Imagine being able to lend your cryptocurrencies against US Treasury bonds, or borrow stablecoins by collateralizing shares of commercial real estate. What seemed like science fiction three years ago is becoming reality with Aave V4. The historic DeFi protocol that popularized decentralized lending is making a strategic pivot: it's no longer just about swapping tokens among crypto enthusiasts, but integrating tokenized Real World Assets into the DeFi credit market ecosystem.

This shift goes far beyond a simple technical update. Aave V4 completely reimagines the protocol's architecture to solve a major problem: how to generate sustainable yields when crypto interest rates fluctuate unpredictably? The answer comes down to three words: Real World Assets, or RWA. From government bonds to tokenized corporate invoices, Aave V4 opens the door to a new generation of collaterals. For those looking to generate passive yield on crypto assets, this evolution fundamentally changes the game.

The hub-and-spoke architecture: a paradigm shift

To understand Aave V4's innovation, you first need to grasp the problem it solves. Previous protocol versions operated like isolated markets. You deposited ETH on Ethereum and borrowed USDC on Ethereum. Period. If you wanted to interact with Arbitrum or Polygon, you had to start from scratch on each blockchain.

As Nora explains: It's like having a different bank account in every city you travel to, with no ability to transfer funds between them. You have to withdraw your money, physically carry it, and redeposit it elsewhere. Tedious, expensive, inefficient.

Aave V4 introduces a radically different system, called the hub-and-spoke architecture. The hub is the system's core, deployed on Ethereum. The spokes are the outposts deployed on other blockchains: Arbitrum, Base, Optimism, Polygon, BNB Chain, Avalanche, Gnosis. All these spokes communicate with the central hub via secure bridges.

In practical terms, this means you can deposit USDC on Base, borrow ETH on Arbitrum, and repay from Polygon. Your collateral is no longer fragmented across fifteen different protocols. It forms a single liquidity pool, accessible from any blockchain connected to the hub.

This architecture enables two essential things. First, it drastically reduces costs: you no longer pay bridge fees for every transaction, the protocol pools transfers collectively. Second, it opens the door to specialized markets. Some spokes can focus on classic crypto assets, others on governance tokens, and others still on real-world assets.

Real World Assets enter DeFi credit markets

The real game-changer—the one that makes Aave V4 a strategically important DeFi protocol for institutional investors—is the native integration of RWAs. Until now, DeFi protocols operated in a closed loop: you lent Bitcoin to borrow Ethereum, you used USDC to obtain DAI. Yields depended entirely on supply and demand internal to the crypto market.

The problem? These yields are volatile. When the market is bullish, everyone wants to borrow to speculate, rates skyrocket. When the market declines, no one borrows, rates collapse, and your deposits earn 0.5% per year. It's hard to build a wealth strategy on such unstable foundations.

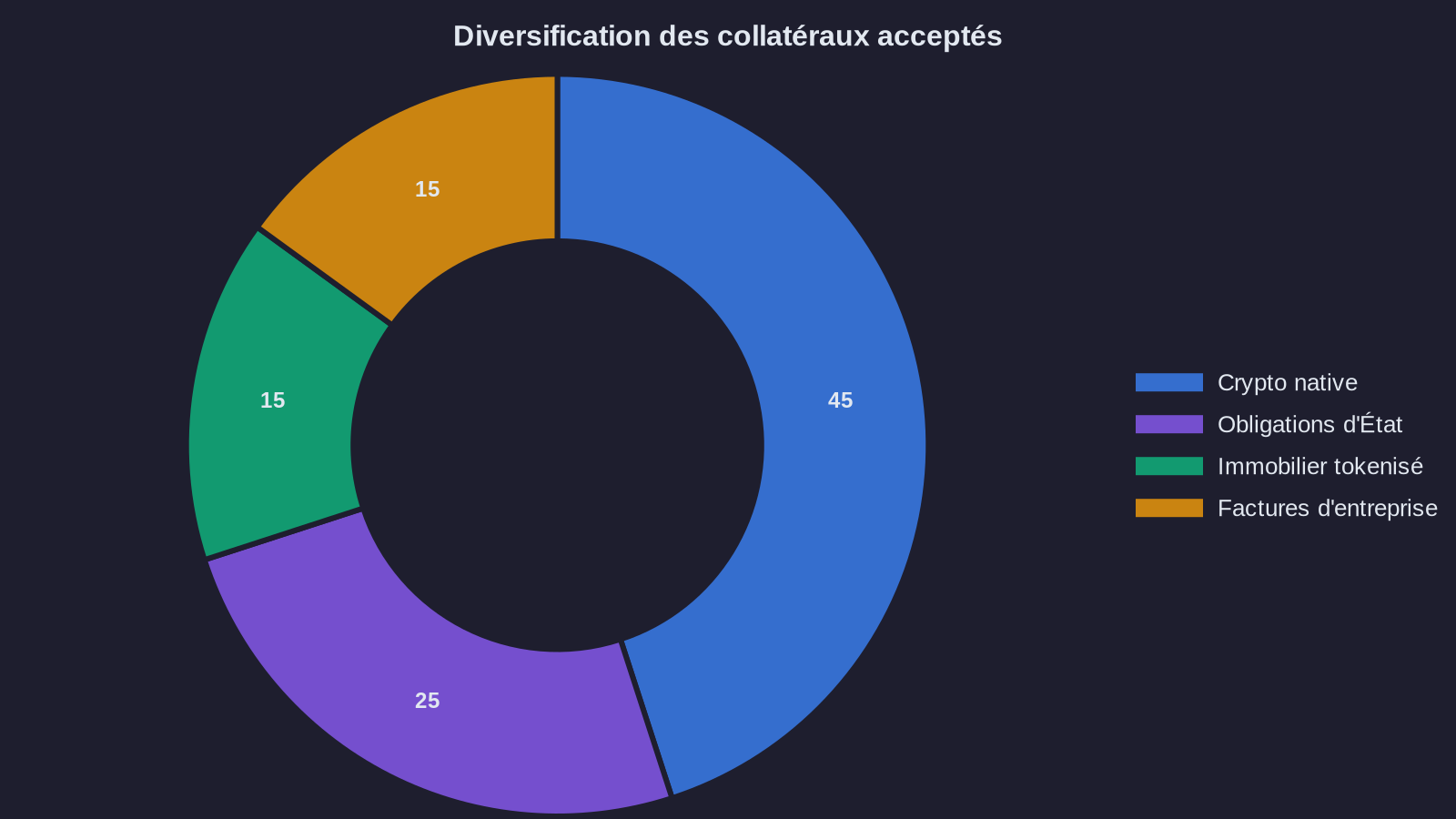

Aave V4 changes things by allowing tokenized real-world assets to be used as collaterals. We're talking about US Treasury bonds (via tokens like OUSG or USDY), corporate bonds, commercial receivables, even tokenized commercial real estate shares. These assets generate predictable yields, indexed to traditional interest rates.

Picture this scenario: you deposit tokens representing US Treasury bonds (current annual yield: around 5%) on Aave V4. The protocol recognizes these tokens as valid collateral. You then borrow stablecoins at 3%. Your net spread: 2% per year, with virtually no volatility. It's not spectacular, but it's stable, predictable, and compatible with rigorous wealth management.

This openness to RWAs answers massive demand. Institutions want to access DeFi's efficiency (instant settlement, transparency, no intermediaries) while maintaining exposure to traditional assets they understand. Aave V4 builds that bridge for them. In a context where crypto asset regulation is clarifying, this convergence between traditional finance and DeFi becomes possible.

Isolated markets: security through segmentation

Integrating RWAs obviously raises a central question: how do you protect the protocol if a tokenized asset turns out to be defective? If a bond issuer goes bankrupt, if a real estate token loses all value, how do you prevent that from contaminating the entire system?

Aave V4 answers with isolated markets. Each asset type with specific risks gets its own compartment. One market dedicated to tokenized Treasury bonds, another to commercial receivables, another to real estate tokens. These markets operate independently: if one collapses, the others aren't affected.

As Nora puts it: It's like a ship with watertight compartments. If one hold springs a leak, you close the doors, isolate the affected compartment, and the rest of the vessel keeps floating. The Titanic taught us that lesson over a century ago.

This modular architecture lets Aave V4 experiment. The protocol can launch a test market with a new tokenized asset, observe its behavior, adjust risk parameters (collateralization ratio, maximum borrowing rate), without endangering the hundreds of millions of dollars already deposited on established markets. This precaution is all the more important after systemic weaknesses exposed by certain DeFi hacks.

For investors, this translates into granular choice. You can decide to participate only in classic crypto markets, with their high but volatile returns. Or you can opt for RWA markets, with their moderate but stable returns. Or mix both, building a diversified portfolio that combines crypto exposure with exposure to traditional interest rates.

The necessary path toward institutionalization of DeFi protocols

You can view Aave V4 as a simple technical evolution. You can also see it as a strategic signal: DeFi is maturing, it's breaking out of its speculative bubble, it's gradually integrating into the traditional financial system. This integration doesn't happen without friction.

RWAs bring stability, but they also bring regulation. A tokenized US Treasury bond remains a regulated financial security. Its issuer must meet compliance obligations: beneficial ownership identification (KYC), tax reporting, international sanctions compliance. Aave V4 must navigate these constraints.

The protocol made modularity its solution for precisely this reason. Pure crypto markets remain permissionless: anyone can participate, without identification, with just a wallet. RWA markets, however, can integrate compliance layers. The issuer of a real estate token can require KYC before authorizing its use as collateral. Aave V4 merely provides the infrastructure; each market sets its own access rules.

This hybrid model is probably DeFi's future. A common, decentralized, transparent technical foundation on which variable compliance layers are added based on assets. Purists will see it as a betrayal of founding principles. Pragmatists will see it as a necessary condition to unlock the trillions of dollars in traditional assets still waiting to be tokenized.

Key takeaways

1. The hub-and-spoke architecture unifies Aave's liquidity: you can now manage your positions from any connected blockchain, without multiplying deposits or paying prohibitive bridge fees.

2. Real World Assets become first-class collaterals: Treasury bonds, corporate bonds, tokenized commercial receivables can now be deposited on Aave to generate stable yields indexed to traditional rates.

3. Isolated markets protect the protocol: each asset type with specific risks gets its own compartment, preventing a default from contaminating the entire system.

Aave V4 isn't a spectacular revolution. It's a methodical evolution, designed to last. The protocol that invented flash loans and democratized decentralized lending is now entering a new phase: progressive institutionalization. Returns may be less exciting than during the DeFi summer of 2020, but they'll be more sustainable. And in asset management, sustainability often matters more than hype.