One hundred million euros. Not a funding round for a promising crypto startup. This is the amount Amundi, Europe's leading asset manager, just deployed on Ethereum through the tokenization of a money market fund. For a player managing over 2 trillion euros in assets, this figure may seem modest. Yet this tokenization of a EUR 100 million fund on Ethereum marks a major strategic turning point: institutional finance is no longer testing blockchain, it's integrating it into its operational infrastructure.

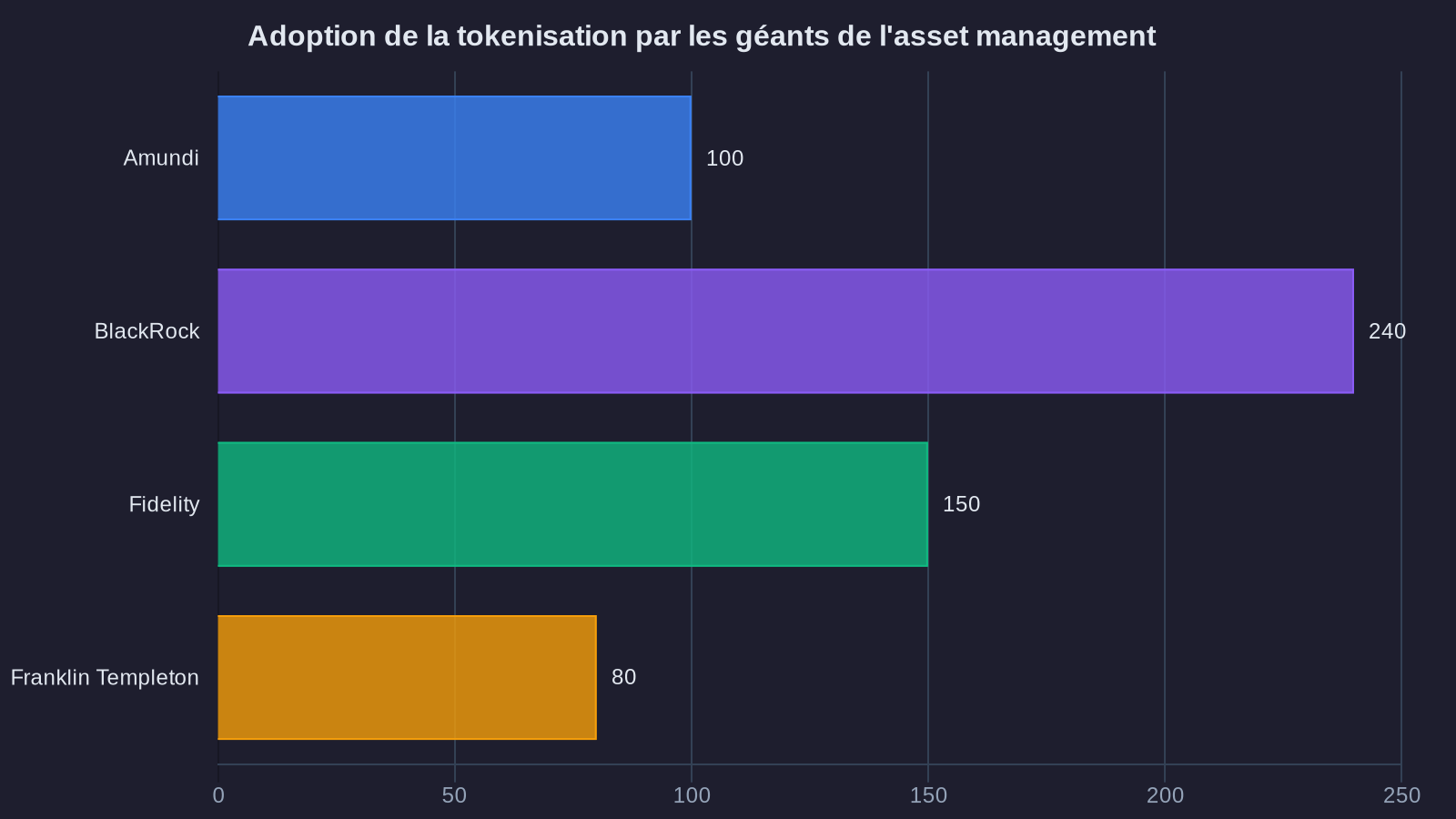

This initiative is part of a broader movement toward blockchain asset adoption by institutions. BlackRock, Fidelity, Franklin Templeton: asset management giants have been multiplying tokenization projects since 2023. But Amundi goes further by choosing Ethereum, a public network, rather than a private or consortium blockchain. This technical choice reveals a strategic vision that transcends simple back-office optimization.

Institutional tokenization: far more than digital compliance

Imagine you own a house. Traditionally, to sell it, you go through a notary, paper deeds, and several weeks of waiting. Tokenization is like dividing that house into thousands of small digital property certificates, each representing a fraction of the asset. These certificates can be exchanged instantly, 24/7, with complete traceability and reduced transaction costs.

For an Amundi tokenized fund like this one, the promise is twofold. First, increased operational efficiency: settlement of fund shares can happen in minutes instead of two business days. Intermediaries are reduced, management costs decrease mechanically. But that's only the visible part.

The real revolution lies in programmable liquidity. A token on Ethereum can embed compliance rules directly into its code: geographic restrictions, automated KYC controls, investment caps. This is what's called a smart contract. Result: you can distribute a complex financial product to an international client base without multiplying manual regulatory layers. This secure approach contrasts with potential vulnerabilities in individual wallets, where security relies on the end user.

Ethereum adoption: why a public blockchain instead of a private one

The question regularly resurfaces in investment committees: why take the risk of a public blockchain when you can build your own private network, controlled end-to-end? Amundi could have opted for a Hyperledger solution or a European banking consortium. The choice of Ethereum is not trivial and illustrates growing Ethereum adoption by institutions.

A private blockchain is like a corporate intranet: fast, secure, but closed. You control everything, but you're also isolated. Ethereum is like the Internet: an open, standardized network with a mature ecosystem of technical service providers, security auditors, and interoperable protocols. This standardization changes the game.

In practical terms, a tokenized fund on Ethereum can be integrated with third-party trading platforms, connected to institutional lending protocols, or used as collateral in financing operations. Impossible with a proprietary blockchain. You move from an isolated asset to a composable asset—one that can be used as a building block in other financial products.

There's also a cost logic. Developing and maintaining a private blockchain infrastructure represents a significant technical investment. Leveraging Ethereum means externalizing the infrastructure layer to a network secured by thousands of independent validators. System resilience is no longer your exclusive responsibility.

Implications for the DeFi ecosystem and institutional tokenization

Amundi's arrival on Ethereum is not merely a technical migration. It marks the convergence of two previously parallel universes: decentralized finance (DeFi) and traditional regulated markets.

Since 2020, DeFi has developed an infrastructure for lending, trading, and asset management entirely on-chain. But these protocols operated essentially with native crypto-assets (ETH, stablecoins) or synthetic assets. Real-world assets (stocks, bonds, fund shares) remained outside the scope. With institutional tokenization like Amundi's, this boundary dissolves.

Now you can envision concrete operational scenarios: an institutional investor depositing Amundi tokens as collateral to borrow stablecoins on Aave. A corporate treasury optimizing its working capital by automatically placing excess funds in a tokenized money market fund, with instant settlement. A family office building a multi-asset portfolio combining tokenized ETFs, on-chain government bonds, and DeFi positions, all from a single interface. These passive income generation strategies become accessible to institutions through tokenization.

This convergence also raises governance and regulatory questions. DeFi protocols operate according to rules coded into smart contracts, with no central authority. Amundi's funds remain subject to the UCITS directive, with strict fiduciary obligations. How do these two logics coexist? The answer comes through technical safeguards: whitelists of authorized addresses, compliance controls embedded in smart contracts, circuit breaker mechanisms in case of market anomalies.

Next steps: from experimentation to infrastructure

One hundred million euros is a signal. But for tokenization to become a market standard, several barriers still need to fall.

The first is regulatory. The European MiCA regulation (Markets in Crypto-Assets) is gradually coming into effect, but only covers part of tokenized financial instruments. The DLT Pilot Regime allows for experiments but remains limited in scope. For mass adoption, we'll need a harmonized framework that recognizes the legal validity of a token as a representation of a financial security, with the same protections as a traditional certificate.

The second barrier is technical. Ethereum can process roughly 15 transactions per second on its main layer. Insufficient to absorb the settlement volume of the entire European bond market. Scalability solutions (rollups, sidechains) exist, but add a layer of complexity. The path to infrastructure capable of supporting institutional volumes under real conditions remains long.

Finally, there's the issue of interoperability. If each asset manager tokenizes its funds on a different blockchain (Ethereum, Polygon, Avalanche, Solana...), we'll recreate the silos we claimed to eliminate. The industry will need to converge on common standards, both on technical protocols and data formats. Initiatives like the Token Taxonomy Framework or the work of the ISSA (International Securities Services Association) point in this direction, but remain embryonic.

Amundi won't be alone for long. BNP Paribas, Société Générale, DWS: announcements of tokenization projects are multiplying. The question is no longer if traditional finance will shift to blockchain, but how quickly and on what terms.

Key takeaways on this institutional tokenization

Amundi's initiative confirms three structural trends. First, tokenization is moving from proof-of-concept stage to operational deployment with significant volumes. Second, institutional players favor public blockchains for their standardization and composability, despite regulatory constraints. Third, the boundary between DeFi and traditional finance is becoming increasingly porous, opening the door to hybrid products that combine on-chain efficiency and regulatory compliance.

For asset management professionals, this is a clear signal: mastering blockchain infrastructure becomes a strategic competency, on par with risk management or tax optimization. For investors, it's an opportunity to rethink asset allocation by integrating instruments previously inaccessible or illiquid.

The coming decade will likely see the emergence of a new generation of financial products: funds that adapt in real time to market conditions, bonds that automate their coupons via smart contracts, portfolios that rebalance autonomously according to predefined rules. Amundi, by deploying 100 million on Ethereum, is not testing a technology. It's laying the first stones of an infrastructure that will redefine how capital flows.