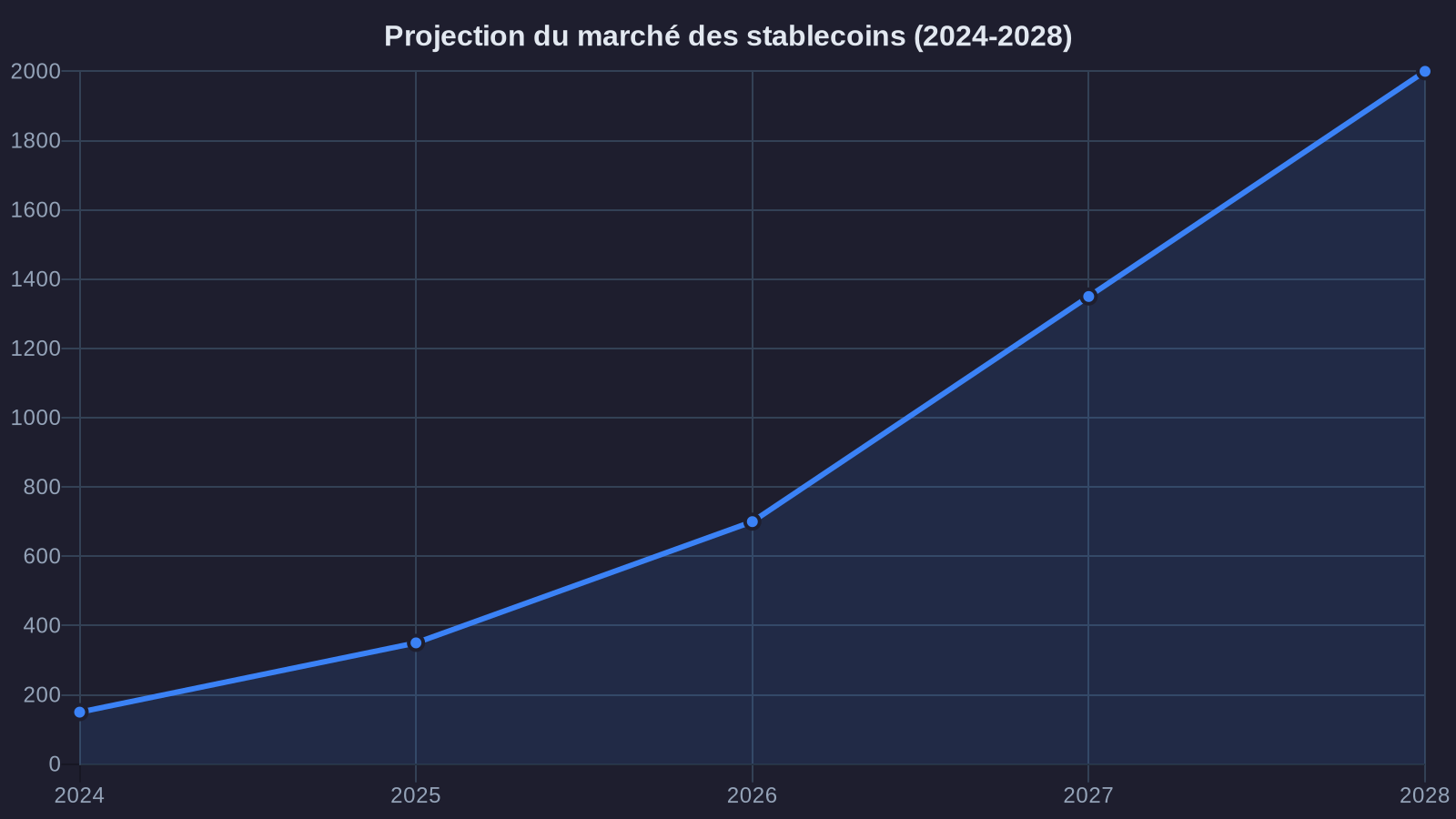

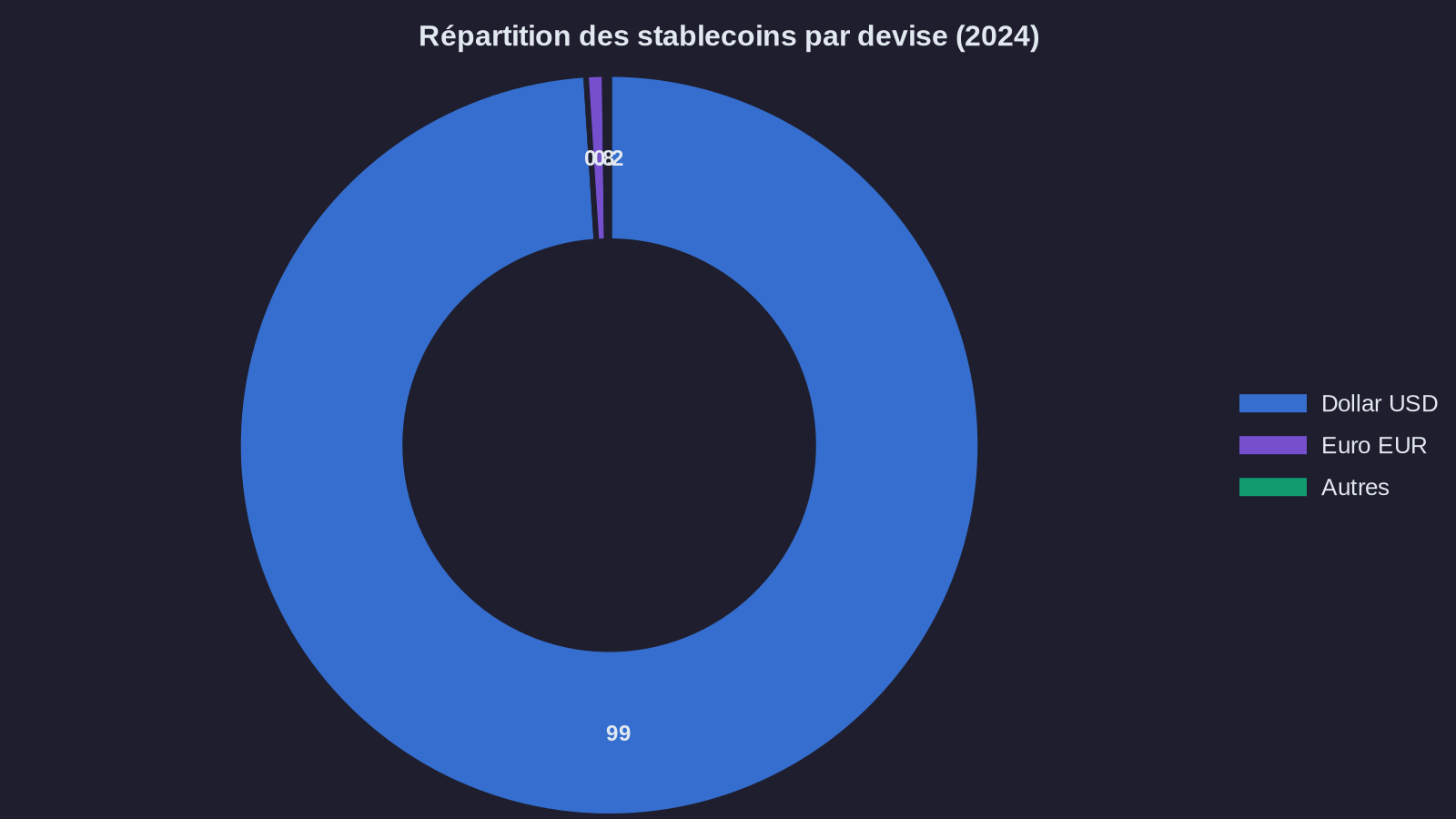

The stablecoin market could reach 2 trillion dollars by 2028. To put that in perspective: that's equivalent to Italy's entire GDP circulating in digital currency backed by the US dollar. Today, 99% of stablecoins are denominated in dollars. The euro represents less than 1% of the market.

This asymmetry is far from trivial. It outlines the contours of a global financial infrastructure where Europe watches from the sidelines as the digitalization of dollar supremacy unfolds. Except something changed late in 2024. Twelve major European banks announced their entry into the euro stablecoin market. Not in five years. Now.

The MiCA regulation (Markets in Crypto-Assets), which came into effect in December 2024, creates Europe's first comprehensive legal framework for crypto-assets. You read that right: comprehensive. While other jurisdictions are still debating definitions, Europe is imposing capital, transparency, and reserve rules that apply to all issuers operating on its territory. This stablecoin regulation under MiCA completely redraws the European landscape.

MiCA: what the text really says about stablecoins

The MiCA regulation distinguishes two categories of stablecoins, which it names "asset-referenced tokens" (ART) and "e-money tokens" (EMT). The difference is structural for understanding MICA compliance.

EMTs are backed exclusively by fiat currency, at a 1:1 ratio. Concretely: a euro stablecoin issued under this regime must be guaranteed by euros held in separate accounts or in high-quality sovereign debt securities. Article 48 of the MiCA regulation requires that these reserves be held with licensed credit institutions and that their valuation be attested every six months by an external auditor.

ARTs, on the other hand, can be backed by a basket of assets (multiple currencies, commodities, etc.). The text subjects them to even stricter capital requirements: Article 35 provides for a minimum initial capital of 350,000 euros, compared to 150,000 euros for EMTs. Why? Because the risk of the promised value decoupling from the actual value is structurally higher.

But the truly disruptive point of MiCA is found in Article 22. It introduces a safeguard clause: if a stablecoin is deemed "of significant importance" (threshold set at 1 billion euros in outstanding volume or more than 10 million users), the European Banking Authority (EBA) can impose additional requirements on it, including limiting its issuance volume or requiring additional capital. Translation: Europe gives itself the means to prevent a non-European stablecoin from becoming systemic on its territory without regulatory oversight. An approach that contrasts with US regulation still fragmented between the SEC and CFTC.

Why twelve European banks are moving now

Société Générale, BBVA, Deutsche Bank, Santander. These names don't appear in a joint press release, but in a series of announcements spread between September and December 2024. What they have in common is that they've all launched or accelerated euro stablecoin projects, backed by their banking infrastructure. This is the concrete illustration of European banking crypto in action.

The timing is no accident. MiCA creates a window of opportunity that these institutions identified with rare strategic convergence. First, the regulatory framework is finally in place. For years, legal risk prevented any serious initiative: which CFO would accept deploying hundreds of millions of euros into an infrastructure whose legal status could flip overnight? MiCA eliminates that uncertainty.

Second, European banks have a structural advantage: they already hold banking licenses, KYC (identity verification) processes, and relationships with regulators. Article 58 of MiCA explicitly allows credit institutions to issue EMTs without an additional license, provided they comply with reserve and transparency requirements. In other words: a bank can launch a euro stablecoin in a few months, whereas a new entrant will need two years to go through the authorization process.

Third, the market is mature. Cross-border payment volumes in stablecoins exceeded 27 trillion dollars in 2024, according to Chainalysis. Corporate treasurers are beginning to use them to streamline their foreign exchange operations and reduce settlement delays. But 99% of these flows pass through dollar-denominated stablecoins issued by American entities (Tether, Circle). A European company settling a payment to an Asian supplier in USDC suffers a double conversion: euros to dollars, then dollars to local currency. The cost of this friction is estimated between 1.5% and 2.5% of each transaction amount.

European banks understand: whoever lays the rails for euro payments will capture structural rent for decades. This isn't a race for innovation's sake. It's an infrastructure battle, comparable to the one being waged by institutional players like Amundi on asset tokenization.

The monetary sovereignty issue nobody names

There's an asymmetry rarely mentioned in stablecoin debates: surveillance capacity. When a dollar-denominated stablecoin circulates massively in Europe, every transaction generates exploitable metadata. Who pays whom, for what, how often, in which geography. This data is far from trivial. It maps in real time the commercial flows, supply chains, consumption patterns.

Article 68 of MiCA imposes on stablecoin issuers a reporting obligation to the EBA, including issuance volume, number of users, and geographic distribution of transactions. But this obligation only applies to issuers subject to European law. An American issuer operating through decentralized channels can technically escape this obligation while capturing the data from millions of European transactions.

This point goes beyond the technical framework. It touches on Europe's capacity to know, understand, and regulate the economic flows crossing its territory. When Tether announced in January 2025 having issued more than 140 billion dollars in stablecoins in circulation, with a significant portion in Europe, the question isn't only about financial stability. It's also about strategic dependency.

European banks launching euro stablecoins aren't doing it out of economic patriotism. They're doing it because they understand that a 2 trillion dollar market in 2028 is being built now, and not being there means accepting to become secondary infrastructure in your own monetary ecosystem.

What will play out by 2028 in the stablecoin market

The most likely scenario isn't a clean victory of the euro or dollar in the stablecoin market. It's progressive segmentation. Dollar stablecoins will dominate intercontinental flows and emerging markets, where the dollar remains the reference currency. Euro stablecoins will develop on intra-European corridors and with eurozone trading partners.

This segmentation won't be natural. It will be the product of regulatory decisions. Article 22 of MiCA, with its safeguard clause, gives European authorities the power to limit the expansion of non-European stablecoins deemed systemic. If Circle or Tether see their growth capped at a certain threshold in Europe, European issuers will have a protected space to develop.

But this protection has a cost. It requires that European stablecoins achieve critical mass quickly in terms of users and liquidity. Otherwise, economic actors will continue to favor dollar stablecoins, which are more liquid, more accepted, more universal. Europe can regulate its market. It can't force its companies to use less efficient stablecoins.

This is where the urgency of the twelve European banks takes on full meaning. They're not aiming for 2028. They're aiming for 2026, the date when the first EMT licenses will have been issued and when the first significant volumes can circulate. If by that date, no euro stablecoin has reached 10 billion euros in outstanding volume, the window of opportunity will close. Payment habits will have consolidated around the dollar, and it will take ten years to reverse them.

The MiCA compliance watchpoint

You're a treasurer, CFO, or simply a crypto-asset holder in Europe. MiCA will modify your operating environment, whether you like it or not. Issuers of stablecoins non-compliant with the regulation must cease their European activities by June 2025, unless they obtain an EMT or ART license. Concretely, some stablecoins currently available on European exchange platforms could be delisted.

If you use stablecoins for treasury operations or international payments, verify right now the regulatory status of the issuer. The EBA publishes on its website the list of authorized entities. If your stablecoin isn't there, anticipate migration to a compliant asset. The cost of forced conversion during volatile periods can reach several percentage points.

For institutional investors: the arrival of bank-issued euro stablecoins will create new yield opportunities, notably through decentralized finance protocols that will integrate these regulated assets. But liquidity will remain fragmented for at least two years. The spreads between euro and dollar stablecoins could generate significant arbitrage opportunities for those who master on-chain currency mechanics.

Finally, for businesses considering accepting stablecoin payments: MiCA imposes enhanced traceability obligations. Article 68 requires that crypto-asset service providers (CASP) identify the origin and destination of funds. If you integrate stablecoins into your payment system, make sure your PSP has proper MiCA authorization. Penalties for non-compliance can reach 5 million euros or 10% of annual turnover, according to Article 101 of the regulation.

Europe isn't playing the same game as the United States on stablecoins. It's not betting on unbridled innovation, but on legal certainty and user protection. This choice may seem conservative. It's above all strategic. In a market targeting 2 trillion dollars by 2028, whoever sets the regulatory standards also sets tomorrow's rails. The question is no longer whether stablecoins will become major payment infrastructure. It's in which currency they'll circulate, and who will control that infrastructure.