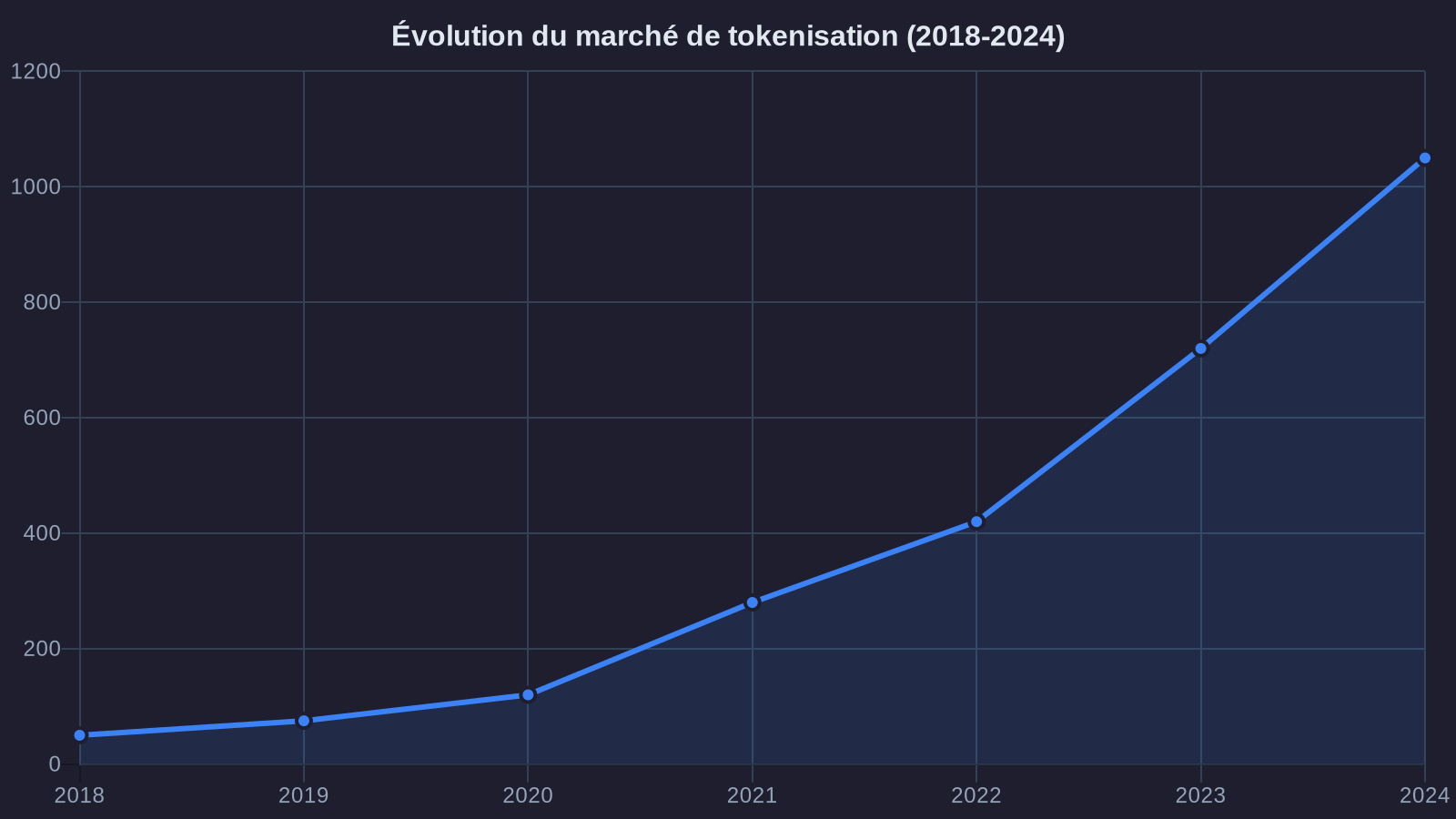

The real-world assets (RWA) tokenization market has just crossed a symbolic milestone: over one billion dollars of real-world assets are now circulating on blockchain. Behind this figure lies a significant shift in the crypto sector. While Bitcoin and Ethereum capture media attention, a less flashy but potentially more transformative segment is taking shape: one that bridges traditional finance and decentralized protocols.

This convergence is nothing new. The first tokenization attempts date back to 2017-2018. But the enthusiasm of that era ran into an unforgiving reality: lack of regulatory framework, virtually nonexistent liquidity, and underestimated operational complexity. Six years later, the landscape has changed. Infrastructure has matured, regulators have set clear guidelines, and crucially, top-tier institutional players are now testing the waters.

For investors seeking to diversify beyond the volatility of pure cryptocurrencies, the question is no longer whether tokenization will take off, but how to position themselves intelligently.

What lies behind the billion in tokenized assets

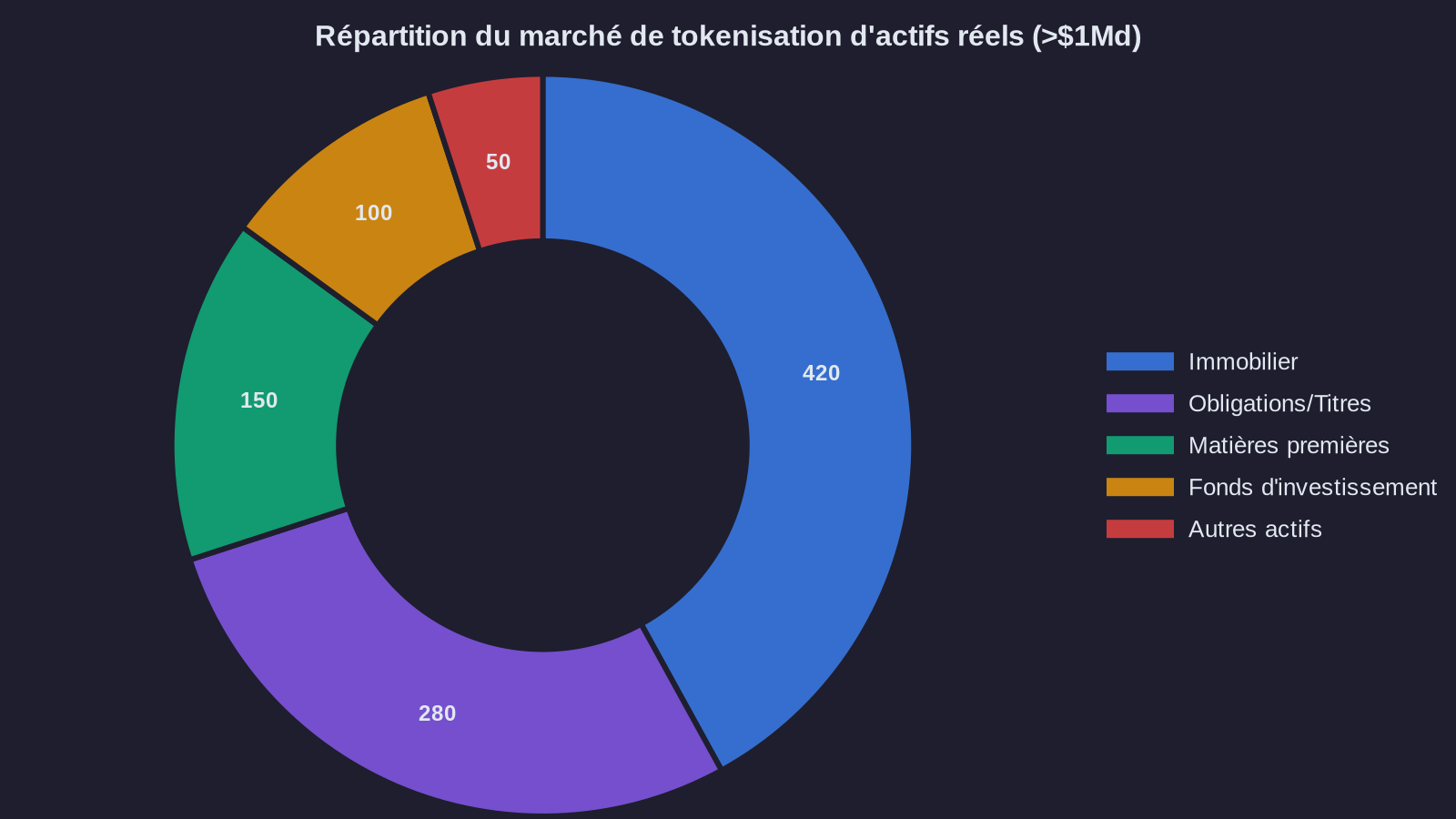

Let's start by clarifying what this one-billion-dollar figure represents. We're talking about traditional assets whose ownership or associated rights are represented by tokens on blockchain. Concretely, this includes several distinct categories.

Tokenized U.S. Treasury bonds take the lion's share, with nearly 700 million dollars according to the latest data. Protocols like Ondo Finance or Franklin Templeton now allow you to buy the equivalent of treasury bonds directly on-chain. The appeal is obvious: combining the risk-free yield of government bonds with the speed and transparency of blockchain. For a stablecoin holder, it's the opportunity to generate yield without leaving the crypto ecosystem.

Tokenized real estate holds the second position, with approximately 200 million dollars. Platforms like RealT or Lofty let you buy fractions of U.S. rental properties for a few hundred dollars. Each token represents an ownership stake in the property and entitles you to proportional rental income. The concept itself isn't revolutionary—REITs have existed for decades. But the on-chain mechanics bring secondary liquidity and transparency impossible with traditional vehicles.

Commodities, carbon credits, and other alternative assets round out the picture. The segment remains experimental, but projects like Paxos Gold (tokenized gold) or certain carbon initiatives show the spectrum is expanding.

What stands out in this distribution is the overwhelming dominance of liquid and regulated assets. The libertarian dream of tokenizing everything—from artworks to startup stakes to vintage cars—hits a simple reality: liquidity concentrates where the legal framework is clear and cash flows are predictable.

The risk-return equation of RWA investing

For an investor accustomed to crypto volatility, tokenized real-world assets present a radically different profile. Take Treasury tokens as an example. The yield follows that of U.S. Treasury bonds, currently around 4 to 5 percent annually. There's no comparison with the flashy promises of certain DeFi protocols. But that's precisely the point.

In a crypto portfolio, these assets serve as ballast. They keep you exposed to the ecosystem while limiting overall volatility. Rather than converting part of your holdings into dollars via an exchange and losing crypto exposure, you can allocate a portion to RWAs that generate stable yields. The trade-off becomes more nuanced: you compare the opportunity cost of staying liquid in stablecoins versus earning 4 to 5 percent with Treasury tokens, versus taking more risk in DeFi liquidity pools.

Tokenized real estate presents a different proposition. Rental yields vary by property, typically between 5 and 10 percent annually. But this introduces specific risks: vacancy, unexpected expenses, local real estate market fluctuations. Tokenization doesn't eliminate these risks; it simply makes them more accessible and transparent. Each token is backed by a physical asset whose existence, rental status, and revenues can be verified. This traceability is progress over certain opaque traditional finance structures.

The real question becomes one of correlation. If you already hold a diversified portfolio of traditional assets, adding tokenized RWAs provides only a form of diversification, not substantive diversification. You remain exposed to the same risk factors, simply through a different infrastructure. Conversely, for a 100 percent crypto-native portfolio, integrating RWAs introduces welcome decorrelation. When the crypto market drops 30 percent in a few weeks, your Treasury tokens quietly continue generating their coupon.

The frictions that remain in real-world asset blockchain

Tokenization promises fluidity, transparency, and fractional ownership. Operational reality is more nuanced. Several frictions persist, which you need to anticipate before positioning yourself.

First friction: regulatory complexity. Most RWA platforms operate under strict regulatory frameworks. This means extensive KYC, geographic restrictions, sometimes lock-up periods. You don't buy a Treasury token the way you swap an altcoin on Uniswap. You need to go through identity verification, wait for validation, respect minimum thresholds. This friction is the price of compliance, but it deters those seeking the instant, pseudonymous access characteristic of DeFi.

Second friction: secondary liquidity remains embryonic. Sure, a token representing a real estate fraction can theoretically be exchanged 24/7. In practice, the order book is often thin. You may find yourself waiting days or weeks to sell your position at an acceptable price. Tokenization facilitates market creation, but it doesn't guarantee market depth. The most liquid assets remain Treasury tokens, supported by protocols that have reached critical mass.

Third friction: counterparty risk doesn't disappear, it shifts. When you hold a token backed by a real estate property, you depend on the issuer to manage the property, collect rents, and distribute revenue. If that entity defaults or turns out to be fraudulent, your token becomes nearly worthless. Blockchain guarantees transaction traceability, not issuer soundness. We're back to classic due diligence—an issue amplified by the sector's youth and the absence of established standards.

Finally, taxation remains a headache. How should income generated by a real estate token be treated? As rental income? As capital gains? Most tax authorities haven't yet ruled clearly. This uncertainty creates a risk of reclassification later. For a professional or institutional investor, this is a major obstacle slowing allocations.

How to invest in tokenized assets today

Faced with these opportunities and frictions, what approach should you take? Several strategies emerge depending on your profile and objectives.

For those primarily seeking to stabilize a volatile crypto portfolio, Treasury tokens are the most obvious entry point. Protocols like Ondo, Mountain Protocol, or Franklin OnChain US Government Money Fund offer liquid and relatively straightforward exposure. Yields track Treasury bond returns, fees are transparent, and liquidity allows you to exit quickly if needed. This allocation might represent 10 to 30 percent of a crypto portfolio depending on risk tolerance. It's the on-chain equivalent of the bond allocation in a traditional portfolio.

For those wanting to explore real estate tokenization, your approach should be more selective. Favor established platforms with multi-year track records, verifiable properties, and full transparency on fees and management. RealT stands as the reference in the U.S. market, with years of operations and hundreds of tokenized properties. Start with small positions to test the mechanics: buying, receiving income, secondary liquidity. Tokenized real estate shouldn't dominate a portfolio, but rather serve as tactical diversification toward uncorrelated yield.

More sophisticated investors can explore protocols that combine RWAs with DeFi. Some projects allow you to use Treasury tokens as collateral to borrow stablecoins, creating managed leverage. Others aggregate multiple RWA types in structured vaults. This approach requires deep understanding of underlying mechanics and smart contract risks, but it opens more elaborate yield strategies.

Whatever your approach, some principles are essential. First, diversify your issuers. Don't concentrate all your RWA exposure on a single platform. Counterparty risk is real, and a problem with one protocol shouldn't wipe out your entire allocation. Second, remain vigilant about transparency. Serious projects publish regular audits, reserve proofs, and details on underlying assets. Any opacity should raise red flags. Finally, maintain a long-term view. RWAs aren't assets to trade daily. Their value lies in stability and regular yields, not speculative appreciation.

The billion is just the beginning for real-world asset tokenization

Crossing the one-billion-dollar mark represents less an arrival than a departure. Projections vary, but several analysts expect 10 to 15 billion dollars in tokenized RWAs by 2025-2026. This growth will be driven by several converging catalysts.

First, growing involvement of traditional financial institutions. When BlackRock launches a tokenized money market fund or Société Générale issues on-chain bonds, the signal is clear: tokenization is no longer a crypto gadget, it's a structural evolution of financial infrastructure. These players bring with them the credibility, volumes, and compliance requirements that pioneers lacked.

Next, improvement in technical infrastructure. Layer 2 solutions, blockchain interoperability, emerging standards (like ERC-3643 for security tokens) facilitate RWA issuance, management, and exchange. Technical frictions decrease, making the user experience comparable to traditional platforms.

Finally, progressive regulatory clarity. Europe with MiCA, the United States with its legal developments, Singapore and other jurisdictions are establishing the rules of the game. Yes, these frameworks are constraining. But they lift the uncertainty that has paralyzed institutional allocations.

For discerning individual investors, the current window presents an interesting balance. The market has matured enough to offer credible and relatively secure options. Yet it remains young enough that yields still compensate for remaining friction and residual risks. In a few years, when tokenization becomes mainstream, these risk premiums will compress.

Real-world asset tokenization won't replace Bitcoin or native DeFi protocols. It occupies a distinct space: that of a bridge between two financial worlds. For those who know how to navigate between regulatory compliance and on-chain opportunities, RWAs offer a pragmatic way to diversify, stabilize, and professionalize their crypto investment approach. The billion crossed isn't an end in itself; it's proof the concept has found market fit. What remains to be seen is how far this trajectory can go.