For decades, the institutional fixed income revenue stack relied on a simple architecture: sovereign bonds, corporate credit, money market products. Predictable returns, known counterparties, well-established processes. Then 2022 arrived with negative rates followed by a sharp rise, and many capital allocators realized their toolkit was showing its limits.

Meanwhile, DeFi was quietly building an alternative for institutions. Not a flashy revolution, but a methodical reconstruction of the very logic of fixed income: how to generate yield on capital without relying on a central issuer, how to structure credit risk without rating agencies, how to distribute liquidity without banking intermediaries.

What seemed experimental three years ago is gradually becoming a strategic building block for institutional allocators seeking to diversify their yield sources. Let's look at how this transformation is actually happening.

Traditional fixed income facing its own limits

Fixed income desks at major institutions face an uncomfortable equation. On one hand, pressure on returns is intensifying: allocators have commitments to honor, liabilities to cover. On the other, traditional fixed income sources are showing structural weaknesses.

The European sovereign bond market spent years in negative territory. Result: billions of euros in capital desperately seeking yield, accepting increasingly compressed risk premiums for increasingly longer durations. Corporate credit offers spreads, certainly, but sector concentration becomes problematic when managing significant ticket sizes.

More fundamentally, the traditional stack suffers from structural rigidity. An institutional bond fund wanting to adjust its exposure must work through counterparties, wait for T+2 or T+3 settlements, manage considerable liquidity friction. This friction carries a cost, especially when market conditions evolve quickly.

This is precisely where institutional DeFi proposes a different approach. Not inherently better, but structurally distinct in how it generates and distributes yield.

How DeFi reconstructs institutional fixed income logic

Decentralized finance isn't trying to replicate bonds. It reconstructs the very function of fixed income from different economic primitives. Three main mechanisms are emerging as credible alternatives for institutional capital.

Lending protocols: credit without a central issuer

Imagine a money market where credit supply and demand balance in real time, without a credit committee or risk department. That's exactly what protocols like Aave or Compound do. You deposit stablecoins (USDC, USDT, DAI), the protocol makes them available to borrowers who post crypto-asset collateral, you receive a yield that fluctuates based on pool utilization.

For an institutional fixed income desk, this is a dollar yield source with interesting characteristics: instant liquidity, no traditional duration risk, no central counterparty to analyze. Risk shifts: it's no longer issuer default risk, it's smart contract risk and insufficient collateral liquidation risk.

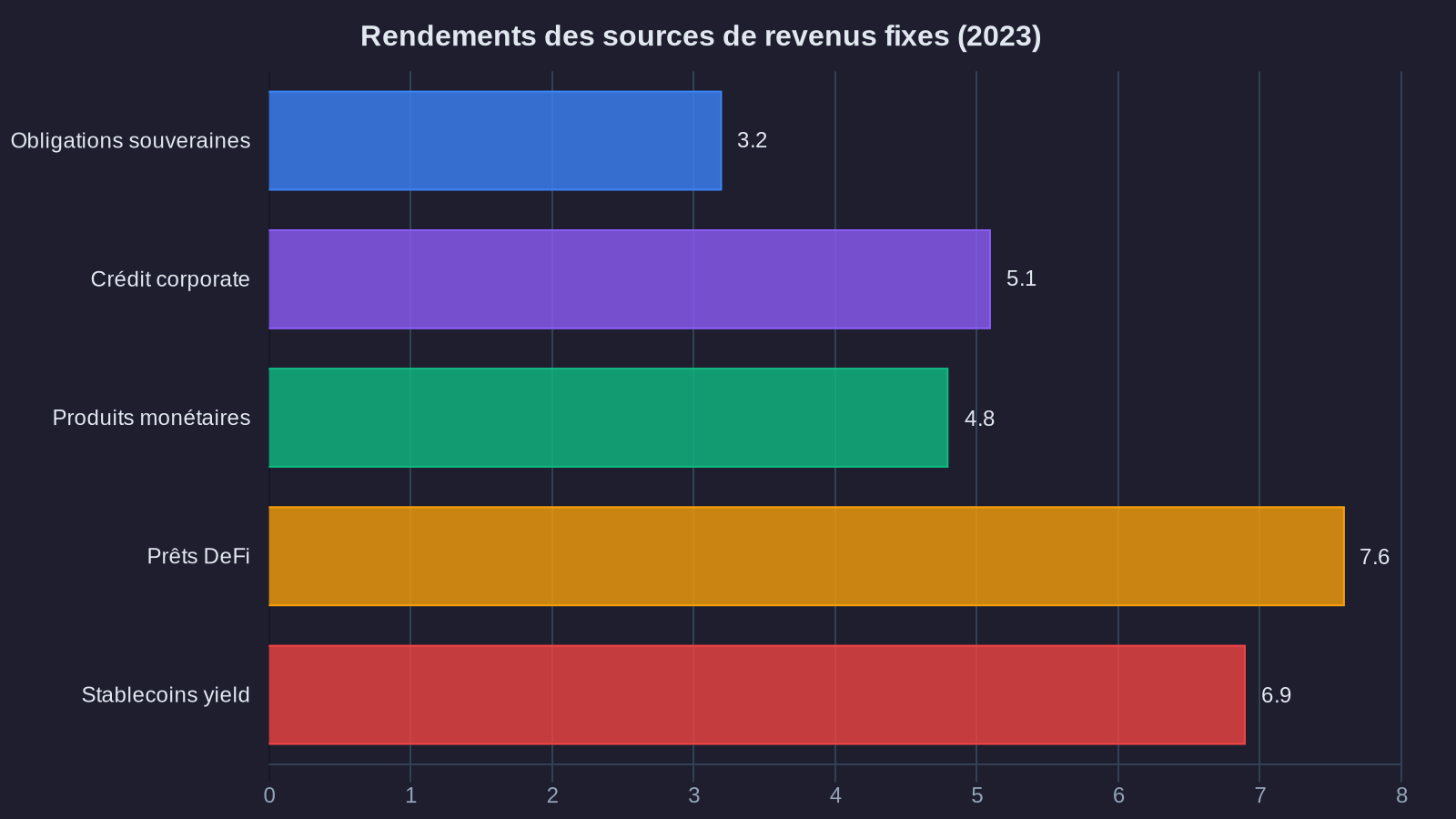

Crypto fixed income yields typically range between 2% and 8% depending on market conditions and the deposited asset. Less spectacular than the three-digit APYs of 2020, but aligned with what an institutional allocator can integrate into a diversified yield strategy.

Liquid staking: transforming an asset into yield

Ethereum post-Merge created a new fixed income primitive: native staking yielding approximately 4% annually. But locking ETH for weeks as a validator is unacceptable for an institutional manager needing liquidity.

Liquid staking protocols (Lido, Rocket Pool) solve this equation. You deposit ETH, you receive a token representing your staked ETH (stETH, rETH) that continues accumulating staking rewards. This token remains liquid, tradable, usable in other DeFi protocols.

For an institution already holding ETH on its balance sheet (and many now do, even just for blockchain infrastructure reasons), this is a way to transform a dormant asset into a productive asset without sacrificing liquidity. The yield is predictable, indexed to Ethereum's consensus mechanics, with volatility dependent on the underlying asset, not the protocol itself.

Yield-generating stablecoin arbitrage strategies

Here's where things get really interesting for institutional desks seeking uncorrelated yield. The stablecoin market generates permanent arbitrage opportunities that DeFi protocols enable systematic exploitation of.

Concrete example: DAI (MakerDAO's decentralized stablecoin) sometimes trades slightly above or below its $1 peg. A protocol like Curve, specialized in stablecoin swaps, offers liquidity pools where you can deposit multiple stablecoins and capture arbitrage fees from traders rebalancing these pools.

Stablecoin yields are typically lower (1% to 4%), but with very contained volatility since you stay within the stablecoin universe. This is a yield component that functions like enhanced money market products. Some institutions see this as an alternative to traditional treasury placements, with superior liquidity and slightly better returns.

Institutional arbitrage opportunities: where the real value lies

Now, let's talk about what really interests professional allocators: the structural arbitrages that institutional DeFi makes possible and that traditional finance can't exploit as efficiently.

Cross-protocol liquidity arbitrage

Different DeFi protocols offer different yields for the same asset at the same time. USDC might yield 3% on Aave, 4.5% on Compound, 2.8% on a Curve pool. These gaps aren't inefficiencies that disappear in seconds (like equity markets), they persist because each protocol has its own supply-demand dynamics.

For an institutional desk with the right tools, this is a low-risk arbitrage opportunity: move capital between protocols to capture these spreads. DeFi makes these moves nearly instantaneous and low-cost. Compare that to traditional fixed income, where reallocating capital between different bond compartments takes days and generates considerable friction.

Decentralized yield curve arbitrage

Some protocols explicitly construct on-chain yield curves. Notional Finance, for instance, allows trading fixed rates on different maturities. You can take a position on the DeFi yield curve shape, exactly like a rates desk would on the sovereign curve.

The interest? These DeFi yield curves aren't correlated to traditional sovereign curves. They depend on demand for on-chain leverage, protocol liquidity, crypto-market dynamics. For an allocator seeking to diversify fixed income sources, this is a structurally different exposure.

Carry on productive collateral

Here's a strategy that simply doesn't exist in traditional finance. You stake ETH to receive stETH generating 4% yield. You deposit that stETH as collateral on Aave to borrow stablecoins. You redeploy those stablecoins in a Curve liquidity pool yielding 3%.

Result: you capture staking yield on your collateral AND yield on the borrowed stablecoins, while maintaining your ETH exposure. It's leveraged carry, but structured transparently and with liquidity. Risks are explicit (liquidation if ETH drops too much, smart contract risk), but quantifiable.

Family offices and crypto-native hedge funds already run these strategies with eight-figure tickets. What was experimental in 2021 is gradually becoming a standard allocation building block.

Institutional constraints: why adoption remains gradual

Let's be clear: we're not on the brink of massive institutional fixed income desks pivoting to DeFi. The brakes are real and structural.

The custody question remains central. An institutional bond fund can't afford to manage private keys on a Ledger. You need qualified custody solutions with asset segregation, insurance, robust governance procedures. These solutions now exist (Fireblocks, Copper, Anchorage), but they add costs and operational constraints.

The regulatory framework is evolving but remains fragmented. A European UCITS manager can't allocate to DeFi with the same rules as a US hedge fund subject to the Investment Company Act. Interpretations differ between jurisdictions, between regulators, sometimes even between legal departments of the same institution.

Smart contract risk remains the subject that makes risk committees wince. A protocol may have been audited by three different firms, it's still code that could contain vulnerabilities. We saw this with the 2022-2023 exploits. For an allocator whose mandate is capital preservation, this risk is hard to accept at scale.

But these constraints are gradually easing. DeFi insurance is professionalizing. Smart contract audits are becoming more systematic and rigorous. Especially, institutions are developing internal expertise: they're hiring profiles that understand DeFi, they're building adapted risk analysis frameworks, they're testing on small tickets before scaling.

Toward a hybrid approach in institutional fixed income strategies

The most likely scenario for the coming years isn't traditional fixed income replaced by DeFi. It's a progressive hybridization, where certain institutions integrate DeFi building blocks into their overall allocation to diversify yield sources.

We're already seeing this shift begin. Family offices are allocating 5% to 10% of their fixed income pocket to DeFi strategies managed by specialists. Macro hedge funds are integrating DeFi positions into their rates book. Corporate treasuries are testing treasury placements on lending protocols to improve cash returns.

What makes this evolution structural is that institutional DeFi offers something traditional fixed income simply can't replicate: near-instantaneous liquidity, complete position transparency, composability that enables sophisticated strategy construction without relying on central counterparties.

For institutions taking the time to understand these mechanics, build necessary infrastructure, and train their teams, DeFi becomes an allocation tool in its own right. Not a speculative bet on crypto-assets, but a structurally different way to generate fixed income yield on capital.

The question is no longer whether institutions will integrate DeFi into fixed income strategies. It's at what pace, and which institutions will gain an edge by building this competency now rather than waiting for the market to mature further.