In February 2025, Circle froze over $270 million in USDC following the Drift platform hack. A decision made within hours. For some, it's reassuring: an issuer capable of reacting quickly to limit damage. For others, it's proof that a centralized stablecoin remains an asset that someone can block whenever they decide.

This situation raises a strategic question for any investor using stablecoins: how much dependence on a central entity are you willing to accept? And more importantly, what are the credible DeFi alternatives when you're looking to position yourself in decentralized yield strategies?

What actually happened with the USDC freeze

On February 20, Drift Protocol, a perpetual trading platform on Solana, suffered an attack. Hackers managed to extract approximately $270 million. Circle, the USDC issuer, immediately froze the stolen tokens to prevent their conversion or laundering.

On paper, this is exactly what you'd expect from a responsible issuer. Circle has the technical means to blacklist certain addresses and render the tokens they hold unusable. This capability has actually been built into the USDC smart contract from the start.

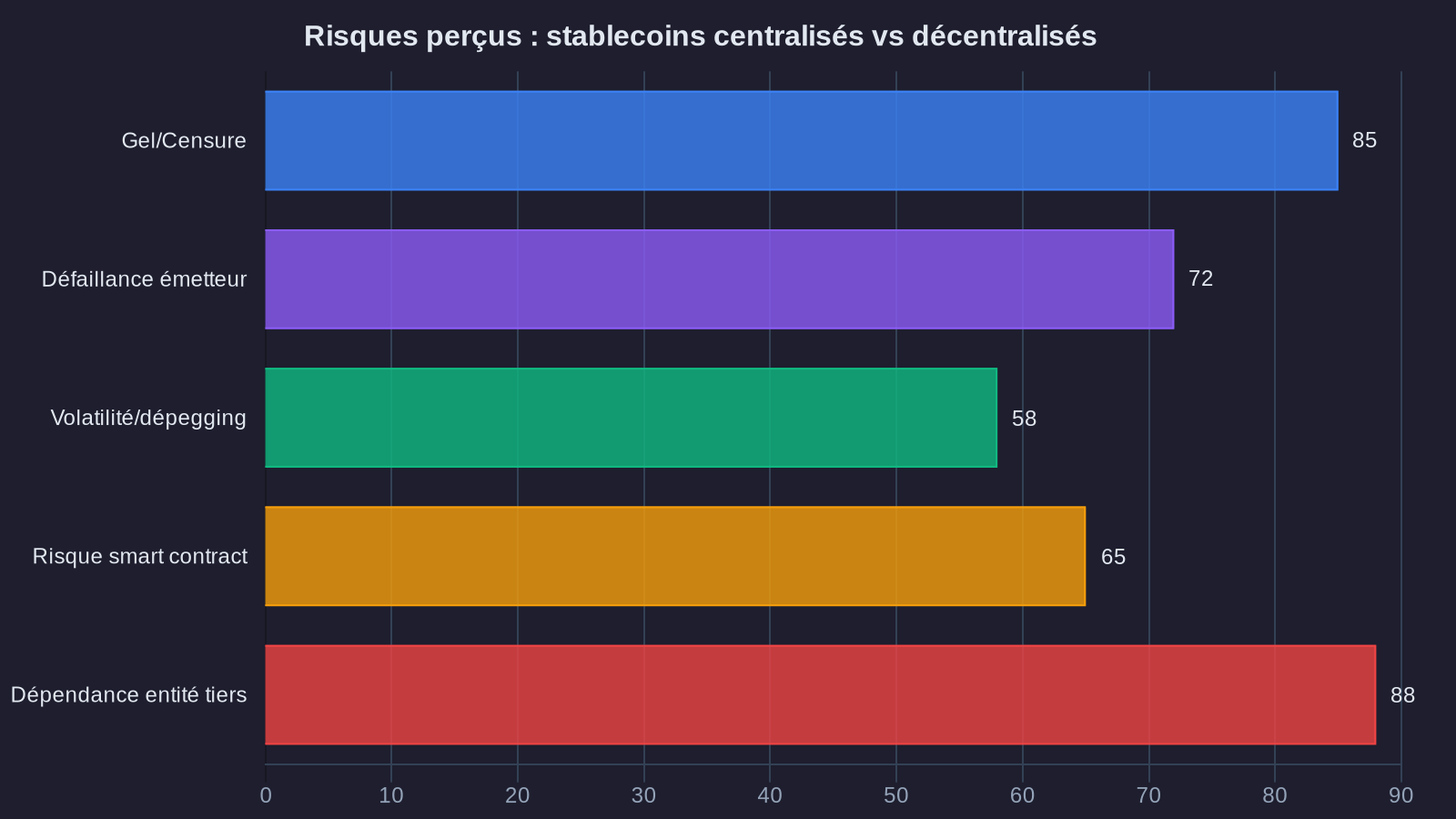

But this intervention highlights a fundamental tension in centralized stablecoin governance. On one hand, it protects the ecosystem against a malicious actor. On the other, it's a reminder that a centralized stablecoin isn't a neutral, immutable asset. Circle can freeze your USDC if an authority demands it, if a court orders it, or if the company determines an address is compromised.

For an institutional investor or treasury manager, this intervention capability isn't necessarily a problem. It might even be reassuring within a regulated framework. But for those seeking to break free from traditional intermediaries, it's a major friction point. This central censorship risk has increasingly become a legal argument in regulatory debates around DeFi.

Why centralized stablecoins still dominate

Despite these limitations, USDC and USDT together represent over 80% of stablecoin market capitalization. This dominance isn't accidental. It rests on three concrete pillars:

Liquidity. You can swap millions of USDC in seconds on any major platform with minimal slippage. This market depth is irreplaceable for structuring yield strategies or managing large flows.

Operational simplicity. USDC is backed 1:1 by dollar reserves and short-term U.S. Treasury obligations, regularly audited. No need to understand complex collateralization mechanisms or monitor solvency ratios. It's a reliable tool for someone who just wants to stabilize a position without complications.

Integration. Almost every DeFi protocol accepts USDC. Fiat ramps support it. Centralized exchanges treat it as a reference currency. This ubiquity creates a network effect that's hard to challenge.

But this convenience comes at a price: dependence on a single entity. Circle is an American company subject to U.S. law. If regulations change tomorrow, if an investigation targets certain user types, USDC could become a control tool rather than a neutral asset.

Decentralized alternatives: DAI, LUSD, and newcomers

Facing this reality, several protocols have built stablecoins without a central intermediary. The idea: create a synthetic dollar whose value is maintained by algorithmic mechanisms and on-chain guarantees, not by a bank reserve.

MakerDAO's DAI: the pioneer under pressure

DAI was the first decentralized stablecoin to reach significant scale. The principle: you deposit crypto-assets as collateral (ETH, wBTC, stETH…), and you borrow DAI in return. If your collateral loses value, the protocol automatically liquidates your position to maintain system solvency.

It's a solid model, tested since 2017. But MakerDAO has progressively integrated real-world assets into its collateral: U.S. Treasury bonds, tokenized receivables. Result: today, over 50% of DAI's collateral relies on assets controlled by centralized entities.

This evolution stabilized the peg and improved yields for DAI holders. But it dilutes the original promise of independent blockchain governance. DAI is no longer truly decentralized in practice. It's a hybrid—more resilient than USDC against direct censorship, but not immune to regulatory pressure on its off-chain collateral.

LUSD: pure decentralization, with its constraints

Liquity took the opposite approach with LUSD. This stablecoin is collateralized solely by ETH, with a minimum ratio of 110%. No real-world assets, no centralized governance, no protocol upgrades possible. LUSD is immutable by design.

This radicalism has a cost. LUSD has less liquidity than DAI or USDC. It's less integrated into DeFi protocols. And most importantly, its collateralization model requires heavy overcollateralization, which limits capital efficiency.

For an investor seeking to maximize yield while maintaining flexibility, LUSD might seem too rigid. But for someone wanting a stablecoin truly resistant to censorship, it's one of the few credible options.

New models: GHO, crvUSD, USDe

Other protocols have launched their own stablecoins in recent months, each with a different angle.

GHO, developed by Aave, allows users to borrow a stablecoin directly via collateral deposited on the platform. The advantage: native integration into one of the most widely used lending protocols. The drawback: GHO depends entirely on Aave governance, making it a semi-centralized stablecoin.

crvUSD, launched by Curve, uses a soft liquidation mechanism that progressively adjusts collateral if price drops, rather than liquidating brutally. It's an interesting innovation to limit losses during volatility. But again, the protocol remains controlled by a DAO, with all the governance risks that entails.

USDe, offered by Ethena, relies on a completely different model: a delta-neutral stablecoin backed by short perpetual positions. The idea is to maintain the peg not through static collateral, but through dynamic hedging strategy. It's promising, but still young and less proven than classical models.

How to rethink your stablecoin strategy in light of freeze risks

So, what should you do concretely when managing a stablecoin allocation? There's no single answer, but several thinking points to adjust your positioning based on your risk profile.

Diversify across multiple stablecoins. Don't put 100% of your treasury in USDC. Spread across USDC, DAI, and possibly LUSD or GHO. This diversification limits your exposure to a single freeze or depeg risk. Yes, it complicates operations a bit. But it's the price to pay for reducing counterparty risk.

Prioritize protocols that accept multiple stablecoins. When you structure a DeFi yield strategy, verify that the protocol doesn't depend solely on USDC. If a liquidity pool accepts DAI, USDC, and LUSD, you can switch between assets without redoing everything. This flexibility becomes a strategic advantage in a crisis.

Accept slightly lower yields for greater resilience. Decentralized stablecoins often offer marginally lower yields than USDC, due to less equivalent liquidity. But this discount can be viewed as insurance premium. You're paying an opportunity cost to reduce censorship or freeze risk.

Monitor regulatory developments. Centralized stablecoins will face increasing oversight. MiCA in Europe, discussions around federal frameworks in the U.S.… These regulations can change the rules overnight. An issuer like Circle could be forced to block certain addresses or use cases. Stay informed to anticipate these shifts.

What this means for discerning investors

The freeze of USDC following the Drift hack isn't an isolated event. It's a reminder that in the crypto ecosystem, asset neutrality is never guaranteed by default. It must be built through protocol design, the nature of collateral, and the absence of centralized control points.

For an investor structuring decentralized yield strategies, this reality demands a trade-off. Either you prioritize the liquidity and operational efficiency of centralized stablecoins, accepting the USDC freeze risk. Or you sacrifice some convenience for resilience, diversifying toward alternatives like DAI, LUSD, or newcomers.

There's no right or wrong answer. But there's a question you must ask yourself: at what point does convenience become a vulnerability?

The Drift incident shows that this moment can arrive faster than you think. And when it does, anticipating is better than improvising.