when Fannie Mae embraces blockchain

The real turning point doesn't come from native crypto players, but from established financial institutions. In January 2025, Fannie Mae issued a directive authorizing mortgage brokers to factor crypto-assets into borrowers' net worth calculations, under certain strict conditions.

Concretely, if you submit a mortgage application in the United States and hold $200,000 in Bitcoin on Coinbase, these assets can now be counted toward your borrowing capacity, just like a brokerage account at Fidelity or Vanguard. Three cumulative conditions apply: assets must be held for at least two months, on a regulated platform (not on a personal cold wallet), and represent a maximum of 30% of total net worth considered.

This development may seem technical. It's fundamental. Fannie Mae guarantees or holds approximately $7 trillion in U.S. mortgage loans. Its green light amounts to institutional endorsement. Regional banks and credit unions, which had viewed the subject with skepticism, are now beginning to structure their own offerings. United Wholesale Mortgage, the second-largest U.S. mortgage lender, announced in February 2025 that it would accept crypto-assets as supplementary collateral by summer.

The potential market is massive. According to Glassnode, 8.2 million Americans hold at least $50,000 in Bitcoin or Ethereum. Among them, 35% are renters and plan to buy a primary residence within three years. If just 10% opt for hybrid crypto real estate financing (cash down payment plus crypto collateral), that represents $12 billion in additional mortgage loans annually.

The wealth risks: what your private banker should explain to you

This all sounds attractive on paper. Wealth management reality imposes several points of caution that any crypto-asset holder should consider before committing.

First risk: margin calls. If Bitcoin drops 40% in three months (which has happened five times since 2017), your LTV ratio deteriorates mechanically. Imagine you borrowed $200,000 with $400,000 in Bitcoin as collateral (50% LTV). If Bitcoin falls 40%, your collateral is now worth just $240,000. Your LTV jumps to 83%. The lender will demand you either partially repay the loan or post additional crypto-assets. If you can't, they'll liquidate part of your positions to bring the ratio back in line. Exactly what happens with a standard Lombard loan when stocks collapse.

Second risk: carry costs. With an average rate of 8.5% and a 20-year term, the total loan cost reaches 204% of the borrowed capital. On $200,000 borrowed, you'll repay $408,000 total. A traditional mortgage at 6.5% over the same period would cost $358,000, or $50,000 less. Admittedly, you retain your Bitcoin. But if Bitcoin doesn't appreciate more than 2% annually on average over the period, the deal is a wealth loser compared to a partial sale.

Third risk: legal rigidity. Current contracts provide no flexibility in case of hardship. You lose your job? You must continue full repayment, or face forced liquidation of your assets. A traditional mortgage offers renegotiation options, payment deferrals, even restructuring. Here, the blockchain doesn't negotiate. The smart contract executes. Period.

Concrete wealth simulation: for a €250,000 loan secured by €500,000 in Bitcoin, at 8.5% over 20 years, your monthly payments are €2,185. If Bitcoin appreciates 10% annually on average (optimistic but observed over the past 10 years), your €500,000 collateral will be worth €3.4 million in 20 years. Your net crypto wealth, after loan repayment, would reach €3.15 million. If you'd sold €250,000 of Bitcoin upfront to finance the property, your remaining €250,000 would be worth €1.7 million. The gap? €1.45 million. But this calculation assumes linear Bitcoin appreciation, which matches no historical reality. Factoring in actual volatility (50 to 80% drawdowns every 4 years), the risk of margin calls becomes statistically probable.

What about Europe? The early signs of a regulated market

France and the European Union are watching this movement with a mix of regulatory caution and growing interest. The MiCA regulation (Markets in Crypto-Assets), in force since December 2024, creates a harmonized legal framework for crypto-asset service providers. Some European players are already testing crypto-secured loan offerings, but haven't yet backed them with tokenized real estate loans.

Nexo, a Bulgarian-origin platform regulated in Luxembourg, offers personal loans up to €2 million secured by Bitcoin, with LTVs up to 50%. Ledn, based in Toronto but operating in Europe via a MiCA license, offers similar financing. Neither player yet offers true mortgages, but discussions with European mortgage brokers have begun.

The main obstacle remains tax treatment. In France, pledging crypto-assets to secure a loan doesn't trigger immediate taxation. However, if the lender must liquidate part of the assets due to a margin call, that liquidation constitutes a taxable event for capital gains, taxed at 30%. This legal point isn't yet fully clarified by tax authorities, which dampens appetite from traditional banks.

Several Paris and Geneva family offices are nonetheless structuring hybrid arrangements: traditional real estate financing covering 80% of the amount, supplemented by a crypto-secured Lombard loan covering the 20% down payment. This approach limits margin call risk (since the crypto loan represents only a portion of total financing) while maintaining exposure to digital asset appreciation. Combined interest rates range from 7% to 9%, which remains competitive for wealth above €2 million, as explained in our analysis on how to generate passive returns on crypto-assets.

What this means for your wealth

The acceptance of crypto-assets as mortgage collateral is no longer anecdotal. It marks the progressive integration of digital assets into the traditional financial system. For Bitcoin and Ethereum holders, it opens a third wealth strategy between immediate sale (taxed) and passive waiting (illiquid).

Three investor profiles can legitimately consider this option. First, those holding a significant portion of their wealth in crypto-assets (over 30%) who want to diversify without triggering taxation. Second, those anticipating long-term structural Bitcoin appreciation and seeking to maximize exposure. Third, real estate investors wanting to purchase in cash to negotiate a discount while keeping their crypto portfolio intact.

For everyone else, caution remains warranted. A traditional French mortgage at 3.8% (current 20-year rate) remains mathematically more advantageous than an 8% hybrid loan, unless your crypto-assets outperform by over 4.2% annually after volatility. It's possible, but not guaranteed, as shown in our study on portfolio diversification.

The real wealth question isn't "can I use my Bitcoin to buy my house?" but "does this strategy optimize my net wealth in 20 years, given my ability to absorb volatility and potential margin calls?" If you can't answer affirmatively with specific numbers, the traditional approach remains wisest.

Your wealth deserves better than a savings account. I'll show you the path, with numbers to back it up.```