Goldman Sachs just crossed a symbolic milestone by massively integrating Bitcoin ETFs into its institutional investment portfolios. This validation from the financial establishment marks a turning point, but it raises a crucial question for French investors: should you prioritize these regulated investment vehicles or maintain direct ownership of crypto-assets?

The answer doesn't come down to crypto ideology or pure regulatory compliance. It depends on a careful analysis of your tax situation, your return objectives, and your ability to navigate a French legal framework that is particularly complex when it comes to crypto-asset taxation.

The mirage of Bitcoin ETF simplicity

Bitcoin ETFs like those offered by BlackRock or Fidelity appeal through their apparent simplicity. You buy them like a stock, they appear on a standard securities account, and the bank handles administrative compliance. For a CFO or family office accustomed to traditional financial products, that's reassuring.

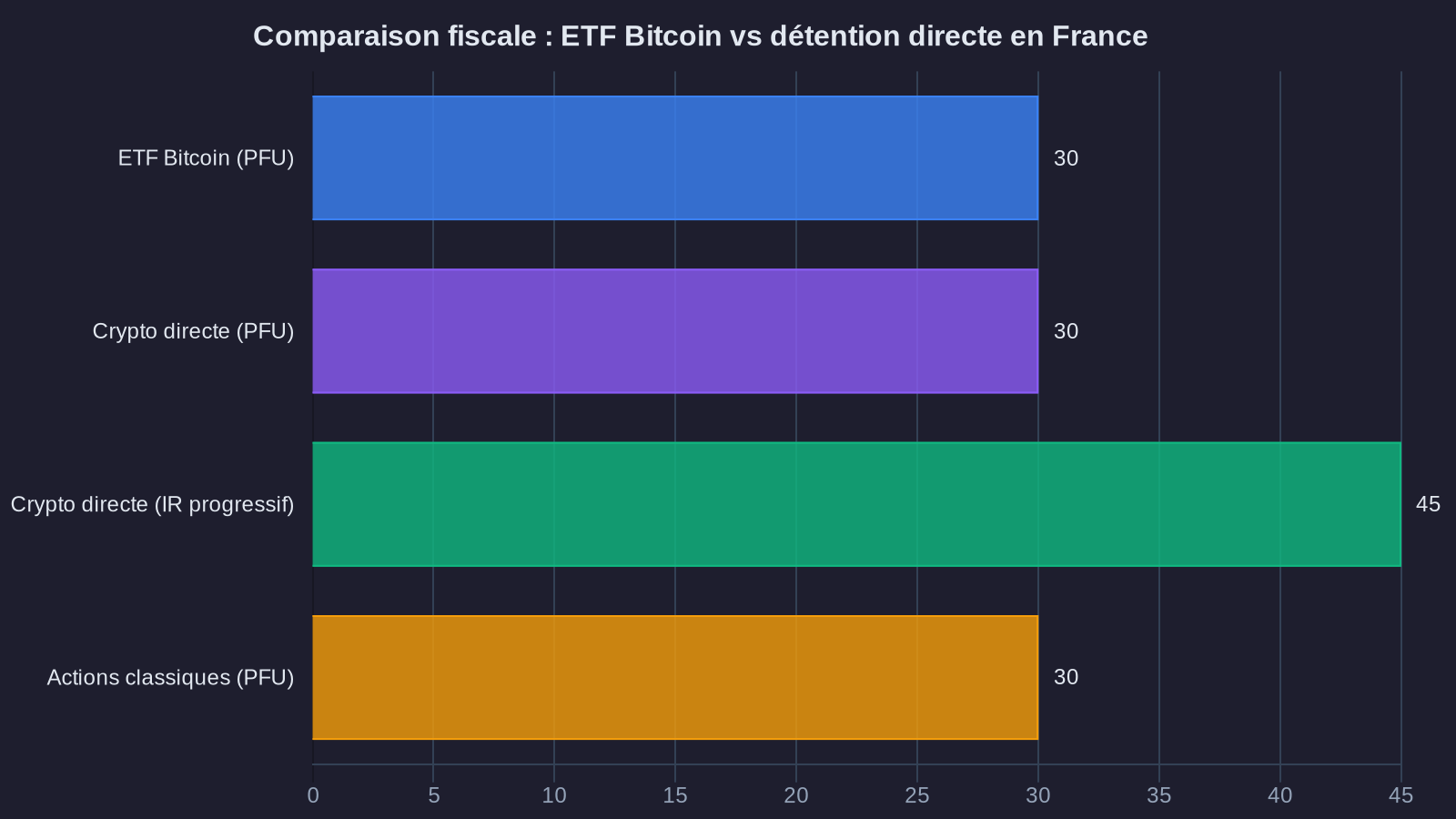

Except that this simplicity masks a less obvious tax reality. In France, Bitcoin ETFs listed in the United States or Europe are treated under the tax regime for standard securities. Specifically, this means taxation under the flat-rate levy (PFU) of 30% on realized gains. This rate combines 12.8% income tax and 17.2% social contributions.

First point to watch: unlike European stocks, Bitcoin ETFs don't benefit from a deduction for holding period. Whether you hold your shares for two months or ten years, the rate stays the same. There's no incentive for long-term holding, contrary to what some financial advisors unfamiliar with crypto-assets might suggest.

Second pitfall often overlooked: the question of management fees. A Bitcoin ETF typically charges annual fees between 0.20% and 0.95%. On exposure of several million euros, these fees can represent tens of thousands of euros per year. These recurring costs mechanically erode net returns, with no meaningful opportunity to optimize them from a tax perspective.

Direct ownership: apparent complexity, real flexibility

Holding Bitcoin directly means managing custody, security, and tax reporting of your assets yourself. It's undeniably more demanding operationally. But this complexity opens up tax optimization levers that ETFs simply don't allow.

The French tax regime for directly held crypto-assets is based on article 150 VH bis of the General Tax Code. Gains are taxed under the 30% PFU, just like ETFs. But be careful—this only applies if you stay within the framework of private wealth management. Once the activity becomes habitual or commercial, the regime switches to self-employment income (BNC) or business profits (BIC), with taxation that can reach 45% plus social contributions.

The real strategic difference lies in the flexibility of managing tax events. With direct ownership, you can precisely time when you realize gains. For example, you can spread sales over multiple years to stay below the €305 annual net gain threshold that qualifies for tax exemption. This threshold is ridiculously low for significant wealth, but it illustrates a legal optimization possibility that doesn't exist with ETFs.

Another dimension often misunderstood: loss carryforward and offsetting. If you hold multiple crypto-assets directly, you can offset losses from one asset against gains from another in the same fiscal year. This tax smoothing mechanism is much harder to implement with ETFs, where each vehicle is treated in isolation. For investors looking to optimize their taxes while limiting risk, solutions like Lombard credit loans allow you to use your crypto without triggering immediate tax events.

Sophisticated investors also use tax loss harvesting strategies adapted to the French framework. Specifically, you intentionally realize a loss late in the fiscal year to offset a gain realized elsewhere, then quickly reinvest. This technique, perfectly legal if it respects the substance-over-form principle, is technically possible with ETFs but far more flexible with direct ownership where you control the timing of each transaction precisely.

Compliance and reporting: where the real pain points are

Tax compliance for crypto-assets in France is often an uphill battle, even for seasoned professionals. Tax authorities require annual reporting of all crypto-asset accounts held abroad via form 3916-bis. This obligation applies to direct ownership, but not to ETFs which are simply financial securities.

In theory, that's a point in favor of ETFs. In practice, this reporting obligation is far from insurmountable if you organize properly. Many French institutional investors and family offices have implemented robust compliance processes that integrate this reporting into their annual tax routine. The real risk lies in improvisation and lack of planning.

What truly creates problems is transaction traceability for calculating gains. With ETFs, your broker or private bank provides you with a single tax statement (IFU) summarizing everything. It's automatic, standardized, and easily usable by your accountant or tax advisor.

With direct ownership, you must reconstruct your complete transaction history, applying the weighted average cost method mandated by French tax authorities. If you've made multiple trades across different exchanges, this reconstruction can become an administrative nightmare. Specialized tools like Waltio or Koinly can automate part of the work, but they require careful setup and don't cover all scenarios, particularly complex DeFi operations or peer-to-peer transactions.

The stakes of transaction traceability go beyond mere administrative convenience. In case of a tax audit, lack of rigorous documentation can result in arbitrary assessment based on unfavorable assumptions. Tax authorities can reclassify private wealth management as habitual activity, with all the tax and social consequences that entails.

Building a hybrid strategy suited to your profile

The real question isn't choosing between ETFs and direct ownership based on ideological considerations, but building an allocation that's coherent with your operational constraints and tax objectives.

For a French institutional investor subject to strict governance requirements, Bitcoin ETFs present clear advantages in terms of regulatory compliance and reporting. An insurance company, pension fund, or foundation under AMF supervision will find in ETFs a familiar investment framework, with regulated counterparties and immediate liquidity on established markets.

Conversely, for a family office with the necessary human and technical resources, a hybrid approach may prove more performant. Allocating part of the portfolio to ETFs to ensure liquid, compliant exposure, while holding a significant portion directly to benefit from tax optimization levers and strategic flexibility.

This hybrid strategy also allows you to diversify counterparty risk. Bitcoin ETFs, despite all their regulatory safeguards, remain exposed to the risk of issuer or custodian insolvency. Direct self-custody ownership, if properly secured, eliminates counterparty risk in favor of operational risk that you need to know how to manage.

Another parameter to integrate into your thinking: holding period and your wealth transfer strategy. If you're planning to transfer your crypto-assets in an estate context, direct ownership offers legal structuring possibilities (gifting, usufruct arrangements, trusts under certain conditions) that don't exist with standard ETFs. For investors approaching retirement, the question of changing tax residency can radically change the tax equation for your crypto-assets. Directly held crypto-assets can also be integrated into specific wealth optimization structures, subject to appropriate legal and tax guidance.

Finally, geography matters. If you're a tax resident of France but considering international mobility in the medium term, direct ownership offers portability that ETFs don't always have. Transferring Bitcoin from one wallet to another is technically simple and nearly instantaneous. Transferring ETFs from a French securities account to an account abroad can trigger complex and costly tax events.

Goldman Sachs' positioning on Bitcoin ETFs testifies to the irreversible institutionalization of Bitcoin as an asset class. But this validation from traditional players doesn't mean their approach is optimal for all French investor profiles. Between apparent compliance and real optimization, the difference is measured in dozens of basis points of net returns and the ability to navigate calmly through a regulatory environment that continues to evolve. What matters, ultimately, is building an exposure strategy coherent with your tolerance for operational risk and your ambition for after-tax performance.