One million euros by age 40. That's the figure your favorite FIRE calculator displays when you enter your income, expenses, and investment timeline. The tool congratulates you: you could retire in eight years if you maintain a 60% savings rate. The catch? This projection relies on assumptions so simplistic they belong more in fairy tales than serious financial planning.

The reality of financial markets bears no resemblance to a smooth curve showing a constant 7% annual return. Economic cycles don't respect your life plans. Inflation doesn't ask permission before eroding your purchasing power. And your life expectancy could well exceed by two decades what you had anticipated filling out that reassuring form.

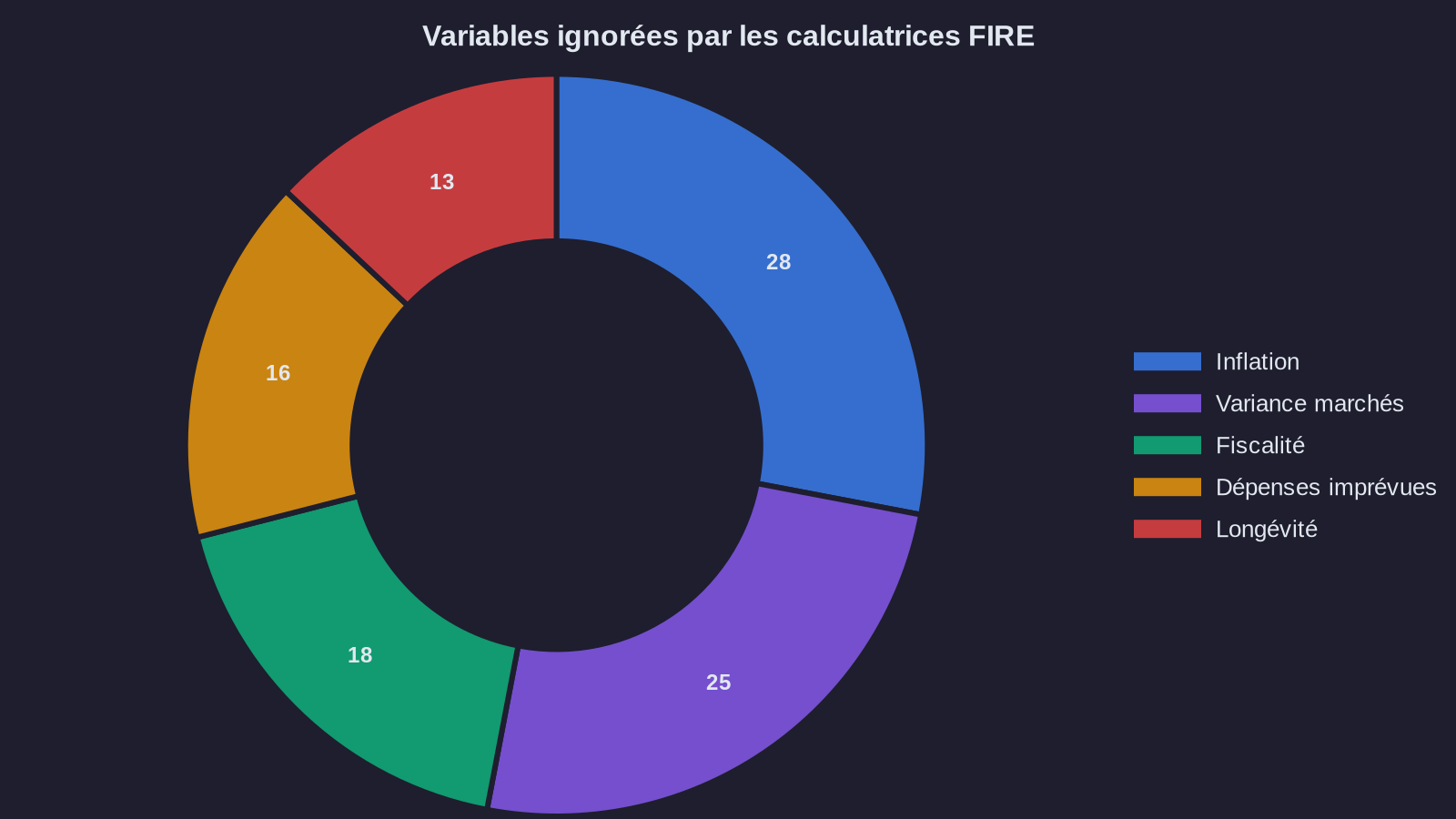

Consumer FIRE calculators systematically overlook several variables that can make the difference between serene financial independence and a forced return to the job market at 55. Let's examine more closely what these calculators deliberately omit, and how to build a retirement planning model that actually holds up.

The myth of constant returns: when variance becomes your worst enemy

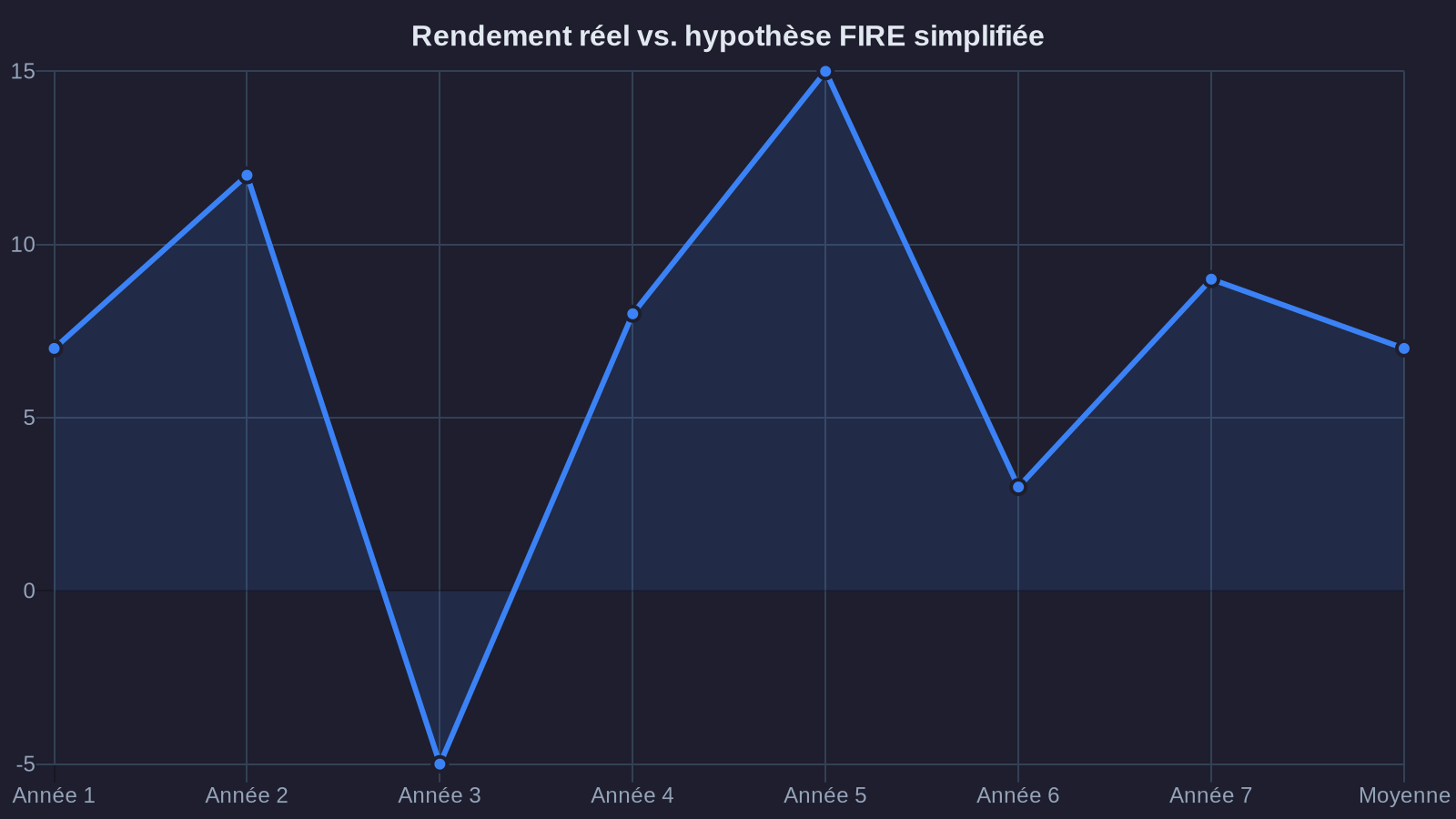

Most FIRE calculators operate on childlike logic: you invest X euros monthly, markets return Y% per year on average, so in Z years you'll have accumulated N euros in assets. This reassuring arithmetic masks a far more complex reality: the order in which returns materialize matters just as much as their average.

Take two investors who save 2,000 euros monthly for ten years. The first sees their investments grow steadily, with 7% returns each year. The second endures five catastrophic years first (returns of -10%, -5%, 0%, 2%, 3%), then five exceptional years (15%, 18%, 12%, 16%, 20%). Over the period, their average return is identical at 7%. Yet in the end, the first investor has amassed several tens of thousands of euros more in assets.

This phenomenon has a technical name: sequence of returns risk. It becomes particularly treacherous in the first years following your early retirement. If markets collapse precisely when you start drawing from your capital, you're forced to sell assets at their lowest point to fund your lifestyle. Your wealth will never recover from this toxic combination: falling prices and forced withdrawals.

Standard calculators completely ignore this dimension. They reason in averages smoothed over decades, as if returns aligned obediently year after year. In the real world, an investor who retired in 2007 had an entirely different experience than someone who left the workforce in 2009, even with identical investment strategies. Timing escapes your control, but its consequences for your wealth are determinative.

Inflation: the variable everyone adjusts too optimistically

Ask any FIRE calculator user what inflation rate they've input into their tool. You'll typically get an answer around 2%, sometimes 2.5%. This figure seems reasonable if you trust historical averages in developed countries over recent decades. It becomes problematic when you project this constant rate over thirty or forty years in a rigorous early retirement FIRE calculation.

First, because inflation is never uniform. A retiree's expense basket doesn't match the consumer price index calculated by statistical institutions. The items that weigh heavily in a senior's budget (healthcare, personal services, quality food) generally experience inflation above average. In the United States, healthcare spending has increased by an average of 5 to 6% annually over the past twenty years—more than double general inflation.

Second, because periods of high inflation do occur. The 1970s saw rates approaching or exceeding 10% in several Western economies. More recently, 2022 reminded many savers that inflation could become a major concern again. Assuming it stays comfortably contained around 2% for forty years is naive optimism.

A common mistake is to adjust your savings target by simply multiplying your annual needs by a constant inflation coefficient. You estimate needing 40,000 euros per year today? Your calculator tells you what capital you need to generate that amount indexed for inflation. But this approach doesn't account for sudden inflationary shocks that may strike precisely at the wrong moment, or the cumulative effect of even a slight underestimation over several decades.

Real inflation of 3% instead of the anticipated 2% reduces your purchasing power by nearly 25% after thirty years. That's not a marginal detail—it's the difference between living comfortably and having to ration expenses. Yet how many simulators actually let you model variable inflation scenarios or test how sensitive your plan is to sustained price increases?

Your retirement duration: the parameter nobody really wants to face

FIRE calculators typically ask at what age you want to retire. Some go further and ask how long you think you'll live. Most users enter a figure around 85-90 years, sometimes less. This comfortable assumption has one major flaw: it systematically underestimates your actual life expectancy.

A healthy 40-year-old man who doesn't smoke and has decent health coverage has a median life expectancy well exceeding 85. For a woman in the same condition, you're looking at closer to 90 years or more. These figures represent medians, meaning you have a 50-50 chance of surpassing them. Planning your retirement based on median life expectancy amounts to betting your financial future on a coin flip.

The question isn't whether you want to live to 95. It's whether your financial plan holds up in that scenario. Adding ten years to your projection doesn't simply translate into a proportional increase in capital needs. Those extra years are typically when healthcare expenses skyrocket, when your ability to generate supplemental income vanishes, and when midcourse corrections become impossible. This reality intersects with the long-term retirement savings challenges facing traditional investors.

Simplistic tools calculate your capital needs using the 4% rule: multiply annual expenses by 25, and you're done. This rule, drawn from William Bengen's work in the 1990s, is based on historical simulations covering retirement periods of thirty years maximum. It was never designed to validate retirements lasting forty-five or fifty years. Mechanically applying this ratio to early retirement at 35 or 40 is reckless extrapolation.

Worse still: the rule assumes you simply consume your capital at a fixed pace, ignoring how your needs vary over time. In reality, your early retirement spending (travel, hobbies, personal projects) differs from your later years. Failing to integrate this variable spending curve means either overestimating your total needs and unnecessarily delaying departure, or underestimating them and facing hardship when medical bills explode.

Building a FIRE calculation model that accounts for real life

If consumer calculators fail to capture real-world complexity, how do you construct a more robust financial projection? The answer isn't some magic tool that gives you the right figure. It's a multi-scenario approach that tests your plan's resilience against probable disruptions.

Start by simulating not one investment path with smoothed average returns, but hundreds of possible trajectories incorporating actual market volatility. Monte Carlo simulations allow you to assess the probability that your capital survives retirement while accounting for year-to-year return variations. A solid plan shouldn't merely work in the median scenario. It must hold up in at least 80 to 90% of cases, including when early-year returns are catastrophic.

Next, integrate multiple inflation profiles. Test a conservative 2% scenario, but add a 3% scenario across the entire period, plus a scenario with sudden spikes to 5-6% followed by returns to normal. Observe how your plan responds when inflation runs hot during the five years right after you leave your job. These stress tests reveal the flaws that smooth averages carefully conceal.

Regarding life expectancy, systematically add ten years to what you consider reasonable. If you think you'll live to 85, plan for 95. This safety margin isn't pessimism—it's elementary prudence. In the worst case, you leave more to your heirs. In the best, you won't find yourself at 90 with depleted capital and no backup plan.

Finally, model your spending realistically. Your needs at 45, freshly retired and in good health, look nothing like those at 75. Many FIRE advocates observe their spending naturally declining with age before rising again in later years due to medical and care costs. Build a three-phase spending curve: active (high discretionary consumption), consolidation (stable, moderate spending), then dependence (rising medical costs). This approach offers a far more accurate picture than the myth of constant inflation-indexed 40,000 euros annually.

Safety margins as guiding principle

You cannot predict the future. Markets will surprise you, inflation will deviate from your projections, and your health will evolve in ways no one can foresee. Faced with this irreducible uncertainty, the only sensible strategy is to build safety margins at every level of your plan.

This means saving more than the optimistic calculator suggests. It requires delaying your departure by a few years if early accumulation returns disappoint. It demands accepting that a robust early retirement FIRE plan is never set in stone—it constantly adjusts to signals from markets, actual inflation, and your own circumstances.

Questions about tax residency in retirement add another layer of complexity that standard calculators ignore entirely. Similarly, integrating alternative assets like cryptocurrencies requires specific thinking about volatility and correlation.

FIRE calculators don't deliberately lie. They oversimplify dramatically to give you a quick, reassuring answer. The problem is that your financial independence isn't built on quick answers. It demands a nuanced understanding of the mechanisms determining your wealth's longevity over decades. Ignoring return variance, downplaying inflation's impact, or underestimating your lifespan transforms your FIRE project into a risky gamble.

Before setting your departure date, take time to test your plan under degraded conditions. Ask yourself if it survives a lost decade in the markets. Verify it withstands persistently high inflation above 3%. Ensure it comfortably funds forty-five years of retirement rather than thirty. If the answer is positive in these adverse scenarios, you have a solid plan. If not, better revise your assumptions now than discover they're flawed in twenty years, when it's too late to course-correct.