HSBC and Standard Chartered have just received authorization to issue stablecoins in Hong Kong, making them the first traditional financial institutions to cross this threshold within a strict regulatory framework. This decision marks a turning point for the financial sector, but especially for companies seeking credible alternatives for managing their treasury in digital currencies.

For a chief financial officer, this news raises a concrete question: should these bank-issued stablecoins be viewed differently from current options like USDC or USDT? The answer depends on several factors we'll examine, keeping in mind that any exposure to crypto-assets carries the risk of capital loss and requires careful consideration of the company's overall treasury strategy.

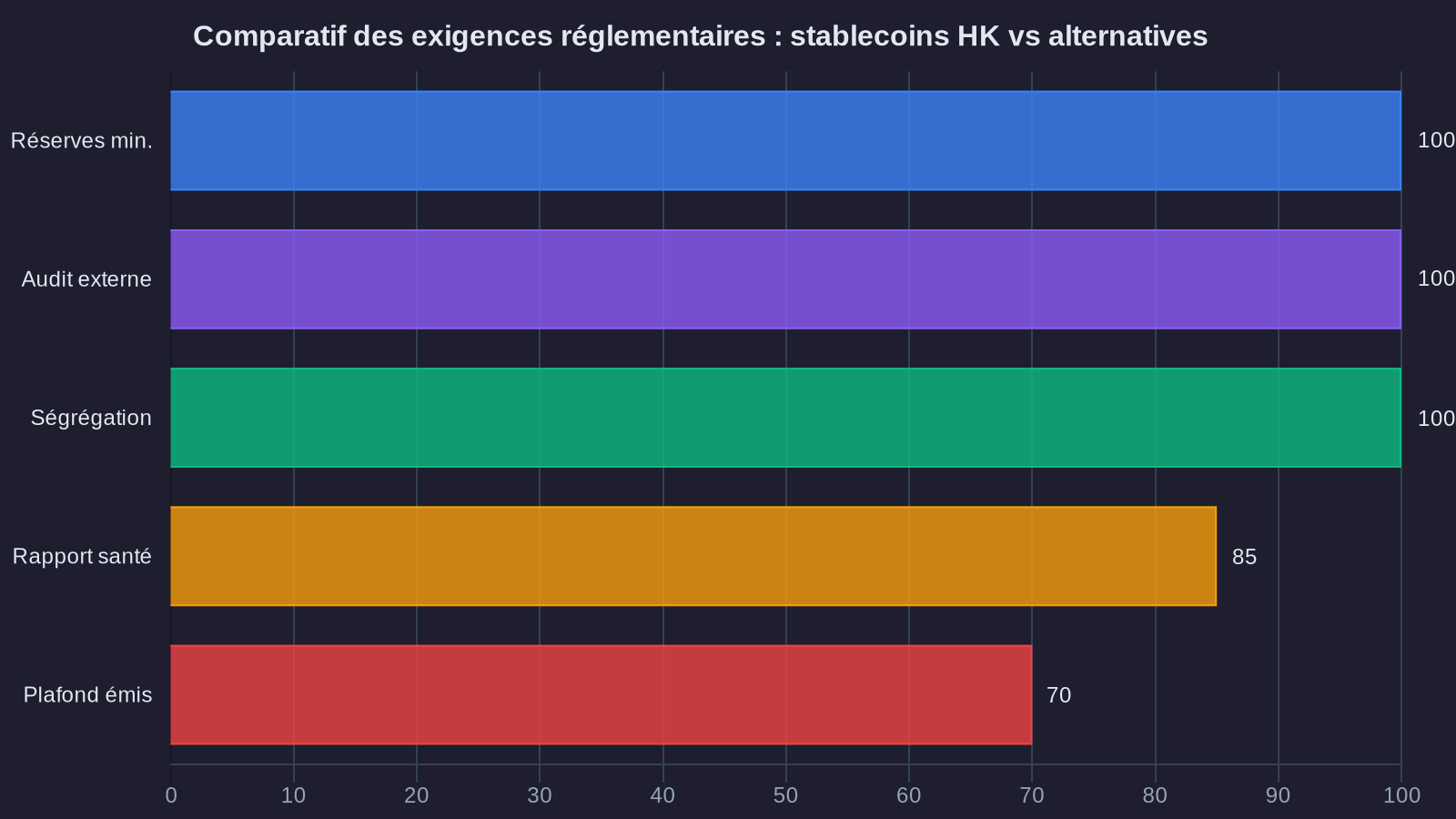

Hong Kong's regulatory framework: a departure from the status quo

Hong Kong adopted a specific licensing regime for stablecoin issuers in 2024, inspired by the European MiCA framework but with certain particularities. The stated objective: create a secure environment for institutional players who want to use regulated stablecoins without exposing themselves to regulatory grey areas.

Unlike existing stablecoins, which often operate in a partial legal vacuum, licensed issuers in Hong Kong must comply with strict requirements on reserves, asset segregation, and reporting. Reserves must be held in high-quality liquid assets, primarily bank deposits and short-term government securities. An independent auditor must verify monthly that the stablecoins in circulation are matched by adequate reserves.

For HSBC and Standard Chartered, this license represents far more than simple administrative compliance. It allows them to offer their corporate clients an alternative to traditional SWIFT transfers, with near-instantaneous settlements and reduced transaction costs, while remaining within the traditional banking perimeter. An executive already working with one of these banks can thus access stablecoins without opening an account with a crypto exchange.

Bank-issued stablecoins versus native stablecoins: what are the operational differences?

The question a CFO legitimately asks: how does a stablecoin issued by HSBC differ from USDC issued by Circle? In principle, the mechanism remains identical. A euro or dollar deposited generates an equivalent digital token, backed by verifiable reserves. But operational differences matter.

Bank-issued stablecoins benefit from the financial strength and credit ratings of the issuer. HSBC holds an A+ rating from S&P, Standard Chartered an A. This financial foundation offers a higher level of confidence for treasurers accustomed to the traditional banking hierarchy. In the event of market stress, a stablecoin issued by a systemically important bank theoretically presents less risk of losing its peg than one issued by a less well-capitalized structure.

Another notable difference: banking integration. An HSBC client holding HSBC stablecoins can instantly convert their positions into fiat currency through their existing current account, without going through an external intermediary. This fluidity reduces operational friction and settlement delays, representing a tangible advantage for a company managing significant international cash flows.

Conversely, these bank-issued stablecoins will likely have lower initial liquidity than dominant stablecoins. Circle's USDC boasts a capitalization in the tens of billions of dollars, with considerable market depth on major trading and DeFi platforms. An HSBC stablecoin, however well-designed, will take time to reach this level of liquidity. For an SME considering allocating 200,000 or 300,000 euros in stablecoins, this limitation may translate into wider spreads during conversions.

Implications for stablecoin yield strategies

The arrival of stablecoins regulated by financial institutions changes the game for companies seeking to generate returns on their treasury through stable currency investments. Currently, the main options consist of depositing USDC or USDT on decentralized finance protocols, or on centralized platforms like Coinbase or Kraken, with returns ranging between 3% and 6% depending on market conditions and risks taken.

With bank-issued stablecoins, one can anticipate the emergence of structured treasury products that resemble traditional interest-bearing accounts. HSBC could offer an account in HSBC stablecoins earning 2.5% or 3%, with a bank guarantee on the nominal capital, within the limits of applicable regulatory frameworks. This approach will appeal to treasurers seeking simplicity and security, even if potential returns remain lower than opportunities offered by DeFi.

For a company with 500,000 euros of excess cash, this yield difference has real impact. Placing this sum in bank-issued stablecoins at 2.5% generates 12,500 euros annually. The same amount deposited on a DeFi protocol at 5% yields 25,000 euros. But this straightforward comparison ignores risk profile. The DeFi protocol exposes the company to smart contract, liquidity, and counterparty risks that a bank account—even a digital one—does not entail.

The optimal strategy often consists of segmentation. One portion of treasury can be allocated to bank-issued stablecoins for their security and administrative simplicity, while a smaller fraction is invested in more dynamic yield protocols, with rigorous risk monitoring. This diversification allows for smoothing the return-risk trade-off and maintaining operational flexibility.

Tax and accounting: necessary clarifications

One of the persistent obstacles to crypto-asset adoption by companies remains their tax and accounting treatment. In France, stablecoins are subject to the tax regime for digital assets. For a company subject to corporate income tax, any capital gain on disposal is taxed at the standard corporate tax rate, currently 25% for income exceeding 38,120 euros.

The question becomes more complex when considering stablecoin valuation fluctuations. In principle, a stablecoin pegged to the dollar or euro maintains stable parity with the underlying currency. But in practice, minor deviations can occur, particularly during periods of market stress. A USDT trading at 0.98 dollars instead of 1 dollar technically generates a latent loss. Accounting for these fluctuations, even marginal ones, can burden administrative tracking.

Bank-issued stablecoins, due to their stricter regulatory anchoring, could benefit from simplified accounting treatment. If French tax authorities recognize that an HSBC stablecoin held on an HSBC account is functionally equivalent to a currency deposit, it would become possible to recognize these positions as liquid assets, without having to record fair value adjustments at each reporting period. This would be a significant gain in administrative simplicity for CFOs.

Currently, this clarification does not exist. Companies holding stablecoins must record them on the balance sheet as intangible assets or financial instruments, valued at reporting date according to IFRS standards or French accounting rules. This uncertainty hampers adoption, as a financial director hesitates to complicate reporting for an investment representing only a limited portion of treasury.

Gradual institutional adoption

The granting of licenses to HSBC and Standard Chartered marks an important symbolic milestone, but its short-term impact should not be overstated. Most companies will not shift massively toward bank-issued stablecoins overnight. Institutional adoption will occur gradually, as use cases become clearer and operational constraints are lifted.

Early adopters will likely be companies conducting frequent international transactions, particularly with Asia. A French SME regularly importing from Hong Kong or Singapore can use HSBC stablecoins to pay suppliers in near-real-time, bypassing traditional SWIFT circuits that take two to three days and incur currency exchange fees. This speed and cost advantage represents a tangible competitive benefit.

For companies considering integrating bank-issued stablecoins into their treasury strategy, several preliminary steps are required. First, verify that your banking partner actually offers this service in your jurisdiction, as licenses obtained in Hong Kong do not automatically apply in Europe. Next, evaluate conversion and holding costs: some issuers charge creation and redemption fees that can reduce investment attractiveness. Finally, it is essential to consult your accountant and tax advisor to anticipate specific accounting and tax implications for your situation.

A pragmatic recommendation: start with a limited trial. Allocate a modest sum, say 50,000 euros, to test the operational mechanics, measure actual costs, and assess ease of integration with your existing management processes. This experimental approach allows you to validate or refute the strategic interest without exposing a significant portion of your treasury.

What this evolution reveals about traditional finance and crypto convergence

Beyond practical considerations, HSBC and Standard Chartered's entry into the stablecoin market signals an ongoing convergence between the traditional banking system and the crypto ecosystem. For years, these two universes ignored or confronted each other. Banks denounced the risks of crypto-assets; crypto players criticized the slowness and opacity of the banking system.

Today, the boundary is blurring. Major banks acknowledge that blockchain technology offers real advantages in terms of speed, traceability, and transaction cost reduction. Crypto players, for their part, understand that regulation and institutional trust are essential to attract corporate and institutional investors.

This convergence opens interesting perspectives for chief financial officers. One can imagine, in a few years' time, hybrid banking services that combine balance sheet solidity with blockchain operational efficiency. A professional current account allowing simultaneous holdings of euros, dollars, and stablecoins, with instantaneous conversions and low-cost cross-border payments, becomes technically feasible.

But this convergence must not overshadow fundamental risks associated with crypto-assets. A stablecoin, even issued by a solid bank, remains exposed to technological and market risks. A blockchain failure, a cyberattack, or a generalized loss of confidence in crypto-assets can impact the liquidity and valuation of these instruments. Diversification remains the golden rule: no company should concentrate its entire treasury in stablecoins, even regulated ones.

The licenses obtained by HSBC and Standard Chartered in Hong Kong constitute a strong signal to the market. They indicate that regulated bank-issued stablecoins can become a legitimate component of corporate treasury strategies, provided they are integrated with rigor and discernment. For a CFO, this evolution does not justify an immediate overhaul of treasury management policy, but it merits careful monitoring and, if warranted, a phase of controlled experimentation. Potential returns and operational gains must always be weighed against the specific risks of this asset class. A prudent allocation, well-documented and validated by the company's governance bodies, remains the most reasonable path for exploring these new opportunities without compromising the organization's financial security.