On March 14, 2025, the U.S. Federal Reserve published an update to its master account access criteria. An announcement that slipped under the radar in mainstream media, but one that marks a turning point for the crypto and fintech industry. For the first time in years, the Fed is clarifying and broadening the conditions allowing non-banking institutions direct access to the federal payments system.

Why does this matter? Because a Federal Reserve master account is far more than a standard bank account. It's direct access to U.S. payment rails, the ability to hold federal reserves without intermediaries, and most importantly, regulatory legitimacy in a sector where trust is everything.

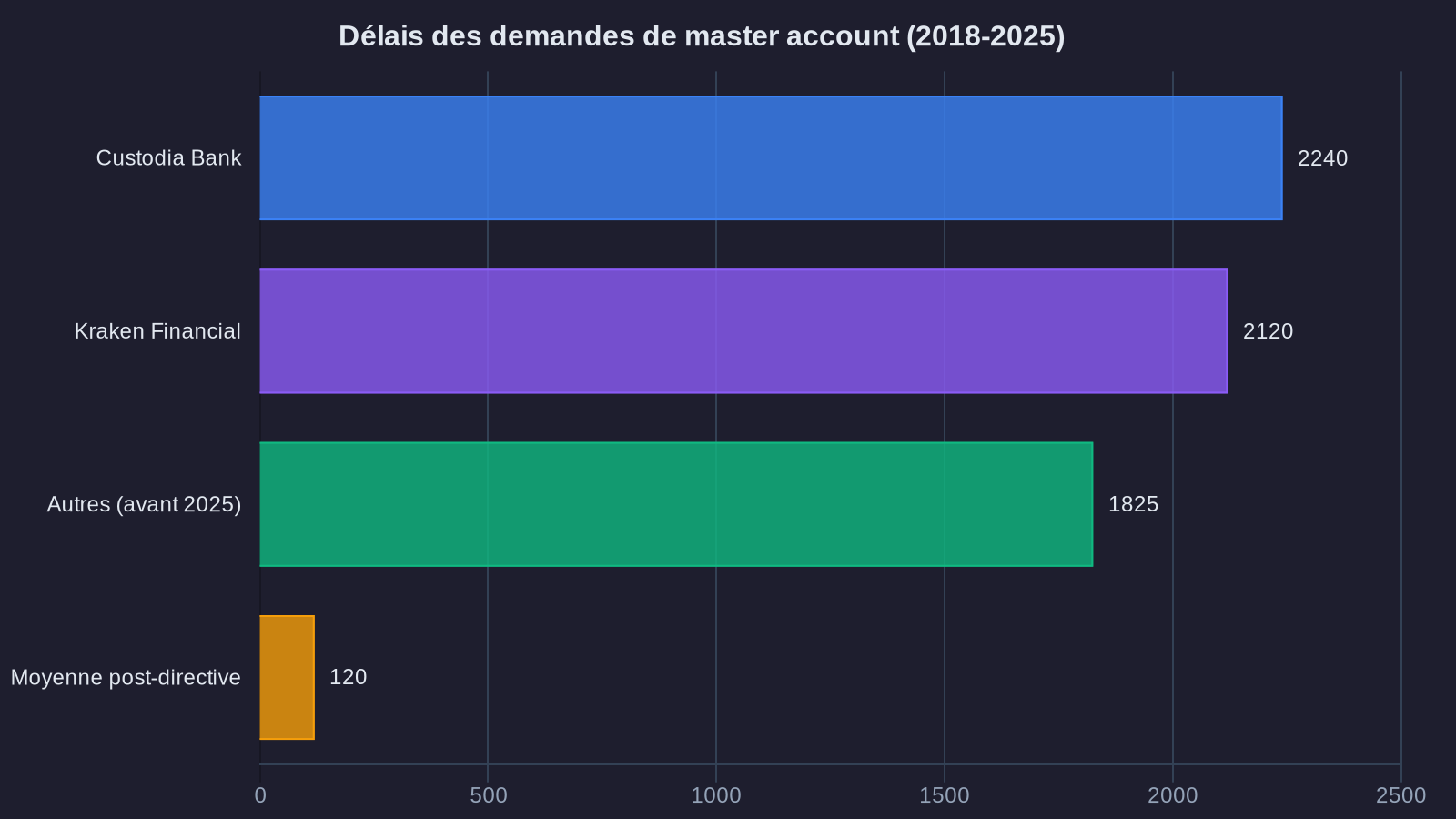

Context: since 2018, several major crypto players (including Custodia Bank and Kraken Financial) have been fighting in court to obtain these Federal Reserve master accounts. The Fed repeatedly refused, citing systemic risks and the lack of an appropriate framework. The new directive fundamentally changes the game by facilitating crypto banking access for qualified institutions.

What a Federal Reserve master account actually enables

A master account is the gateway to the American banking system. Technically, it's an account held directly with one of the twelve regional Federal Reserve banks. This account enables three fundamental things.

First, access to Fed payment services: Fedwire (for large interbank transfers), FedACH (for automated retail payments), and soon FedNow (the Fed's instant payments system launched in July 2023). Without a master account, a fintech must go through a partner bank, which adds costs, delays, and most importantly, strategic dependence.

Second, the ability to hold federal reserves. Funds deposited in a master account are direct liabilities of the Fed, considered the safest asset in the American financial system. For a crypto company managing billions in stablecoins, being able to back these tokens with federal reserves rather than commercial bank deposits fundamentally changes the risk profile.

Finally, access to the Fed's discount window in case of liquidity crisis. It's the ultimate safety net for the banking system. Crypto players are currently excluded from this, making them particularly vulnerable during stress periods (as we saw with Silicon Valley Bank's collapse in March 2023, which nearly took down Circle and its USDC stablecoin).

New master account access criteria: what's changed

The March 2025 directive introduces a three-tier framework based on systemic risk levels and the nature of activities. The first tier covers institutions with assets exceeding $10 billion or managing critical market infrastructure. These players undergo enhanced evaluation including stress tests and regular Fed audits. Circle, Coinbase Custody, and Paxos fall into this category.

The second tier targets mid-sized institutions (between $1 billion and $10 billion in assets) with primarily domestic operations. The approval process is streamlined but imposes capital and liquidity ratios aligned with Basel III. This is the main target of this opening: allowing serious but mid-sized players to access the system without years of legal battles.

The third tier remains restrictive: pure-play crypto operators without full banking licenses (special purpose depository institutions or SPDIs) must demonstrate complete separation between crypto and deposit-taking activities. This is the compromise the Fed found to prevent direct contamination of the payment system by crypto volatility.

Critical point: the Fed now imposes a maximum 180-day timeline for reviewing master account applications, with written justification required for any refusal. No more silent rejections or files stuck for years. This procedural transparency was a key demand from industry players, particularly since the Trump fintech executive order that encouraged greater regulatory clarity.

Implications for the stablecoin ecosystem

The most immediate impact plays out in the stablecoin market, which today weighs $238 billion (TradingView data as of March 18, 2025). Circle, the issuer of USDC, was previously forced to store its reserves at partner commercial banks. With a master account, the company can now hold all of its reserves directly with the Fed.

Concretely, this means every USDC in circulation is backed by a dollar of federal reserves, with no bank counterparty risk. The bank run risk that drove USDC down to $0.88 in March 2023 (when Silicon Valley Bank failed) theoretically becomes impossible. For institutional investors and companies using stablecoins for treasury operations, this is a paradigm shift. This evolution aligns with ongoing discussions about transforming stablecoins into regulatory surveillance tools.

Paxos and Gemini, the two other major regulated issuers in the United States, benefit from the same advantage. There's already a progressive migration underway: since the Fed's announcement, USDT's (Tether, domiciled in the British Virgin Islands with no Fed access) market share has fallen from 68% to 63% in three weeks. Institutional players now favor regulatory certainty.

The other consequence, less visible but equally important, concerns settlement speed. With direct access to Fedwire and FedNow, stablecoin issuers can offer near-instantaneous dollar-to-stablecoin conversions, 24/7. Today, these operations take between 1 and 3 business days when routed through intermediary banks. For companies using stablecoins for international payments, this is a major competitive advantage.

The risks the Fed is monitoring

This opening doesn't mean a free pass. The March 2025 directive introduces strict safeguards, and the Fed maintains tight control over which players it authorizes. The first identified risk is contagion: if a stablecoin issuer with a master account fails, losses could spread to the traditional banking system through payment interconnections.

To prevent this, the Fed imposes strict capital separation. Companies with master accounts must establish a dedicated legal entity with its own capital and governance. Crypto activities (trading, volatile token custody) must remain in separate subsidiaries with no direct access to Fed accounts. This is already the model Coinbase follows with Coinbase Custody Trust Company, its subsidiary regulated as a qualified custodian.

The second risk concerns cybersecurity. A master account provides access to Fedwire, the payment system processing $4 trillion daily. A successful breach could have systemic consequences. The Fed therefore requires quarterly security audits conducted by approved firms, with standards aligned to those of Tier 1 banks (JPMorgan, Bank of America, etc.). Compliance costs are estimated between $5 and $15 million annually for mid-sized players.

Finally, the Fed closely monitors money laundering risk. Stablecoins are used massively for international payments, a fertile ground for illicit flows. Companies with master accounts must implement enhanced KYC/AML systems with automatic suspicious transaction reporting to FinCEN (Financial Crimes Enforcement Network). Some voices in the industry worry these obligations will stifle innovation by making the system as burdensome as traditional banking.

ForYield's take

This regulatory evolution confirms a fundamental trend: the progressive normalization of fintech infrastructure. American regulators are abandoning the defensive posture of 2018-2022 ("we ban on principle") for a more pragmatic approach ("we regulate what works"). Master account access is its most concrete illustration.

For investors, this changes two things. First, counterparty risk on U.S. regulated stablecoins structurally decreases. A portfolio holding USDC through Circle with Fed reserves now presents a risk profile comparable to a traditional money market fund, plus the 24/7 liquidity of crypto markets. That's a solid argument for defensive allocations.

Second, this regulatory clarity opens the door to new products. We're beginning to see yield strategies emerge that combine the safety of Fed-backed stablecoins with yield farming opportunities on audited DeFi protocols. At ForYield, we're integrating these developments into our management strategies: regulated stablecoins are becoming a foundation layer for defensive allocations, while institutional-grade DeFi protocols offer structural yields on these assets.

Vigilance remains warranted. The Fed's criteria will evolve, audits will tighten, and some players won't pass scrutiny. But the direction is clear: American crypto infrastructure is professionalizing, and investors seeking safety and returns now have access to solutions that didn't exist three years ago. This convergence between traditional finance and decentralized protocols is what makes the sector attractive for long-term allocations.

```