For years, the question was straightforward: could stablecoins legally offer returns to their holders? The answer from U.S. regulators was equally clear: no. Or rather, maybe, but wrapped in legal ambiguity that deterred most serious players.

The Crypto Market Structure Bill, taking shape for likely adoption in 2026, changes everything. Emerging compromises are opening the door to yield-bearing stablecoins—dollar-pegged tokens that distribute a portion of the interest generated by their reserves. But this authorization comes with strict guardrails that redefine the rules for all of DeFi.

To understand what's at stake, you first need to grasp why this question has crystallized so much tension between crypto innovation and traditional financial regulation.

The core issue: when does a stablecoin become a security?

Imagine depositing 100 euros into a digital vault. In exchange, you receive a token representing those 100 euros. As long as that token's worth exactly 100 euros and generates no returns, regulators sleep soundly. It's simply a payment mechanism.

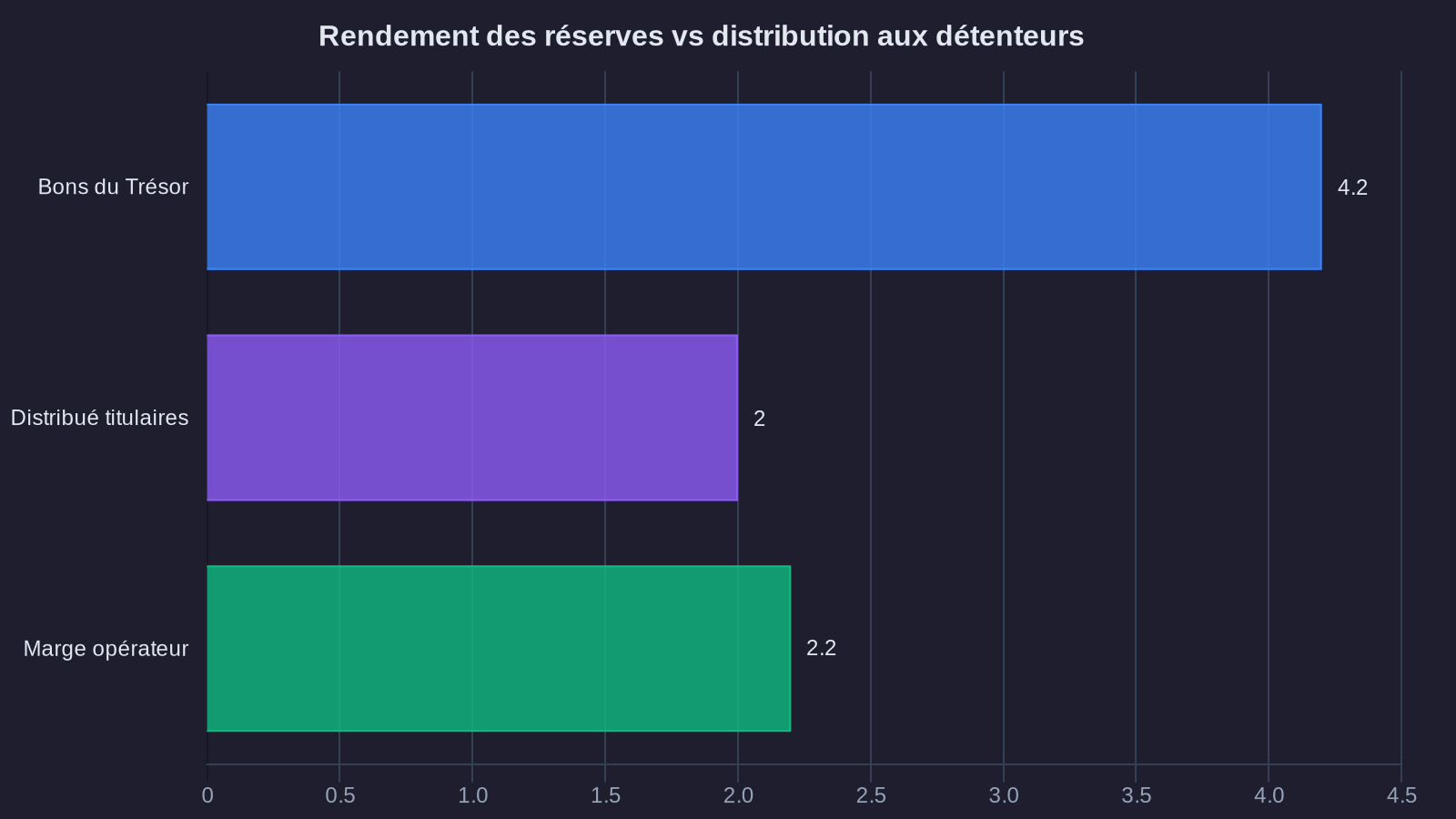

Now imagine the vault manager places your 100 euros into Treasury bonds earning 4% annually and passes 2% of that return to you. Your token still trades at 100 euros, but it generates interest. For the SEC (the U.S. financial markets regulator), you've just crossed a red line: that token now looks like a security, complete with all the regulatory obligations that entails.

This is precisely the dilemma that's stalled yield-bearing stablecoin development in the United States. Projects like Mountain Protocol or Ondo Finance have had to navigate murky legal waters, sometimes by excluding U.S. investors, sometimes by adopting complex legal structures.

The debate isn't just about legal nuance. It cuts to the heart of what makes DeFi attractive: the ability to put your assets to work without intermediaries, transparently and accessibly. If holding a stablecoin becomes as burdensome as owning a listed stock, much of the promise evaporates.

The compromises emerging from the Crypto Market Structure Bill

Draft versions of the bill, debated between Republicans and Democrats in Congress, sketch out a framework attempting to balance innovation with investor protection. Three pillars are emerging.

First pillar: a clear distinction between payment stablecoins and investment stablecoins. A stablecoin distributing no returns to holders remains a payment instrument, subject to lighter-touch rules. It simply needs to maintain its dollar peg and prove it holds sufficient reserves (cash, short-term Treasury securities). This is where USDC and USDT fit today.

The moment a stablecoin starts redistributing interest generated by its reserves, it shifts into a hybrid category. Not quite a traditional security, but no longer a simple payment mechanism either.

Second pillar: strengthened transparency requirements. Yield-bearing stablecoin issuers must publish the exact composition of their reserves, with monthly audits conducted by independent firms. They must also detail their return distribution policy: what percentage of interest the issuer retains, what percentage flows to users, and under what terms.

This transparency is designed to prevent the drift seen with some projects that promised high yields without explaining where the money came from. Remember the collapse of Anchor Protocol and its UST stablecoin, which offered 20% annual returns funded by... nothing tangible.

Third pillar: a cap on distributable yields. This is probably the most contentious point. Current compromises suggest that returns paid to holders couldn't significantly exceed short-term U.S. Treasury rates. The goal is to prevent promises of outsized yields from luring unsophisticated investors into risky products masquerading as stablecoins.

Concretely, if 3-month T-Bills yield 4.5%, a yield-bearing stablecoin could distribute between 3% and 4% to users, with the issuer keeping the remainder for operating costs and margins. Nothing revolutionary, but enough to create a credible alternative to traditional savings accounts.

How stablecoin regulation changes the game for DeFi investors

This nascent regulation isn't just about compliance checkboxes. It's reshaping the landscape of strategies available in decentralized finance.

For retail investors, access to stable, transparent yields becomes safer. Until now, earning returns on stablecoins often meant using lending protocols or liquidity mining, mechanisms that remained opaque for many. With regulated yield-bearing stablecoins, you get a simpler solution: just hold the token, no complex maneuvering, no unaudited smart contract risk.

It's a bit like the difference between putting money in a savings account (simple, regulated, guaranteed return) and structuring products (potentially higher returns, but with risks few people truly understand).

For established DeFi protocols, competition intensifies. Platforms like Aave or Compound, which let you lend stablecoins for compensation, will need to contend with a new competitive force. Why take smart contract risk if you can earn 3.5% simply by holding a yield-bearing stablecoin in your wallet?

The answer likely hinges on yield differentials. If Aave continues offering 6–8% on USDC during high-demand periods, the added risk remains justified for sophisticated users. But the baseline "risk-free" return (or low-risk return) mechanically rises, compressing margins throughout the value chain.

For stablecoin issuers, the business model evolves. Circle, the USDC issuer, currently generates most revenue by placing user reserves into safe instruments and keeping all the interest. Under new regulation, it'll need to redistribute some of that interest to stay competitive against new entrants offering yield-bearing stablecoins from day one.

We're already seeing this shift. Circle has announced testing a yield-bearing USDC version in certain jurisdictions, anticipating U.S. regulation. Tether, meanwhile, remains quieter but would struggle to ignore this trend if regulation mandates it. This evolution echoes questions about stablecoin centralization and their impact on DeFi strategies.

Gray zones persisting in yield compliance

Despite progress, several questions linger. The main one concerns how this U.S. regulation articulates with frameworks finalizing elsewhere, notably in Europe with the MiCA regulation (Markets in Crypto-Assets).

MiCA takes a different approach: it implicitly allows yield-bearing stablecoins but imposes capital and governance requirements that could prove more restrictive than the U.S. framework. An issuer operating on both sides of the Atlantic must navigate two distinct regimes, complicating standardization.

Another gray zone: what happens to algorithmic stablecoins generating yield without relying on fiat reserves? Projects like Frax or Ethena propose hybrid mechanisms, partially collateralized, where yields come from carry trades or arbitrage rather than simple Treasury interest. The bill doesn't appear to have clearly settled their status.

Finally, it remains unclear how regulators will treat decentralized protocols issuing stablecoins without a central legal entity. MakerDAO, which issues DAI, operates through distributed governance. Who bears compliance responsibility? Early developers? Governance token holders? This question extends beyond yield-bearing stablecoins, but becomes critical once reporting and audit obligations enter the picture.

Toward normalized yields in DeFi?

What's taking shape with the Crypto Market Structure Bill isn't revolutionary—it's normalization. Yield-bearing stablecoins will likely become a standard product, much like money market funds in traditional finance: capital-protected, liquid investments offering modest but predictable returns.

For investors who came to DeFi seeking double-digit returns risk-free, it's disappointing. That era, fueled by protocol subsidies and artificial incentives, is ending. What remains is an alternative financial infrastructure, more transparent and accessible than the traditional banking system, yet subject to the same fundamental constraints: there's no high return without high risk.

The real question for 2026 and beyond is whether this regulation enables a mature DeFi ecosystem where returns reflect genuine economic activity (collateralized lending, liquidity provision in active markets), or whether it stifles innovation by imposing barriers to entry that are too high.

Signals are mixed. On one hand, regulatory clarity should attract institutional players long hesitant to participate, as shown by growing institutional adoption of stablecoins, with rising volumes and liquidity. On the other, the most innovative protocols might continue developing outside the U.S., in more permissive jurisdictions, creating market fragmentation.

What's certain is that DeFi's landscape in 2026 will look vastly different from 2021. Regulated yield-bearing stablecoins will be central to it, but their success depends on delivering a simple user experience while meeting complex regulatory demands. A delicate balance that will define the sector's next phase of maturity.