Imagine you could buy an Apple share at 3 in the morning from Tokyo, have the transaction validated in 400 milliseconds, and pay a fraction of a cent. Then resell it an hour later to a Brazilian investor, bypassing any banking intermediary. This vision isn't futuristic at all: it's exactly what Solana already enables for tokenized financial securities in 2026.

Since 2023, institutional players have been massively testing the tokenization of financial securities. BlackRock, Fidelity, JPMorgan: they're all experimenting with this technology that transforms stocks, bonds, or fund units into tokens that can be exchanged on blockchain. One thing is becoming clear: while Ethereum dominated these early experiments, Solana has gradually established itself as the infrastructure of choice for large-scale deployments with its record institutional adoption on the network.

This shift is no accident. It reveals a deeper truth about what financial institutions really seek when they adopt blockchain.

Speed as competitive advantage: real-time settlement

To understand why Solana is winning, you first need to grasp what a tokenized stock really is. It's as if your traditional stock certificate became a digital token: you keep exactly the same rights (dividends, voting, ownership), but this token can circulate 24/7 on a blockchain instead of through traditional banking channels.

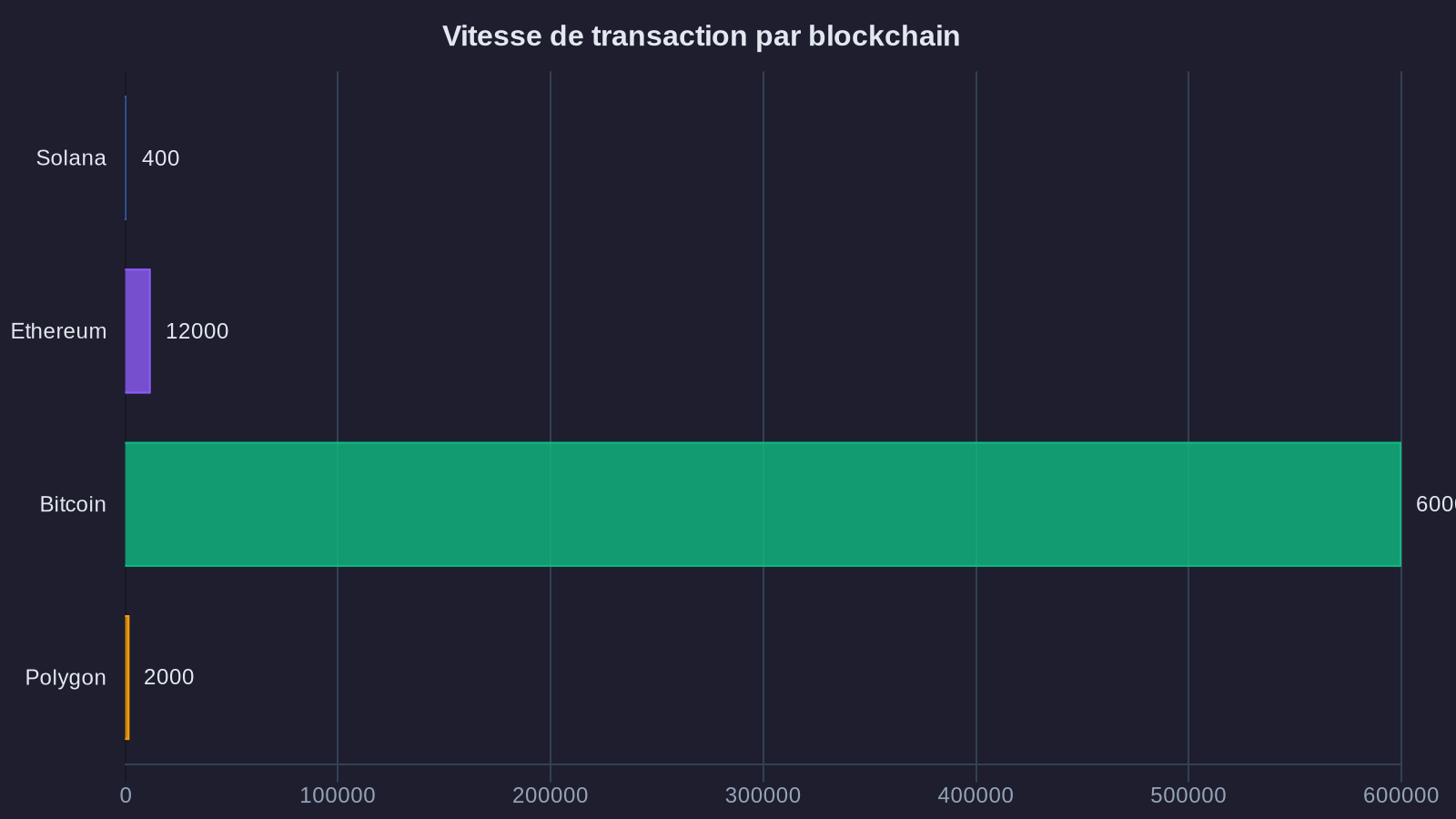

The difference? Execution speed. On traditional markets, settlement of a stock takes two business days (T+2). Even the most modern systems don't go below that. Ethereum, the first blockchain tested for these use cases, validates a transaction in 12 to 15 seconds. Solana? 400 milliseconds on average for genuine real-time settlement.

This difference may seem trivial. It's not. In institutional finance, every second your capital is tied up represents an opportunity cost. A fund managing 500 million euros and rebalancing its positions daily doesn't look at those 400 milliseconds the same way a retail investor would. For these players, it's the difference between a system that scales and a technological curiosity.

Let's take a concrete example: in September 2024, Hamilton Lane tokenized 2.1 billion dollars in private equity assets on Solana. The fund now allows its institutional investors to redeem their shares in less than a day, compared to a minimum of 90 days in the traditional system. This additional liquidity fundamentally changes the risk-return equation of these typically illiquid investments.

The economics that swayed institutions: Solana as an Ethereum alternative

Speed is just one factor. The other decisive element is cost. And here the numbers speak for themselves in this alternative to Ethereum.

A transaction on Ethereum costs between 2 and 50 dollars depending on network congestion. That's acceptable for transferring 100,000 dollars, but becomes prohibitive for smaller amounts. Solana charges approximately 0.00025 dollars per transaction. Always. Regardless of network congestion.

This predictability changes everything for institutions. It's like if the postal service charged the same postage whether you send a letter on a quiet Tuesday morning or on December 24th. In an environment where you're potentially processing hundreds of thousands of transactions daily (think automatic portfolio rebalancing), this cost predictability becomes a major decision criterion.

Franklin Templeton understood this well. The American asset manager, which oversees more than 1.5 trillion dollars, launched its tokenized money market fund on Solana in 2024. Their calculation was straightforward: with 50,000 investors performing an average of one transaction per week, Ethereum would have cost them between 5 and 125 million dollars annually in transaction fees. On Solana, this cost drops below 1,000 dollars. Not 1,000 dollars per day. 1,000 dollars per year.

This savings doesn't just benefit asset managers. It flows directly to the fees charged to end investors. And in a sector where every basis point matters, that's a decisive competitive advantage.

The use cases that are actually emerging beyond the marketing pitch

Let's talk concrete. What are institutions actually doing with Solana tokenized securities trading today? Three use cases stand out clearly.

First use case: tokenization of investment funds. This is the most mature. Players like WisdomTree or 21Shares now offer crypto ETFs whose shares are directly issued as tokens on Solana. The benefit? An institutional investor can buy shares at 2 in the morning, transfer them instantly to their custody platform, and use them as collateral for other financial operations. All without waiting for market opening, without manual validation, without settlement delays.

Second use case: corporate bonds. Sygnum Bank issued in 2024 a tokenized bond of 50 million Swiss francs on Solana for a corporate client. Bondholders receive their coupons automatically via smart contract, without intervention from a paying agent. The system manages distribution, rights verification, and payment proof archiving itself. Result: operational costs divided by 20 over the bond's lifetime.

Third use case, more recent: fractional shares. Imagine being able to buy 0.01 Amazon shares rather than one whole share at 3,000 dollars. Tokenization has made this technically possible for a while, but transaction costs made this granularity impractical. On Solana, fractionalization becomes economically viable. Backed Finance allows you to buy fractional shares of the S&P 500 for as little as 10 dollars, with negligible transaction fees.

These three examples share one point in common: they wouldn't be economically viable on Ethereum in its current configuration. It's not a question of absolute technical superiority, but of fit between a blockchain's characteristics and a market's real constraints.

The obstacles that remain for tokenized stocks on blockchain

Let's be clear: Solana doesn't solve all the problems of financial securities tokenization. Three major challenges persist.

First, regulatory issues. A tokenized financial security remains a financial security. It must comply with the same compliance obligations, reporting requirements, and anti-money laundering standards. But European and American regulators haven't yet harmonized their positions on the exact legal status of these tokens. MiCA in Europe provides an initial framework, but gray areas remain. Notably on who is responsible in case of a smart contract bug.

Next, interoperability. If your securities are on Solana and your custodian bank uses Ethereum, how do you ensure compatibility? Bridge projects exist, but they introduce additional technical risks. The industry hasn't yet converged on a single standard.

Finally, governance. Solana is a relatively young blockchain that experienced several major outages in 2022-2023. For an asset manager bearing fiduciary responsibility, betting on infrastructure that can go down for several hours represents a non-negligible operational risk. Recent network stability is reassuring, but the scars of these incidents linger in institutional memory.

What's emerging for Solana tokenized securities trading in 2026

The signals are nonetheless clear: the infrastructure is professionalizing rapidly. Fireblocks, Anchorage, and BitGo now offer institutional custody solutions on Solana. Security audits are multiplying. Connections with traditional banking systems are improving.

There's also an interesting phenomenon emerging: players who first tested tokenization on Ethereum are gradually migrating their highest-volume operations to Solana, while keeping Ethereum for specific use cases (notably complex DeFi where Ethereum's ecosystem remains more mature). This multi-chain approach is becoming standard among the most advanced institutions.

The real test will come when a significant-scale issuer (think a top-10 global bank) tokenizes an entire public bond offering on Solana. Several projects are in preparation for 2025-2026. Whoever crosses that line first will set a precedent that will massively accelerate adoption.

Because that's what this is really about: a gradual shift, not overnight revolution. Tokenized financial securities won't replace traditional stocks in 2026. But they'll likely represent 2 to 5% of new securities issuance volume. And that share will continue growing, driven by economic advantages that become too significant to ignore.

Solana isn't winning because it's the most decentralized blockchain, the most secure, or the oldest. It's winning because it solves concrete problems faced by institutional players managing real money. In finance, it's often this pragmatism that tips infrastructure decisions.