In November 2024, several U.S. Congressional members opened accounts on Polymarket and Kalshi. Officially, to "understand these new financial technologies." Unofficially, some placed massive bets on political events whose outcomes they already knew. The scandal broke when blockchain researchers traced the flows and identified troubling patterns: positions opened hours before official announcements, systematic gains on legislative resolutions, abnormally high volumes on niche markets. What's emerging today is a crucial debate about regulating prediction markets and their vulnerability to insider trading.

The problem isn't new. For years, American elected officials have been able to buy shares in companies they're supposed to regulate. But with crypto prediction markets, manipulation becomes traceable, instantaneous, and public. What was once hidden in opaque stock portfolios now appears in plain sight on a blockchain. Result: Washington finds itself forced to legislate on a form of insider trading it had carefully ignored until now.

How prediction markets work: transparency that unsettles

Unlike traditional stock exchanges, platforms like Polymarket or Kalshi allow you to bet on virtually any event: election results, the timing of interest rate hikes, the outcome of a parliamentary vote. The mechanism relies on liquidity pools where users buy "yes" or "no" positions on a given prediction. If the event occurs, you receive one dollar per position purchased. Otherwise, you lose your stake.

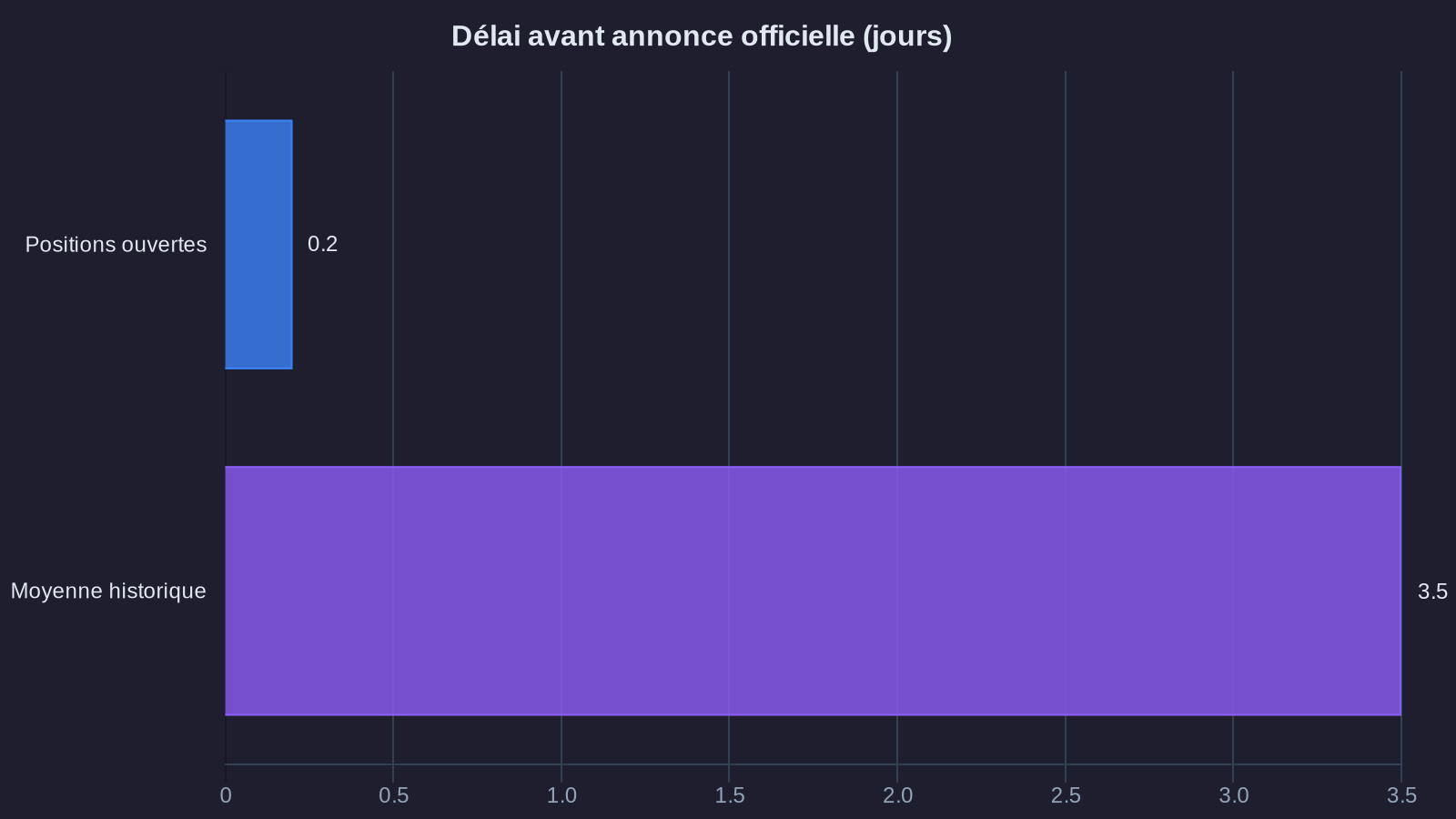

What makes these platforms dangerous for those holding privileged information is precisely their transparency. Every transaction is recorded on-chain. Addresses, even pseudonymous ones, can be linked to real identities through cross-referencing. When a wallet accumulates large positions betting "yes" on a specific legislative vote, and that vote passes just days later, blockchain analysts ask questions.

This is exactly what happened in December 2024. A group of Republican lawmakers bet substantial sums on the adoption of a tax amendment concerning crypto assets. The amendment passed by one vote. Combined gains exceeded $800,000. The matter was revealed by Chainalysis, which published a report documenting the flows with surgical precision. Impossible to deny. Impossible to claim ignorance.

The current legal gap: a STOCK Act that doesn't cover crypto assets

Since 2012, the STOCK Act (Stop Trading on Congressional Knowledge) theoretically prohibits Congressional members and their staff from speculating based on information obtained in their official capacity. But the text targets exclusively traditional securities: stocks, bonds, listed derivatives. Decentralized prediction markets fall into none of these categories, creating a blind spot in American insider trading regulation for crypto.

Section 21A(a) of the Securities Exchange Act of 1934, which defines insider trading, mentions neither crypto assets nor prediction contracts. Result: an elected official can legally bet on the outcome of a vote they know will pass, as long as they don't use a financial instrument regulated by the SEC. It's a gaping legal loophole that some have exploited without restraint.

The CFTC (Commodity Futures Trading Commission), which regulates Kalshi, did attempt to impose restrictions. But its jurisdiction covers only derivative contracts on commodities. Polymarket, based abroad and operating on blockchain, completely escapes its reach. As for the SEC, it focuses on tokens it deems to be securities, not on prediction markets themselves.

This ambiguity created a gray zone where privileged information circulates freely, as long as it doesn't directly touch a Nasdaq-listed stock. But recent scandals have changed things. American citizens, already fed up with their elected officials' privileges, discovered that some were literally betting on their own political decisions. Media pressure became unbearable.

Proposals under discussion: the PREDICT Act versus decentralized markets

Two bills are currently being debated in Congress. The first, filed by House Democrats, proposes an outright ban for all elected officials and their direct staff from participating in prediction markets, regardless of platform used. The text extends the STOCK Act definition to include "any prediction contract, any centralized or decentralized market allowing speculation on a future event." Penalties are severe: up to five years in prison and full confiscation of gains.

The second proposal, backed by Senate Republicans, takes a more nuanced approach. Rather than a total ban, it imposes a public disclosure requirement within 48 hours of any position taken on a prediction market. Officials would have to publish the amount wagered, the prediction involved, and the platform used. For gains exceeding $10,000, written justification would be required. The idea is to maintain investment freedom while making any manipulation visible and politically sanctionable.

Both texts also provide for creating a public registry of elected officials' crypto transactions, managed by the Office of Congressional Ethics. This registry would aggregate declared blockchain addresses and allow real-time monitoring by independent organizations. Technically, it's feasible: several companies already offer on-chain analysis tools capable of tracing flows with redoubtable precision.

The impact on platforms: toward mandatory political KYC?

Polymarket and Kalshi didn't wait for regulators to respond. Kalshi, regulated by the CFTC, announced in January 2025 the implementation of enhanced verification procedures for anyone holding political office. Concretely, U.S. elected officials and their direct staff will need to declare their status upon registration. Their positions will then be automatically made public, with a 24-hour delay.

Polymarket, on the other hand, is resisting. The platform, decentralized and based in the Bahamas, refuses for now any form of political KYC. Its position is simple: "We are not subject to American law. Our users are free to bet anonymously as long as they respect our terms of service." But this strategy is becoming untenable. Several U.S. states have already threatened to block access to the platform if it doesn't cooperate with authorities, illustrating tensions between decentralization and regulatory framework.

The real issue is regulators' ability to impose rules on decentralized protocols. If an official uses a non-custodial wallet and goes through a VPN, how do you identify them? How do you prove an Ethereum address belongs to a specific person? The tools exist – on-chain data cross-referencing, pattern analysis, fiat flow tracking – but their use raises privacy and proportionality questions.

Some experts propose a hybrid solution: require platforms to implement an automatic flagging system. When an address accumulates large positions on sensitive political events, it would be automatically reported to competent authorities. Not systematic KYC, but targeted surveillance of suspicious behavior. This is the model used by traditional banks for anti-money laundering. It could work here too.

The warning point

If you use prediction market platforms like Polymarket or Kalshi, know that your transactions are traceable, even if you think you're operating anonymously. Blockchain analysis tools can link addresses to real identities through data cross-referencing. If you possess non-public information likely to influence the outcome of an event you're betting on, you could face insider trading charges, even if these platforms aren't yet formally regulated as traditional financial markets.

For elected officials and political staff, the situation is even more risky. Even absent an explicit law prohibiting these practices, internal Congressional ethical rules may apply. Several lawmakers have already faced investigations by the Office of Congressional Ethics for transactions deemed contrary to public ethics, without any criminal law being violated. Political consequences can precede legal ones.

Keep all supporting documents for your positions: dates, amounts, investment rationale. Should you need to justify yourself to authorities, you'll need to prove your position was based on public information. If in doubt, consult a lawyer specializing in financial markets law before opening a significant position on a political or regulatory event.

What this affair reveals about crypto regulation to come

The Polymarket scandal marks a turning point in prediction market regulation in the United States. For the first time, American regulators face a type of manipulation they can't ignore because it's public, documented, and politically explosive. Unlike classic insider trading on securities, which requires lengthy investigations and hard-to-obtain evidence, on-chain transactions provide a permanent and verifiable record.

This use case could accelerate implementation of a comprehensive regulatory framework for crypto assets. If elected officials themselves are caught red-handed thanks to blockchain transparency, it becomes politically impossible to continue claiming these technologies escape regulation. We can expect the pending texts to be voted quickly, with rare bipartisan support in Washington.

But beyond the political aspect, this matter raises a fundamental question: how do you regulate decentralized protocols without recreating the centralized control structures that crypto was supposed to transcend? The solution probably won't come from an outright ban, but from a combination of mandatory transparency, automated monitoring, and dissuasive sanctions. A model that could apply well beyond just prediction markets.