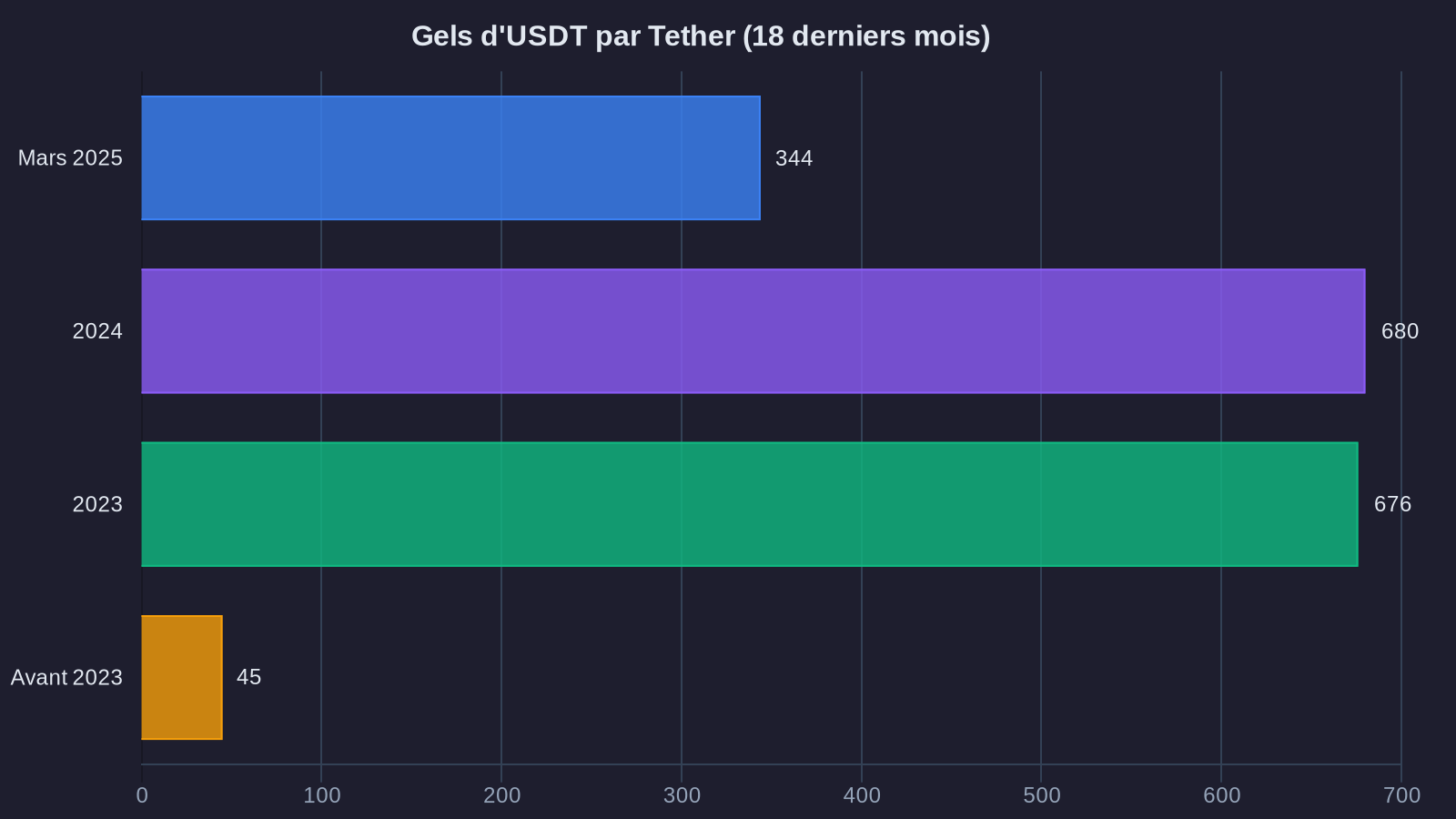

On March 13, 2025, Tether froze $344 million in USDT associated with Iranian addresses in response to heightened US sanctions. The operation took less than 48 hours. No recourse available for affected holders. No appeal process.

This USDT freeze event raises a direct question for institutional investors and family offices: if the asset you consider "stable" can be unilaterally frozen by its issuer, what is its true reserve value?

Analysis of the implications for your crypto allocations and asset protection strategies in the face of stablecoin censorship.

The context: when geopolitics catch up with stablecoins

Iran sanctions are nothing new. But their application to cryptocurrencies has intensified since 2023, with mounting pressure from the US Treasury Department on stablecoin issuers.

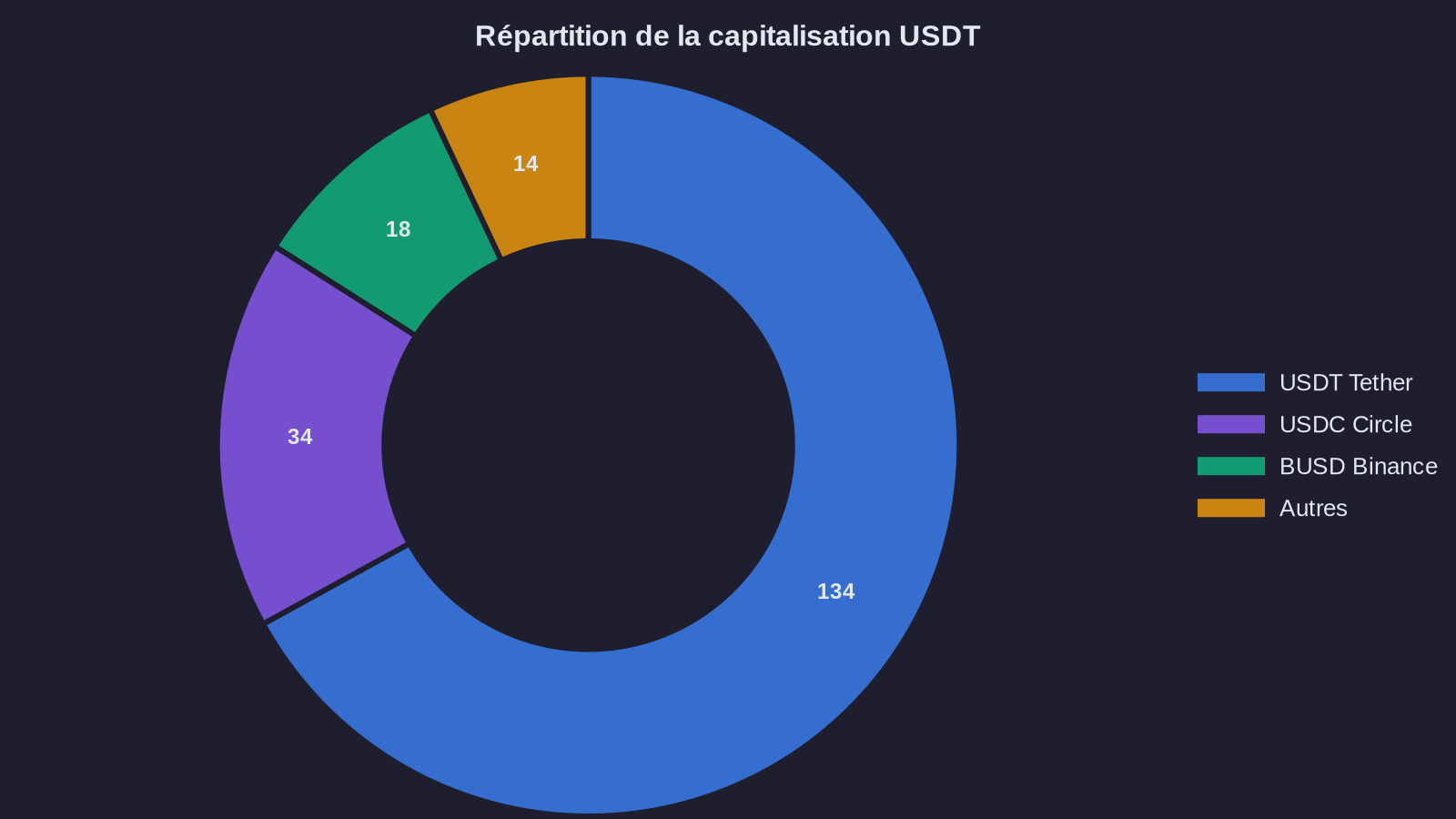

Tether, issuer of the largest stablecoin by market cap ($134 billion as of March 18, 2025), has actively collaborated with US authorities since late 2023. The company has frozen over $1.7 billion in USDT on sanctioned addresses over the past 18 months, according to its own transparency reports.

The March 2025 freeze represents the largest single operation to date. The $344 million primarily involved currency exchange circuits and peer-to-peer trading platforms used in Iran to circumvent international banking restrictions.

From Tether's perspective, this cooperation is strategic: it facilitates dialogue with US and European regulators as the company seeks licenses across multiple jurisdictions. From the perspective of affected users, it's outright confiscation, without process or compensation.

What this freeze reveals about the true nature of centralized stablecoins

USDT is not a decentralized cryptocurrency. It's a debt instrument issued by a private company (Tether Limited), theoretically backed by reserves in dollars and US Treasury bonds. Each USDT token represents a promise of redemption at par with the dollar.

This structure entails three systemic risks that this freeze brings to light:

First risk: censorship at the protocol level. Tether has a technical function in the USDT smart contract that allows it to "blacklist" any address. Once blacklisted, the address can neither send nor receive USDT. The tokens remain visible in the wallet but become unusable. There is no built-in dispute mechanism in the protocol.

This technical capability is not a bug—it's an intentional feature. It allows Tether to respond to orders from authorities. But it also sets a precedent: if the company can freeze $344 million in 48 hours under geopolitical pressure, it can theoretically freeze any amount for any reason deemed sufficient by the competent authorities. Circle has moreover demonstrated similar capacity with USDC, confirming that stablecoin censorship is now a structural reality of the market.

Second risk: concentration of censorship power. The freeze decision rests with a single entity: Tether Limited. There is no decentralized governance, no community vote, no independent appeals mechanism. The company acts as an obligatory intermediary between token holders and access to their value.

This centralization poses a structural problem for institutional allocations. If a stablecoin can be unilaterally censored, it no longer fulfills its role as a liquid and permanently accessible store of value. It becomes a conditional asset, whose availability depends on the whim of its issuer and the authorities that oversee it.

Third risk: progressive expansion of freeze criteria. Today, it's sanctions against Iran. Tomorrow, it could be other criteria: anti-money laundering, taxation, capital controls, sectoral regulation. Each new regulatory pressure potentially expands the scope of "at-risk" addresses.

Centralized stablecoin issuers have no choice but to cooperate: refusing would jeopardize their licenses, banking relationships, and ability to maintain the reserves that guarantee parity with the dollar. But this cooperation gradually transforms stablecoins into an extension of the traditional banking system, with the same constraints and vulnerabilities.

Concrete implications for your crypto allocations

If you hold a significant portion of your crypto liquidity in centralized stablecoins (USDT, USDC, BUSD), this freeze changes the risk equation.

Your tokens are not "freezable" unless you are directly targeted by sanctions or an investigation. But the risk is not binary. It exists along a continuum ranging from full liquidity to complete unavailability, with several intermediate stages:

For regulated institutions: the risk of reputation and compliance exposure increases. Holding large volumes of USDT raises legitimate questions from auditors and regulators: how do you ensure your counterparties are not themselves exposed to sanctioned addresses? How do you trace the origin of your stablecoins? What KYC processes do you apply to your liquidity providers?

These questions are not theoretical. Several European funds have already reduced their USDT exposure in 2024-2025, precisely to avoid complications related to regulatory reporting under MiCA (the European crypto-assets regulation that entered into force in 2024).

For family offices and sophisticated private investors: the risk is one of conditional liquidity. If a significant part of your crypto allocation is in USDT and Tether faces increased regulatory pressure (for example, an investigation into money laundering involving major counterparties), access to that liquidity could degrade rapidly. Not necessarily through a direct freeze, but through a scarcity of counterparties accepting USDT, higher conversion fees, or a discount on OTC markets.

This scenario is not an extreme hypothesis. It already happened with USDC in March 2023, when Circle (its issuer) revealed a $3.3 billion exposure to bankrupt Silicon Valley Bank. USDC briefly lost parity with the dollar, falling to $0.88 before stabilizing. For 72 hours, holding USDC meant accepting a 12% discount and degraded liquidity.

Alternatives and asset protection strategies to mitigate this risk

The solution is not to abandon all stablecoins. They remain an indispensable tool for managing liquidity in a crypto portfolio. But the composition of this liquidity pool must evolve to account for censorship risk.

Diversification across centralized stablecoins: USDT and USDC represent 92% of total stablecoin market cap as of March 18, 2025. But they don't respond to the same pressures. USDC (issued by Circle, US-based) is more exposed to American and European regulations but benefits from enhanced transparency and regular audits. USDT (issued by Tether, British Virgin Islands-based) operates in a regulatory gray zone but enjoys superior liquidity on Asian markets and unregulated exchanges.

Spreading your exposure across multiple issuers reduces concentration risk. If one faces major regulatory pressure, you retain liquidity via the others.

Integration of decentralized stablecoins: DAI (issued by MakerDAO) and FRAX represent partially decentralized alternatives. DAI is collateralized by other crypto-assets (ETH, centralized stablecoins, tokenized bonds) and governed by a DAO. It cannot be frozen by a central entity. But its liquidity remains inferior to USDT and carries volatility risk if underlying collateral deteriorates.

FRAX uses a hybrid model, partially collateralized and partially algorithmic. It offers a compromise between decentralization and stability, but remains less liquid than dominant stablecoins.

These options don't replace USDT or USDC in an institutional portfolio. But they can constitute 10-20% of your crypto liquidity pool as insurance against widespread censorship risk on centralized stablecoins. Growing institutional adoption of stablecoins makes this diversification all the more critical.

Recourse to tokenized bonds and on-chain money market funds: A growing share of institutional liquidity on blockchain is moving toward on-chain yield products backed by traditional assets: tokenized US Treasury bonds (via Ondo Finance, Franklin Templeton, BlackRock), on-chain money market funds (via Backed Finance, Hashnote).

These instruments offer yields (currently between 4.5% and 5.2% on products backed by US T-Bills) while maintaining near-instant liquidity. They carry a different regulatory risk than stablecoins: they are traditional financial securities, subject to securities regulations, with regulated issuers and institutional custodians.

They are not suitable for all uses (they are less liquid than USDT for high-frequency trading or exchange arbitrage), but they constitute a credible alternative for the "treasury reserve" portion of an institutional crypto portfolio.

What ForYield thinks

We have integrated centralized stablecoin censorship risk into our management strategies since 2024. Our allocations systematically include diversification across multiple stablecoin issuers, with dynamic weighting adjusted based on regulatory signals and liquidity observed on OTC markets.

For portfolios above €5 million, we recommend allocating 15-30% of the liquidity pool to decentralized alternatives or regulated on-chain yield products. This allocation aims not for performance but for resilience: it guarantees access to liquidity even if the availability of dominant stablecoins deteriorates sharply.

The $344 million freeze by Tether is not an accident. It's a signal: centralized stablecoins are gradually becoming extensions of the traditional financial system, with its constraints and control points. Adjusting your allocation to this reality is not a matter of ideology—it's a matter of risk management.

If you wish to analyze your current stablecoin exposure and identify relevant adjustments for your allocation, our teams are available for a portfolio audit.

```