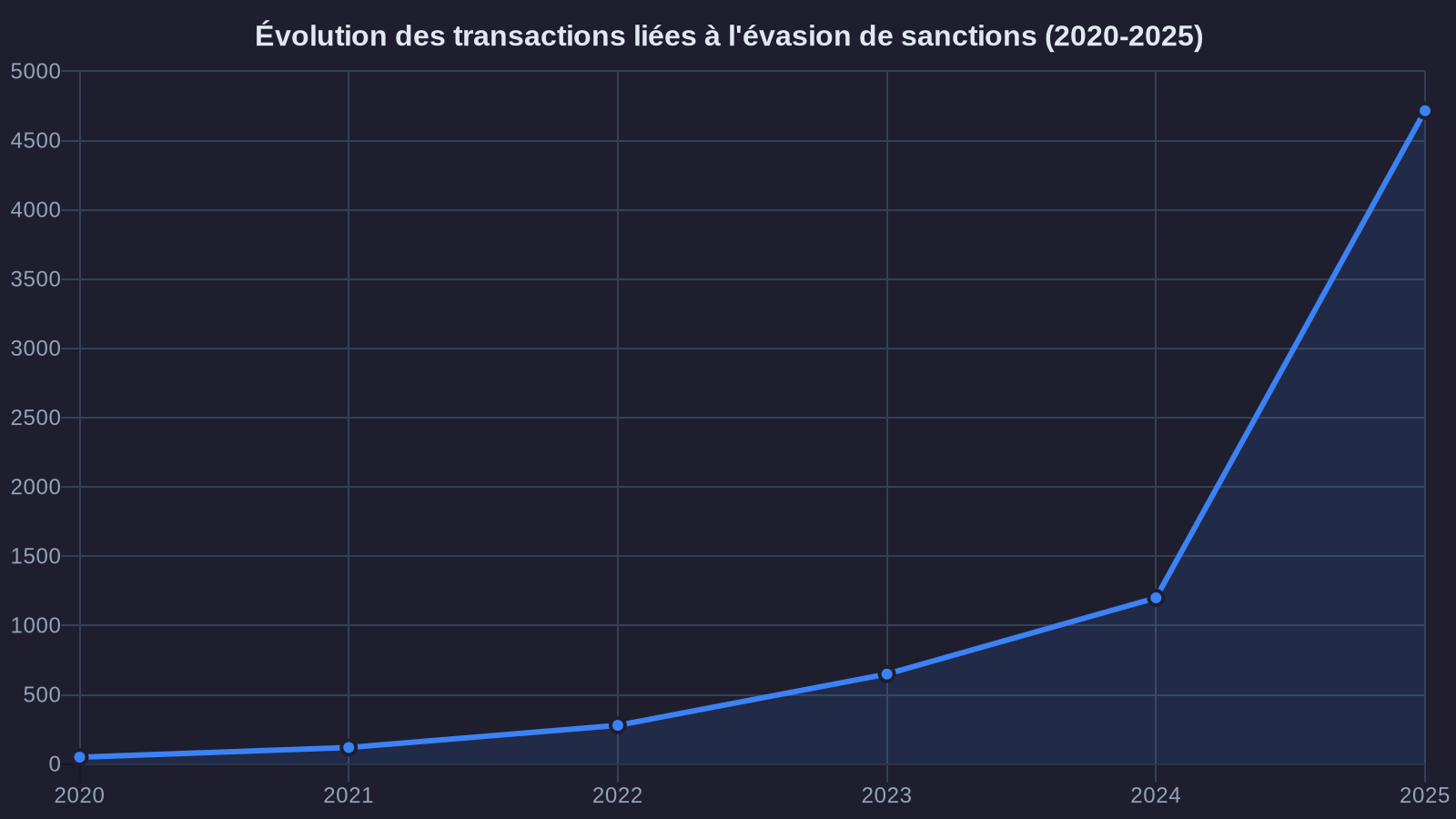

The Financial Action Task Force (FATF) has just released its 2025 report on money laundering and terrorist financing risks in the crypto sector. One figure immediately stands out: +694% increase in transactions related to international sanctions evasion. Behind this dramatic surge lies one particular financial instrument: stablecoins, cryptocurrencies pegged to the dollar or euro.

While stablecoins have conquered the market thanks to their stability and practical utility, they are now at the heart of a critical regulatory debate on FATF compliance and sanctions evasion. The FATF points not to their legitimate use on regulated platforms, but to their circulation on secondary markets and decentralized protocols, where traditional surveillance mechanisms struggle to apply.

For stablecoin holders and industry professionals, this report marks a turning point. Regulatory pressure will intensify, and the European Union, with its MiCA regulation progressively entering into force since 2024, is positioning itself at the forefront of this regulatory offensive.

The 2025 FATF Report: What's Changed in Stablecoin Compliance

The FATF regularly updates its anti-money laundering recommendations to adapt the framework to new financial realities. Its 2025 report dedicates an entire chapter to stablecoins and identifies three major shifts that explain this concerning rise in diversions.

First observation: the growing sophistication of evasion schemes. While bad actors once relied on Bitcoin mixers or complex transaction chains, they now favor stablecoins for their instant liquidity and near-universal acceptance. A USDT or USDC converts instantly into fiat currency in dozens of jurisdictions, including those less vigilant about fund traceability.

Second finding: the explosion of peer-to-peer exchanges and non-custodial DeFi protocols. The FATF notes that 73% of suspicious transactions identified in 2024 passed through decentralized platforms or over-the-counter exchanges, thus escaping KYC (Know Your Customer) obligations imposed on digital asset service providers (DASP). These parallel circuits allow sanctioned entities to convert stablecoins into local currencies without passing through the traditional banking system.

Third structural element: the geographic fragmentation of stablecoin issuance and circulation. While Tether (USDT) and Circle (USDC) are domiciled in high-regulation jurisdictions, their tokens circulate freely on blockchains accessible from anywhere in the world. This disconnect between issuer, holder, and end beneficiary significantly complicates the work of financial intelligence units.

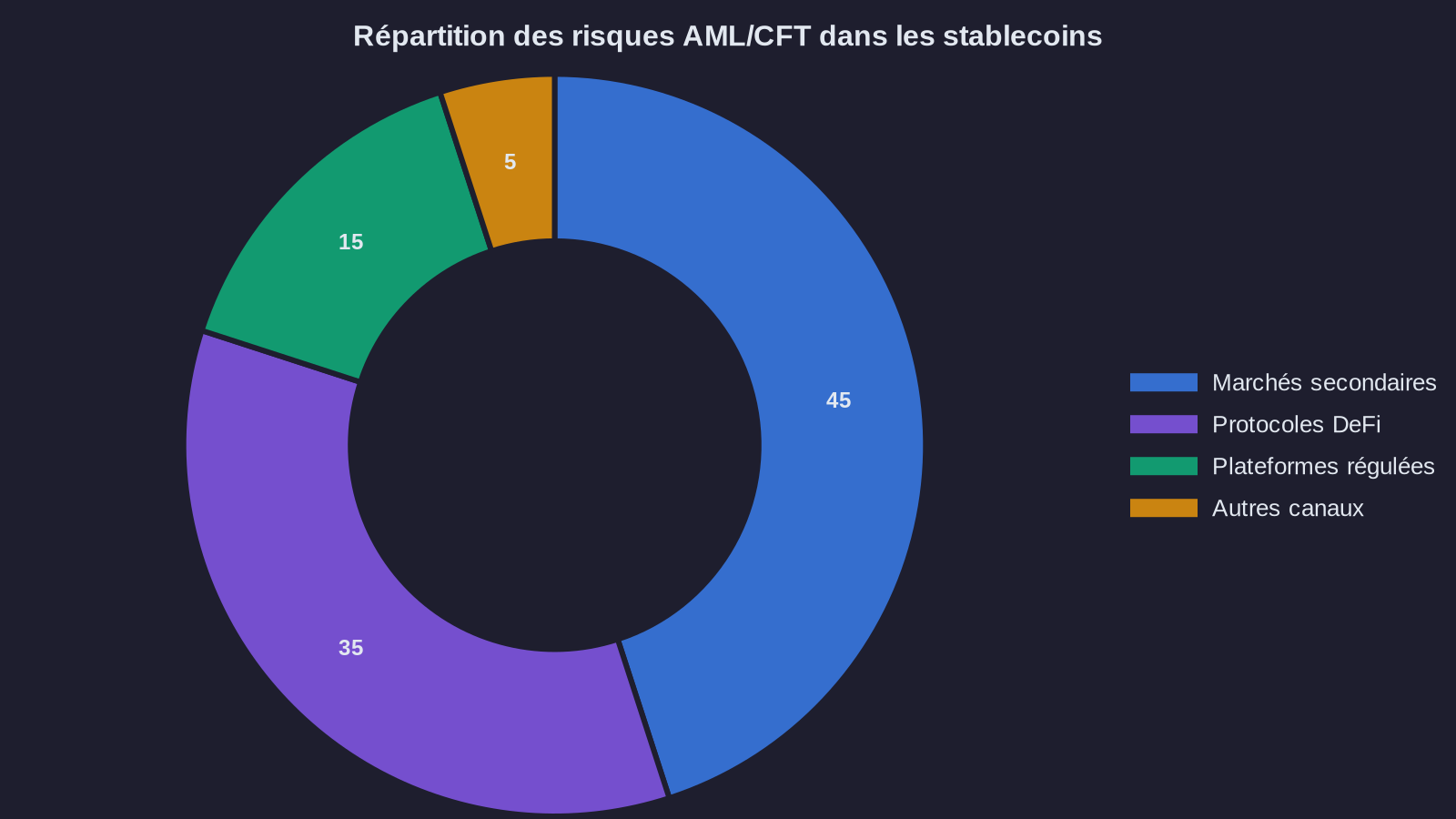

Secondary Markets: The Blind Spot in Stablecoin Surveillance

The FATF report points to a problem regulators know but still struggle to solve: secondary market surveillance. On a regulated platform like Coinbase or Kraken, each transaction undergoes identity verification, risk analysis, and where applicable, a suspicious activity report to TRACFIN in France or FinCEN in the United States.

But once a user has withdrawn their stablecoins to a personal wallet, traceability becomes far more opaque. Admittedly, all transactions remain recorded on the blockchain, but the identity of an address holder is not public. A USDT can change hands dozens of times via decentralized exchanges (DEX), lending protocols, or simple direct transfers, without any regulated entity knowing the identity of the parties involved.

The FATF emphasizes that this gray zone of the secondary market is massively exploited by three categories of actors:

- Sanctioned entities (states, companies, individuals subject to international embargoes) that use stablecoins to circumvent banking restrictions and access global markets.

- Professional money laundering networks that offer crypto-to-fiat conversion services through informal exchange networks, particularly in Southeast Asia, Latin America, and the Middle East.

- Fraudsters and cybercriminal groups that demand ransoms in stablecoins rather than Bitcoin, because conversion to liquid funds is faster and less traceable.

Faced with this situation, the FATF recommends extending compliance obligations to decentralized protocols themselves, a proposal that raises complex technical and legal questions. How can you enforce KYC on a smart contract autonomously deployed on Ethereum? Who is responsible for compliance of an open-source protocol without a centralized legal entity? These questions largely remain unanswered.

MiCA and the European Response: Toward Systematic Stablecoin Tracing

The European Union has gained regulatory ground with the MiCA regulation (Markets in Crypto-Assets), which entered into force progressively since June 2024. While MiCA primarily regulates service providers and token issuers, Article 62 imposes specific requirements on issuers of reference stablecoins (e-money tokens and asset-referenced tokens).

In practice, any stablecoin issuer exceeding certain capitalization or transaction volume thresholds must obtain authorization from the European Banking Authority (EBA) and comply with reserve, liquidity, and reporting obligations. Tether and Circle, the two sector giants, must either comply or restrict their distribution in Europe.

But MiCA goes further. Article 68 introduces an obligation to cooperate with financial supervision authorities to detect and report suspicious transactions. In other words, stablecoin issuers must implement monitoring systems capable of identifying fund movements to addresses linked to sanctioned entities or illicit activities.

This approach follows the funds transfer regulation (Regulation (EU) 2023/1113, known as the "Travel Rule"), which requires DASPs to collect and transmit identification information of senders and beneficiaries for any transaction exceeding 1,000 euros. The objective: recreate in the crypto world the equivalent of the SWIFT system, where every fund movement is documented and traceable.

The challenge remains immense. Stablecoins circulate on public blockchains, accessible without geographic restrictions. A user based in a third country can easily buy USDC on a DEX, transfer them to a self-hosted wallet, then exchange them for bitcoins or convert them into local currency through an informal network. MiCA can only control the entry point (regulated platforms) and the issuer, not secondary circulation.

What This Means for You: Enhanced Compliance Vigilance

If you hold stablecoins or your business accepts them as payment, expect intensified checks and justification requests. European financial intelligence units, including TRACFIN in France, are strengthening their blockchain analysis capabilities and collaborating increasingly closely with companies specializing in on-chain tracing (Chainalysis, Elliptic, CipherTrace).

Several concrete points of vigilance:

On regulated platforms, identity verifications will become stricter. Some DASPs now require proof of fund origins for any stablecoin deposit above a certain threshold. If you transfer USDT from a personal wallet to Kraken, you may be asked to prove those tokens come from a legitimate source (documented initial purchase, payment for services, etc.).

Withdrawals to self-hosted wallets are also under increased surveillance. Several European platforms now limit withdrawals to non-whitelisted addresses or impose verification delays for significant amounts. The objective: ensure funds don't transit to unregulated protocols or exchanges in high-risk jurisdictions.

Peer-to-peer transactions, particularly via platforms like LocalBitcoins or Telegram groups, are in the crosshairs. The FATF explicitly recommends that member states monitor these circuits and sanction intermediaries facilitating sanctions evasion. In France, conducting a crypto-to-fiat exchange activity without DASP registration is subject to criminal penalties (Article L. 574-1 of the French Monetary and Financial Code).

Finally, for businesses accepting stablecoin payments, customer due diligence obligations are increasing. You must be able to justify the origin of funds received, especially if amounts are significant or transactions come from sensitive jurisdictions. Article L. 561-10 of the French Monetary and Financial Code requires professionals to implement risk-appropriate vigilance procedures. Concretely, this means: enhanced identity verification, documentation of business relationships, and suspicious activity reporting if anything unusual is detected.

The Future of Stablecoins: Compliance or Marginalization?

The FATF report and the European regulatory response sketch two possible futures for stablecoins. The first scenario: progressive integration into the regulated financial system, with compliant issuers, licensed distribution platforms, and systematic traceability mechanisms. Stablecoins would then become a payment tool as monitored as bank transfers, but infinitely faster and cheaper.

The second scenario: market fragmentation, with "clean" stablecoins accepted by institutions on one side, and tokens circulating in a parallel economy on decentralized protocols and informal networks on the other. This dichotomy already exists: some exchanges now refuse to list tokens that have transited through mixers or blacklisted addresses.

For regulators, the challenge is striking the right balance. Too many constraints, and legitimate players will leave Europe for more accommodating jurisdictions. Too few, and stablecoins will continue to be a preferred vector for sanctions evasion and money laundering.

The FATF is betting on strengthened international coordination. Its new recommendations call for harmonization of compliance standards across major jurisdictions (United States, European Union, United Kingdom, Japan, Singapore). The objective: avoid regulatory arbitrage and progressively close gray zones.

The vigilance point: If you use stablecoins, prepare for increased transparency. Opaque transactions or complex structures will systematically attract authority attention. The best protection remains rigorous documentation of your operations and using regulated platforms for any crypto-to-fiat conversion. Consult your accountant or legal counsel to adapt your practices to new requirements, especially if you manage significant volumes or operate internationally.

The FATF report marks a decisive step in regulatory normalization of crypto-assets. Stablecoins are no longer a technical niche: they now represent over 200 billion dollars in capitalization and are used daily by millions of users. Their integration into the global anti-money laundering framework is no longer a matter of principle, but operational urgency. The coming months will tell whether issuers, platforms, and regulators can build an ecosystem that is both efficient and compliant. One thing is certain: the era of crypto Wild West is coming to an end.