In February 2025, the U.S. Congress passed the GENIUS Act (Guiding and Establishing National Innovation for US Stablecoins), legislation that requires stablecoin issuers to maintain full liquid reserves and forgo any deposit insurance scheme. This measure marks a strategic shift in U.S. crypto regulation: it enshrines the full-reserve model, but it also ends the illusion of traditional banking guarantees for stablecoin holders.

For business leaders considering integrating stablecoins into their treasury management or seeking to understand DeFi yields, this regulatory evolution fundamentally reshapes the landscape. The GENIUS Act clarifies certain gray areas, but it also redistributes risks among issuers, decentralized protocols, and end holders. Let's break down the concrete implications of this legislation for French SMEs exploring crypto diversification.

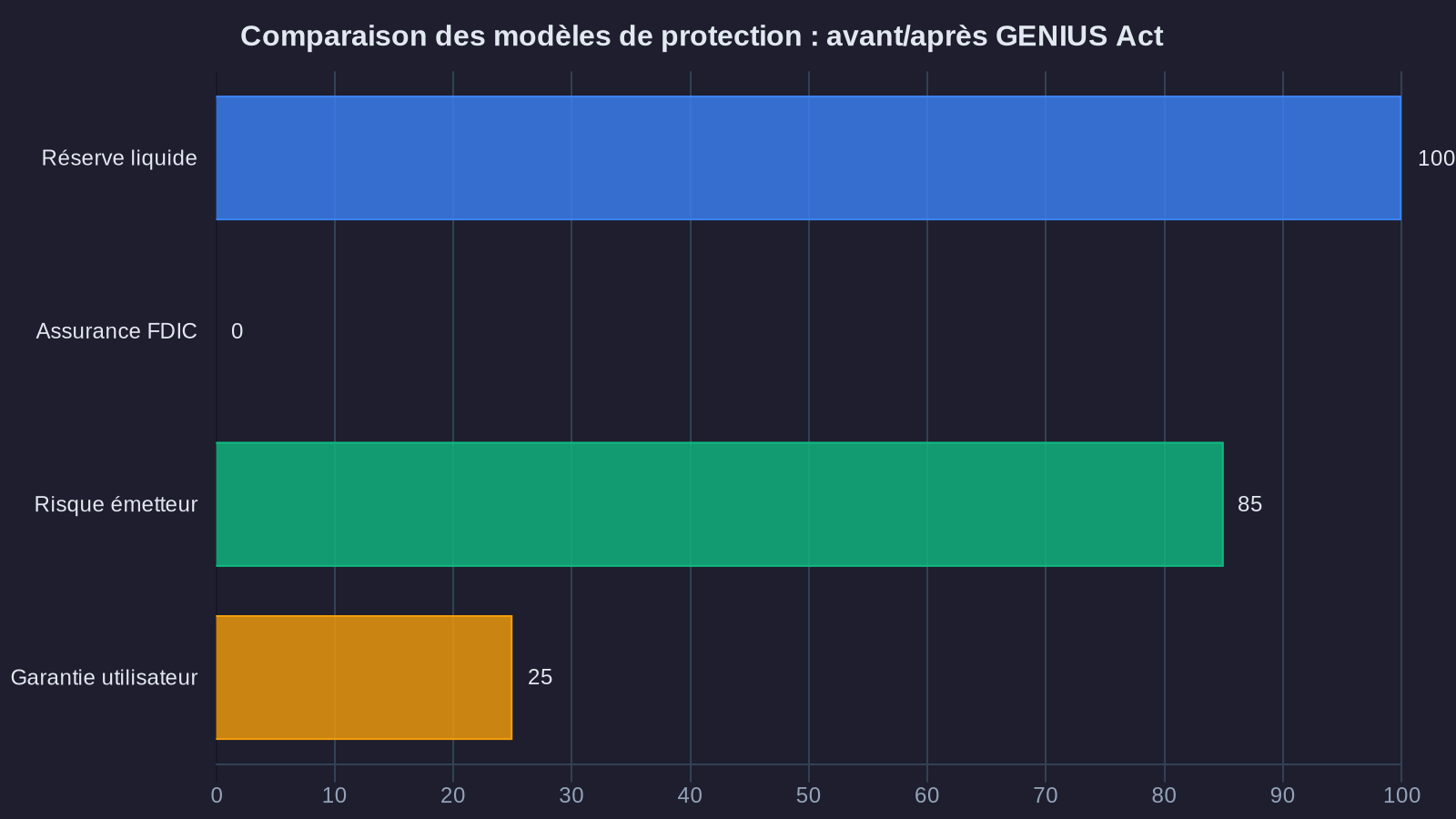

What the GENIUS Act Actually Imposes on Stablecoin Issuers

The GENIUS Act establishes a unified federal framework for stablecoins regulation United States 2025. Two requirements stand out: the obligation to maintain liquid reserves equal to 100% of circulating capitalization, and the formal prohibition on offering crypto deposit insurance of the FDIC (Federal Deposit Insurance Corporation) type to stablecoin holders.

In practice, an issuer like Circle (USDC) or Paxos (USDP) must now hold, for every dollar of stablecoin issued, a dollar in liquid assets or very short-term U.S. sovereign debt securities (Treasury bills under three months). This constraint strengthens issuer solvency, but it also eliminates any room to invest these reserves in higher-yielding assets. The model becomes that of a full-reserve bank, without money creation or leverage.

The prohibition on deposit insurance, for its part, puts an end to ambiguity. Some issuers had suggested that their stablecoins might benefit from protection similar to bank accounts insured by the FDIC. The GENIUS Act settles the matter: a stablecoin is not a bank deposit, and its holder fully assumes stablecoin counterparty risk on the issuer. If Circle or Tether encounter financial difficulties, no public funds will cover holder losses. This clarification requires companies to reassess the real risk of exposure to stablecoins, even the most reputable ones.

Direct Consequences for DeFi Yields

Decentralized finance (DeFi) relies heavily on stablecoins to offer attractive yields through staking, lending, or liquidity provision. Until now, protocols like Aave, Compound, or Curve allowed users to earn annualized returns of 3% to 8% by lending USDC or DAI, sometimes more during periods of high liquidity demand.

With the GENIUS Act, these yields risk declining for several reasons. First, stablecoin issuers can no longer generate significant revenue from their reserves: they must now profit solely through transaction fees or ancillary services. Second, regulatory clarity strengthens competitive pressure: issuers that fail to meet these reserve requirements will lose access to the U.S. market, concentrating supply among a few reference players.

For companies using stablecoins for treasury purposes, this evolution requires recalibrating expectations. A 5% DeFi yield on USDC remains feasible, but it now requires explicitly factoring in smart contract risk, counterparty risk on the issuer, and the absence of any public safety net. An SME placing €200,000 in excess liquidity in stablecoins to earn a DeFi yield must understand it assumes multiple layers of risk: that of the DeFi protocol itself (code vulnerabilities), that of the stablecoin issuer (under-collateralization or fraud risk), and that of on-chain rate volatility.

In this context, DeFi yields should no longer be compared to savings accounts or insurance-wrapped euro funds, but rather to speculative-grade corporate bonds. The compensation reflects real capital loss risk, not simply a liquidity premium.

What This Means for French SME Crypto Treasury Management

For a French SME finance director, the question is not whether the GENIUS Act is good or bad law, but how it reshapes the risk and opportunity landscape. Three elements warrant particular attention.

First, the U.S. regulatory framework will gradually influence the European framework. The MiCA regulation (Markets in Crypto-Assets), which came into force in 2024, already imposes strict reserve requirements for stablecoins issued or distributed in the European Union. With the GENIUS Act, we see transatlantic convergence: both blocs prioritize transparency, reserve liquidity, and prohibition of public guarantees. This means stablecoins meeting U.S. standards will likely enjoy facilitated passporting to Europe, and vice versa. For a French company, it becomes strategically important to favor stablecoins regulated on both sides of the Atlantic, like Circle's USDC or EURC.

Second, the GENIUS Act indirectly strengthens stablecoin credibility as short-term treasury instruments, but does not transform them into risk-free liquidity equivalents. A company holding €500,000 in USDC to finance international payments or smooth exchange-rate fluctuations must explicitly integrate into its risk management policy the fact that no public mechanism will protect it if the issuer fails. This requires diversifying issuers (not concentrating all crypto treasury in a single stablecoin), actively monitoring reserve audits published monthly, and limiting overall crypto-asset exposure.

Third, the absence of deposit insurance requires rethinking allocation between stablecoins held in custody (cold wallet or regulated platform) and stablecoins deployed in DeFi. A prudent strategy involves segmenting crypto treasury into three buckets: an immediate liquidity bucket (stablecoins in custody, zero yield but limited issuer risk), a moderate-yield bucket (stablecoins staking on audited, widely-used protocols, 3% to 5% yield), and a higher-yield but more volatile bucket (exposure to niche DeFi protocols or yield farming strategies, potential 8% to 12% yield but material loss risk). This segmentation allows calibrating risk exposure according to investment horizon and the company's liquidity needs.

Toward Inevitable Stablecoin Ecosystem Professionalization

The GENIUS Act accelerates an underlying trend: professionalization of the stablecoin ecosystem. The players who will survive this regulatory wave are those with sufficient financial capacity to maintain full reserves, who accept regular audits, and who renounce misleading marketing promises about stablecoin absolute safety.

For companies, this clarity is good news medium-term. It reduces the risk of systemic events like the Terra/Luna collapse, where a poorly designed algorithmic stablecoin triggered tens of billions in losses within days. It also strengthens traceability and transparency, two criteria essential for auditors and statutory auditors who must certify accounts of companies holding crypto-assets.

However, this evolution also marks the end of a certain naïveté. Stablecoins are not fiat currency equivalents, and DeFi yields are not risk-free returns. An SME integrating stablecoins into treasury management must do so with the same rigor it applies to bond investments or bank financing: documentation of risks, limitation of amounts deployed, diversification of counterparties, and regular strategy review based on regulatory evolution and market conditions.

The GENIUS Act closes no doors, but it requires crossing each threshold with eyes open. For a finance director, this means an allocation of 5% to 10% of available treasury to stablecoins remains feasible, provided you explicitly accept capital loss risk and never treat these assets as alternatives to money market funds or short-term instruments. Crypto diversification becomes a deliberate, documented, and proportionate treasury management decision reflecting the company's capacity to absorb potential loss. This is precisely the rigorous approach that will allow French SMEs to capitalize on yield opportunities offered by stablecoins and DeFi, without turning their treasury into speculative testing ground.