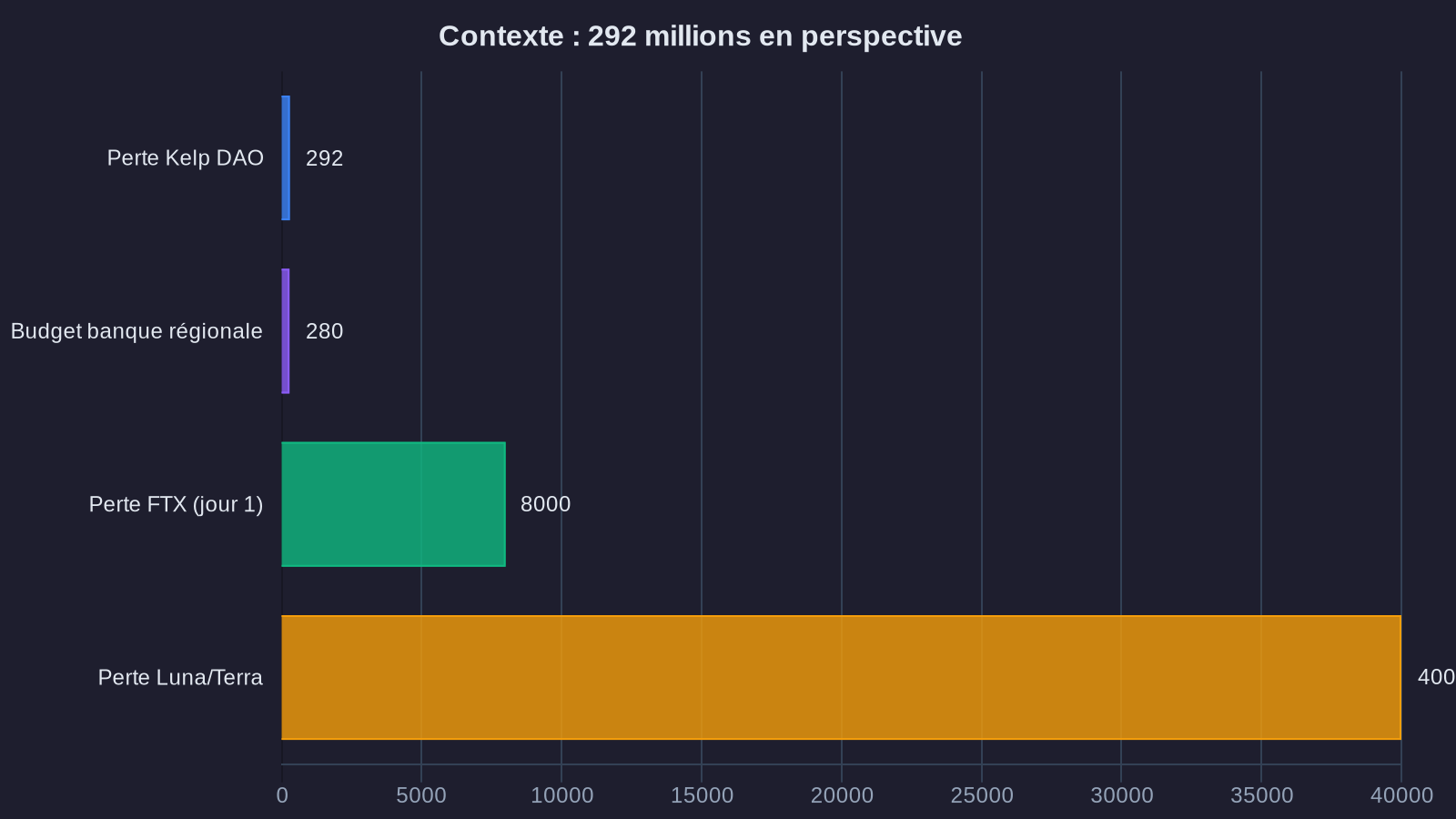

On April 17, 2024, Kelp DAO, a liquid staking protocol built on Ethereum, lost $292 million in just a few hours. A figure that's hard to wrap your head around. To put it in perspective: that's equivalent to the annual budget of a mid-sized European regional bank evaporating overnight.

What makes this Kelp DAO exploit particularly fascinating is that it combines everything that both captivates and terrifies institutional investors in DeFi: cutting-edge technical innovation, DeFi security risks that are routinely underestimated, and an impressive collective response from the ecosystem to limit the damage. Let's break down what actually happened, and more importantly, what this episode reveals about the maturity of decentralized finance.

What happened: anatomy of a $292 million exploit

Kelp DAO offered a service that appeals to many investors: liquid staking. Imagine depositing money into a savings account, but instead of locking up your funds, you receive a certificate that you can use elsewhere to generate additional income. That's exactly how liquid staking works.

You deposit your ethers (ETH) into the protocol and receive rsETH tokens in exchange (digital "receipts"), and these rsETH can be used in other DeFi protocols to borrow, lend, or provide liquidity. Meanwhile, your ETH continues to generate staking rewards. An elegant mechanism, in theory.

The attacker exploited a flaw in the rsETH pricing system. In simple terms: the protocol used an oracle (a system that provides price data) that could be manipulated. The attacker managed to convince the system that their rsETH was worth far more than its actual value, then borrowed massive sums based on that inflated value. Once the funds were borrowed, they transferred them out of the protocol. All in just a few transactions.

The technical flaw lay in the architecture of the price validation system. Kelp DAO relied on a calculation mechanism based on the ratio between deposited assets and issued tokens. But this ratio could be temporarily distorted by coordinated transactions, creating a window of opportunity spanning just a few seconds. Enough for a prepared attacker.

The response: when the Aave bailout DeFi kicks in to save the day

What distinguishes this exploit from previous ones is the speed and coordination of the response. Within two hours, several major DeFi players mobilized. Aave, the largest decentralized lending protocol, immediately froze all markets linked to rsETH to prevent the attacker from liquidating additional positions.

At the same time, a coalition called "DeFi United" formed spontaneously. It brought together developers from different protocols, blockchain security teams, and even professional traders. Their goal: track the attacker's fund movements, block their attempts to convert to untraceable assets, and negotiate a potential return of the stolen funds.

This collective mobilization bears some resemblance to emergency response teams in traditional finance, except here, everything happened open-source, in real-time, with teams that had never met in person. A fascinating paradox: DeFi, often criticized for its lack of oversight, demonstrated a remarkable capacity for self-organization.

The strategies deployed in this rsETH recovery plan included:

- Immediate freeze of exposed markets on Aave, Compound, and other lending protocols

- Forensic analysis of transactions to trace stolen funds across different blockchains

- Coordination with centralized exchanges to blacklist the attacker's addresses

- Implementation of a bounty (white hat bounty) to incentivize the attacker to return the funds

Ultimately, approximately 40% of the funds were recovered or frozen. That's both encouraging and insufficient. For an institutional investor, losing 60% of committed capital remains unacceptable, regardless of how effective the post-incident response was.

DeFi security lessons: persistent structural flaws

This exploit highlights several structural flaws that persist in the DeFi ecosystem, despite years of evolution.

First, the oracle problem. DeFi protocols need reliable data about asset prices to function. But providing this data in a decentralized and manipulation-resistant way remains an unsolved challenge. Kelp DAO used a system that appeared robust under normal conditions but proved vulnerable against a determined attacker.

Imagine an ATM that would accept any piece of paper as currency, as long as it had the right dimensions. That's essentially what happened here: the system verified certain criteria, but not the right ones.

Second, the growing complexity of protocols creates exponential attack surfaces. Kelp DAO combined several mechanisms: liquid staking, cross-chain bridging, yield optimization. Each added component multiplies possible interactions, and thus potential attack scenarios. Security audits, even conducted by reputable firms, cannot anticipate all possible combinations.

Third, there's the question of emergency governance. Most DeFi protocols are designed to be decentralized and censorship-resistant. But in a crisis, that decentralization becomes a handicap. Kelp DAO lacked mechanisms to quickly freeze compromised contracts. Adding these mechanisms means reintroducing a form of centralization. Not having them means accepting a structural vulnerability.

Implications for institutional adoption of DeFi

For institutional investors watching DeFi with a mix of interest and caution, the Kelp DAO exploit impact on institutional DeFi sends contradictory signals.

On one hand, the ecosystem's ability to mobilize quickly demonstrates growing operational maturity. Major protocols like Aave have proven emergency procedures. Security teams collaborate effectively. The infrastructure for tracing and forensic analysis is constantly improving. These are encouraging signs.

On the other hand, the frequency and scale of exploits remain incompatible with institutional fiduciary requirements. A family office or pension fund can't explain to its clients that it lost 60% of an allocation because an oracle was manipulated for three seconds. Financial regulators, already skeptical, see this as confirmation of their concerns.

The fundamental problem is that DeFi operates according to different logic than traditional finance. In classical finance, security relies on trusted intermediaries, insurance, legal guarantees. In DeFi, security relies on code, economic incentives, and transparency. These two models are difficult to reconcile.

Some institutional players are beginning to explore hybrid solutions: use DeFi protocols, but through custodial interfaces that add layers of traditional protection. It's a pragmatic compromise, even if it sacrifices some of the value proposition of decentralization.

We're also seeing the emergence of DeFi protocols specifically designed for institutional investors, with more restrictive governance mechanisms, more rigorous audits, and sometimes whitelists of authorized users. These protocols are less philosophically "pure," but more acceptable from a regulatory and fiduciary standpoint.

Toward a two-speed DeFi?

The Kelp DAO exploit illustrates a tension running through the DeFi ecosystem: should we prioritize rapid innovation and open accessibility, or security and regulatory compliance?

The answer seems to be: both, but not in the same protocols. A two-speed DeFi is taking shape. On one side, experimental, highly innovative protocols that accept high risks in exchange for potentially superior returns. On the other, more conservative protocols, exhaustively audited, with reinforced security mechanisms, specifically targeting institutional investors.

This bifurcation isn't necessarily negative. It allows innovation to continue progressing rapidly, while building safer rails for capital that can't tolerate extreme volatility. The challenge will be maintaining interoperability between these two worlds.

For institutional investors interested in DeFi, the Kelp DAO exploit offers several practical lessons. First, diversification is crucial: no protocol, however audited, is completely safe. Second, size matters: protocols with several billion TVL (Total Value Locked) generally have more robust security mechanisms and a more active community to respond to incidents. Finally, code transparency and security track record should take priority over yield promises.

The future of institutional crypto adoption will likely pass through more sophisticated risk management frameworks that borrow from both traditional practices (stress tests, diversification, hedging) and blockchain specifics (on-chain analysis, real-time monitoring, automated recovery mechanisms). Kelp DAO will have been, despite itself, a catalyst to accelerate this necessary maturation.