Imagine your bank suddenly offering you the chance to buy Bitcoin as easily as Apple stock. Your wealth advisor discussing Ethereum returns with you. The New York Stock Exchange processing token transactions 24 hours a day. This scenario is no longer science fiction—it's 2025, the year when Wall Street and crypto asset adoption becomes reality.

Something fundamental is happening. Traditional financial institutions—the same ones that called Bitcoin "criminal money" five years ago—are now deploying massive infrastructure to integrate crypto-assets into their offerings. BlackRock now manages billions in Bitcoin ETFs. Morgan Stanley is preparing its advisors to discuss staking with clients. The NYSE is developing a crypto trading platform operating continuously.

This wave of institutional crypto adoption represents far more than a simple change of opinion. It's a complete overhaul of the rules of the game. And if you're interested in crypto-assets—whether you're already an investor or simply curious—you need to understand what's really at stake.

The scale of the movement: numbers that speak for themselves

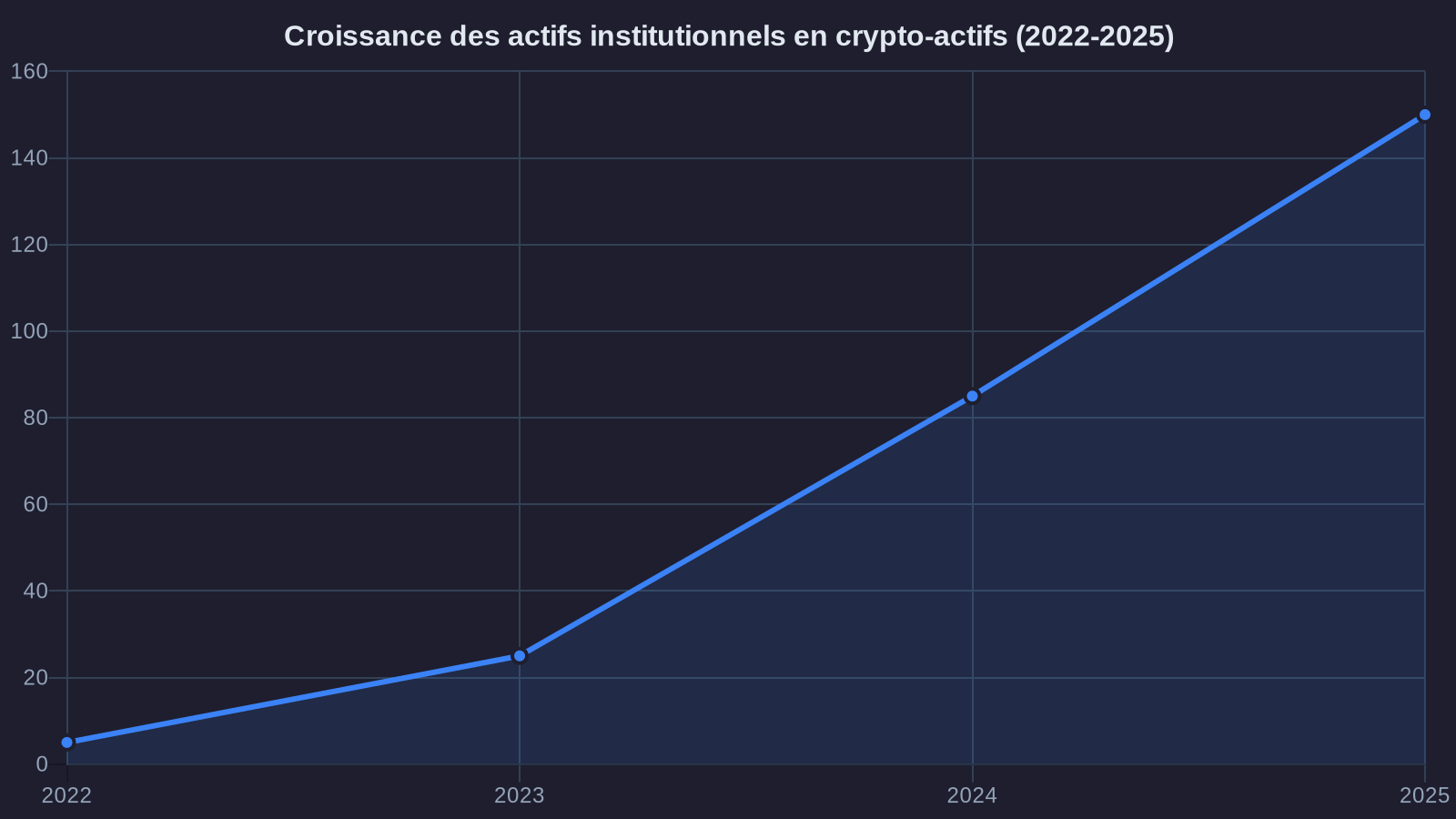

Let's start by setting the stage with some key figures. Institutional assets under management linked to crypto-assets now exceed $150 billion. To put that in perspective: it's more than Hungary's GDP, and it was practically zero three years ago.

BlackRock, the world's largest asset manager with $10 trillion under management, launched its Bitcoin ETF in January 2024. Within months, this fund became one of the fastest-growing ETFs in financial history. Morgan Stanley now allows its 15,000 financial advisors to offer Bitcoin investments to their high-net-worth clients. Goldman Sachs operates a complete trading and custody platform for crypto-assets.

But what makes this movement truly different from previous adoption phases is its systemic nature. These are no longer isolated initiatives led by a few bold banks. It's the entire ecosystem that's shifting: exchanges, custodian banks, asset managers, regulators. Each is building its piece of the Wall Street blockchain infrastructure.

The NYSE, the historic temple of traditional finance, is developing a platform allowing crypto-assets to be traded 24 hours a day, 7 days a week. It's as if the postal service suddenly decided to deliver mail continuously, including weekends. This permanent availability—natural in the crypto world, unthinkable in traditional finance—is gradually becoming the norm expected by investors. In fact, the NYSE is now tokenizing listed stocks, marking a historic turning point in traditional financial infrastructure.

Tokenization: beyond simple trading

But institutional adoption isn't limited to "buying Bitcoin." What truly fascinates Wall Street giants is tokenization. Behind this technical term lies a profound transformation in how we can own and exchange... practically anything.

Imagine your apartment represented by 100 tokens. You could sell 20 tokens (20% of your property) to an investor in Tokyo, 15 to another in Berlin, while keeping 65% for yourself. Transactions would settle instantly, without a notary, without delays, with perfect traceability. Rental income would be automatically distributed each month to token holders, proportional to their share.

This is exactly the model BlackRock is experimenting with through its BUIDL fund (BlackRock USD Institutional Digital Liquidity Fund). Launched in March 2024, this fund tokenizes U.S. Treasury bonds on blockchain. Concretely: you buy a token, and that token represents a share of government bonds. Interest is paid daily, directly to your wallet. No intermediary. No multi-day settlement delays. Instant.

What makes this approach revolutionary is the combination of three elements: liquidity (you can theoretically resell your token at any time), transparency (blockchain records everything), and automation (smart contracts manage distributions). Morgan Stanley is pushing further by now integrating staking strategies into some of its products. Staking is like a savings account: you "lock" your Ethereum tokens to secure the network, and you receive interest in return.

The crucial difference from traditional finance? No need to wait for market opening, no T+2 settlement (two days after the transaction), no cascade of intermediaries each taking their cut. Blockchain enables near-instant settlement, 24/7, with drastic reduction in friction costs. These tokenized securities are radically transforming access to financial assets, as evidenced by the integration of real-world assets into DeFi protocols.

What this means for individual investors

You might be wondering: "Okay, but what does this actually change for me?" Several major shifts are already underway.

Accessibility is improving dramatically. You no longer need to understand the difference between a private and public key, manage a complex wallet, or navigate through opaque exchange platforms. Your regular broker—the one you already buy stocks from—is beginning to offer crypto-assets with the same simplicity. Morgan Stanley, Fidelity, Charles Schwab: all are developing familiar interfaces to access this universe once reserved for insiders.

Security and regulation are strengthening. Traditional financial institutions bring with them decades of experience in risk management, regulatory compliance, and investor protection. BlackRock won't launch a product without subjecting it to extensive controls. This doesn't mean risk disappears—crypto-assets remain volatile—but the risk of pure fraud, of a platform vanishing with your funds, diminishes considerably when you go through a regulated player.

Products are diversifying and becoming more sophisticated. Beyond simply "buying Bitcoin," you're progressively gaining access to more elaborate strategies: crypto index funds, yield-generating products via staking, exposure to diversified token baskets, even structured products combining traditional and crypto assets. This sophistication is a double-edged sword: more choice, but also more complexity to understand.

However, this institutionalization also carries less obvious implications. By making crypto-assets "easy," we risk forgetting certain fundamentals. Bitcoin was designed as a decentralized system, without intermediaries. When you buy a Bitcoin ETF through your broker, you don't actually own Bitcoin—you own a share of a fund that owns Bitcoin. Important distinction: you can't use this asset as currency, you don't control your private keys. It's indirect ownership, like owning shares in a mining company rather than physical gold.

Questions you should ask yourself

Facing this wave of institutional crypto adoption, several questions merit reflection before diving in.

What is your real motivation? If you're interested in crypto-assets to diversify your portfolio with moderate exposure, institutional products (ETFs, funds) are probably suitable. If you want to explore decentralized philosophy, experiment with DeFi (decentralized finance), or simply control your assets directly, then going through Wall Street moves you away from that objective.

Do you truly understand what you're buying? A Bitcoin ETF is not Bitcoin. A tokenized fund with integrated staking combines multiple layers of complexity. Before investing, make sure you understand: where are underlying assets held? Who keeps them? What are the fees? What specific risks (counterparty risk, smart contract risk, liquidity risk) are you assuming?

What time horizon are you considering? Institutional entry brings liquidity and probably some long-term stabilization. But short-term, crypto-assets remain volatile. The institutional investors themselves often reason over horizons of several years. If you're looking for quick gains, you risk being disappointed—or worse, panic-selling during a correction.

Finally, a fundamental question: what portion of your wealth should you allocate to this asset class? Institutional advisors generally recommend between 1% and 5% for a standard investor. This caution reflects asset volatility, but also residual regulatory uncertainty and technological risks. Some more aggressive investors go to 10-15%, but this implies high risk tolerance. For those considering a longer-term strategy, the tax implications of crypto-assets in retirement also deserve careful attention.

Toward a hybrid finance powered by Wall Street blockchain

Wall Street's massive adoption of crypto-assets is shaping the contours of a hybrid finance. On one side, traditional institutions bring their expertise in risk management, access to liquidity, their proven infrastructure. On the other, blockchain technology offers transparency, operational efficiency, and new possibilities (tokenization, smart contracts, instant settlement).

This convergence doesn't eliminate tensions. Crypto purists blame institutions for betraying the original decentralized spirit. Regulators worry about systemic risks if these assets become too intertwined with traditional finance. Investors question the right balance between innovation and prudence.

But one thing is certain: we won't go back. The $150 billion in institutional assets won't disappear. The 24/7 platforms won't revert to standard trading hours. Tokenization won't stop at Treasury bonds—it will progressively expand to real estate, artwork, carbon credits, to countless assets today difficult to fractionalize or exchange.

For you as an individual investor, this transformation means both more opportunities and more responsibilities. More opportunities because access simplifies, products diversify, costs fall. More responsibilities because you must understand what you're truly buying, distinguish marketing from reality, and clearly define your investment objectives.

Wall Street didn't "adopt" crypto out of ideological enthusiasm. It did so because clients demand it, because technology demonstrates its utility, and because business opportunities are considerable. This pragmatic transformation is perhaps less romantic than the original vision of Bitcoin pioneers. But it makes crypto-assets accessible to millions who otherwise would never have engaged with them.

The question is no longer whether this Wall Street and crypto assets 2025 adoption will happen—it's already underway. The real question is: how will you position yourself in this new reality? With prudence and discernment, the opportunity is there. Without preparation or understanding, it's an unnecessary risk. The choice is yours.