March 2025. An announcement that slipped under the radar of mainstream media marks a turning point for anyone holding crypto assets as part of their wealth strategy. Fannie Mae, the quasi-governmental institution guaranteeing nearly 30% of U.S. mortgage loans, is partnering with Coinbase to launch a pilot program for Bitcoin-backed mortgages in the United States.

Concretely, this means a Bitcoin owner in the U.S. can now use their digital assets as collateral to finance the purchase of a primary residence without having to sell their positions. For European investors watching this market closely, the question arises: is this a credible wealth-building opportunity or a risky structure that could undermine their allocation strategy?

Let's examine this development with the necessary perspective, backed by data.

The mechanism: how a Bitcoin collateral mortgage actually works

The principle isn't entirely new. Since 2018-2019, players like BlockFi or Nexo were already offering crypto-backed loans. What changes with Fannie Mae's entry is the normalization and standardization of these products within the traditional American financial system.

Let's take a concrete example. You hold 10 BTC, currently valued at approximately €850,000 (assuming Bitcoin at €85,000). You want to purchase a property worth €400,000 in the United States. Rather than selling 5 BTC—which would trigger immediate taxation on capital gains, potentially 30% flat tax in France—you use your 10 BTC as collateral.

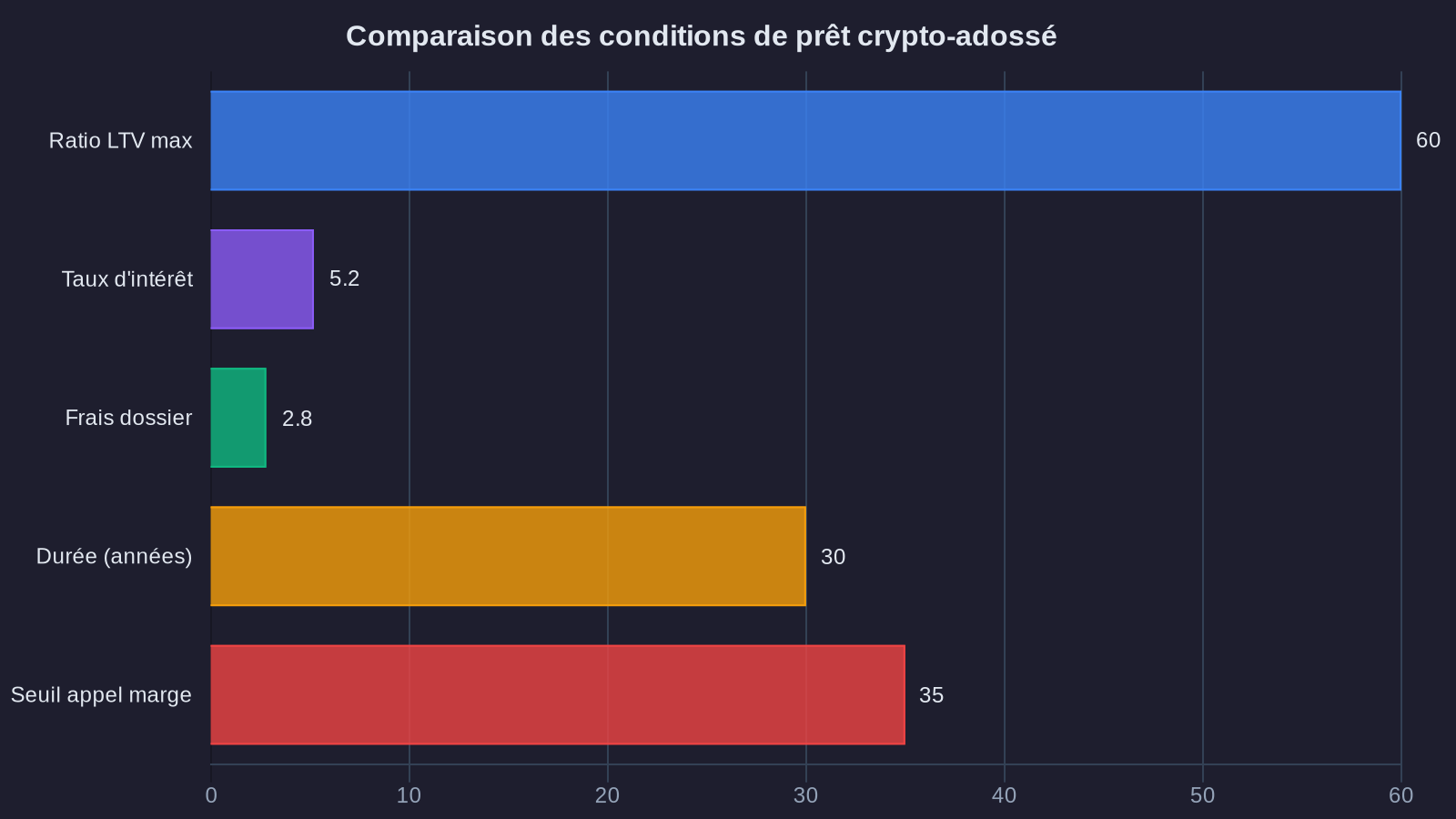

The lender then grants you a standard mortgage of €400,000, with a loan-to-value (LTV) ratio generally capped between 30% and 50%. This means that to borrow €400,000, you must provide collateral of at least €800,000 to €1,300,000 in Bitcoin. Your BTC remains locked for the duration of the loan, but you retain ownership and benefit from any future appreciation.

The interest rate currently ranges between 5.8% and 7.2% depending on your profile, or roughly 1 to 2 percentage points above a standard U.S. mortgage, which hovers around 6% in early 2025. This risk premium compensates for the intrinsic volatility of the collateral. To learn more about crypto financing mechanisms in the United States, check out our detailed analysis: United States: how your Bitcoin can finance your home.

The wealth equation: when does this Bitcoin real estate structure make financial sense

For such a product to present genuine wealth-building interest, several conditions must be met. The first is obvious: you must anticipate that your Bitcoin's future performance will exceed the cost of credit, net of taxes.

Let's compare two scenarios over a 10-year horizon, with a French investor holding 10 BTC valued at €850,000, wanting to purchase a property worth €400,000.

Scenario A: selling BTC and buying outright

- Sale of 5 BTC to raise €425,000

- Assumed average cost basis: €20,000 per BTC (€100,000 for 5 BTC)

- Taxable capital gain: €325,000

- 30% flat tax: €97,500

- Net available: €327,500

- Amount to finance: €72,500 in cash or standard credit

Scenario B: keeping BTC and taking a secured loan

- 10 BTC locked as collateral (valuation €850,000, 47% LTV)

- Loan of €400,000 at 6.5% over 20 years

- Monthly payment: approximately €2,985

- Total interest cost over 20 years: €316,400

- Maintained exposure to 10 BTC throughout the loan period

The wealth arbitrage becomes favorable to scenario B if, and only if, Bitcoin's annualized performance exceeds approximately 6.5% per year over the period. Historically, BTC has delivered annualized performance of roughly 45% since 2013. Even taking a much more conservative assumption—say 12% per year over the next 10 years—your 10 conserved BTC would be worth approximately €2,640,000 versus €1,325,000 if you had kept only 5 BTC.

The difference of €1,315,000 far exceeds the loan cost of €316,400, even incorporating deferred taxation. However, this calculation rests on a strong assumption: continuous Bitcoin appreciation.

The risks: what banks don't always tell you clearly

The first risk, and the most obvious, is that of a margin call. If your Bitcoin collateral's value drops below a certain threshold—generally when LTV exceeds 70% to 80%—the lender will ask you to either provide additional liquidity or sell part of your BTC to restore the collateral ratio.

Take our earlier example. You borrowed €400,000 against 10 BTC valued at €850,000 (initial LTV of 47%). If Bitcoin falls to €50,000, your 10 BTC are now worth only €500,000. Your LTV jumps to 80%. The bank notifies you that it requires a return to 65% LTV, meaning you must either provide €75,000 in cash or sell 1.5 BTC.

This mechanism caused massive liquidations in 2022 during the Luna and Celsius collapse. Thousands of borrowers saw their positions liquidated by force, permanently losing their digital assets at the worst point in the cycle.

The second risk concerns the lock-up duration. A standard mortgage spans 15 to 25 years. Blocking a significant portion of your crypto portfolio over such a period deprives you of all flexibility. If an exceptional investment opportunity arises—or if you face an unexpected situation—you cannot mobilize these assets without repaying the loan early, which typically involves penalties.

Finally, a rarely mentioned point: counterparty risk. When you deposit your BTC as collateral, they leave your direct control. You depend on the solvency and governance of the lending institution. FTX's collapse in November 2022 reminded everyone that even apparently solid platforms can implode in days. With Fannie Mae and Coinbase, counterparty risk is objectively lower than with an unregulated actor, but it's never zero. To better understand protection mechanisms, see our article: DeFi circuit breakers: how protocols protect your funds in real-time.

Wealth positioning: for whom can this product make sense

Based on the analysis above, this type of structure isn't suitable for all wealth profiles. It primarily addresses investors who combine three characteristics.

First, a strong and long-term conviction about Bitcoin appreciation. If you view BTC as a speculative asset you wish to exit medium-term, there's no point locking it up as collateral for a 20-year loan. This product is designed for those who see Bitcoin as a store of value for wealth, much like gold or real estate.

Second, the ability to absorb volatility and potential margin calls. Concretely, this means having a cash reserve representing at least 20% to 30% of the borrowed amount. In our €400,000 example, it would be prudent to maintain €80,000 to €120,000 in quickly accessible liquidity to handle a potential margin call without being forced to sell at the worst moment.

Third, sufficient wealth diversification. Locking up your entire crypto portfolio as collateral for a mortgage amounts to concentrating risk twice: on Bitcoin on one hand, real estate on the other. A reasonable allocation would require these two positions combined not exceed 40% to 50% of your total wealth. Our guide on wealth diversification deepens these allocation principles.

In practice, this product finds its optimal utility in a specific situation: a long-term Bitcoin investor wishing to acquire a primary residence in the United States without triggering a taxable event, and who has otherwise accumulated diversified savings allowing them to manage uncertainties with ease.

What this means for your wealth

Fannie Mae's entry into this market constitutes a signal of institutional normalization. Five years ago, using Bitcoin as loan collateral was an exotic arrangement, reserved for early adopters willing to take significant counterparty risks. Today, the same mechanism enjoys near-governmental American endorsement.

Yet this institutional legitimation changes nothing about the fundamental risk profile. A loan backed by a volatile asset remains a loan backed by a volatile asset. Bitcoin's annualized volatility over the past three years hovers around 65%, versus 15% for the S&P 500. No institutional blessing modifies this reality.

If you're considering this type of structure, the central question remains: what portion of your wealth are you willing to expose simultaneously to crypto risk and real estate risk, while bearing a carrying cost of 6% to 7% annually? For most French investors, the answer should fall somewhere between 0% and 15% of total wealth, no more.

This product is neither revolutionary nor a trap. It's another tool in the wealth-building toolkit, one that will find its place in certain well-defined situations. The key is identifying them rigorously, backed by data.

Your wealth deserves better than a savings account. I'll show you the way, backed by the numbers.