An unusual phenomenon is currently sweeping through crypto markets: tokens issued during private fundraising rounds are trading on secondary platforms at discounts reaching 90% compared to their initial valuations. Projects valued at several billion dollars during their funding rounds see their tokens exchanged for a fraction of their issuance price.

This situation raises eyebrows. One might see a massive arbitrage opportunity here, a chance to buy into projects backed by prestigious funds at a steep discount. The reality is considerably more nuanced, and understanding the mechanisms at play becomes essential for anyone considering positioning themselves on these assets of the crypto secondary market.

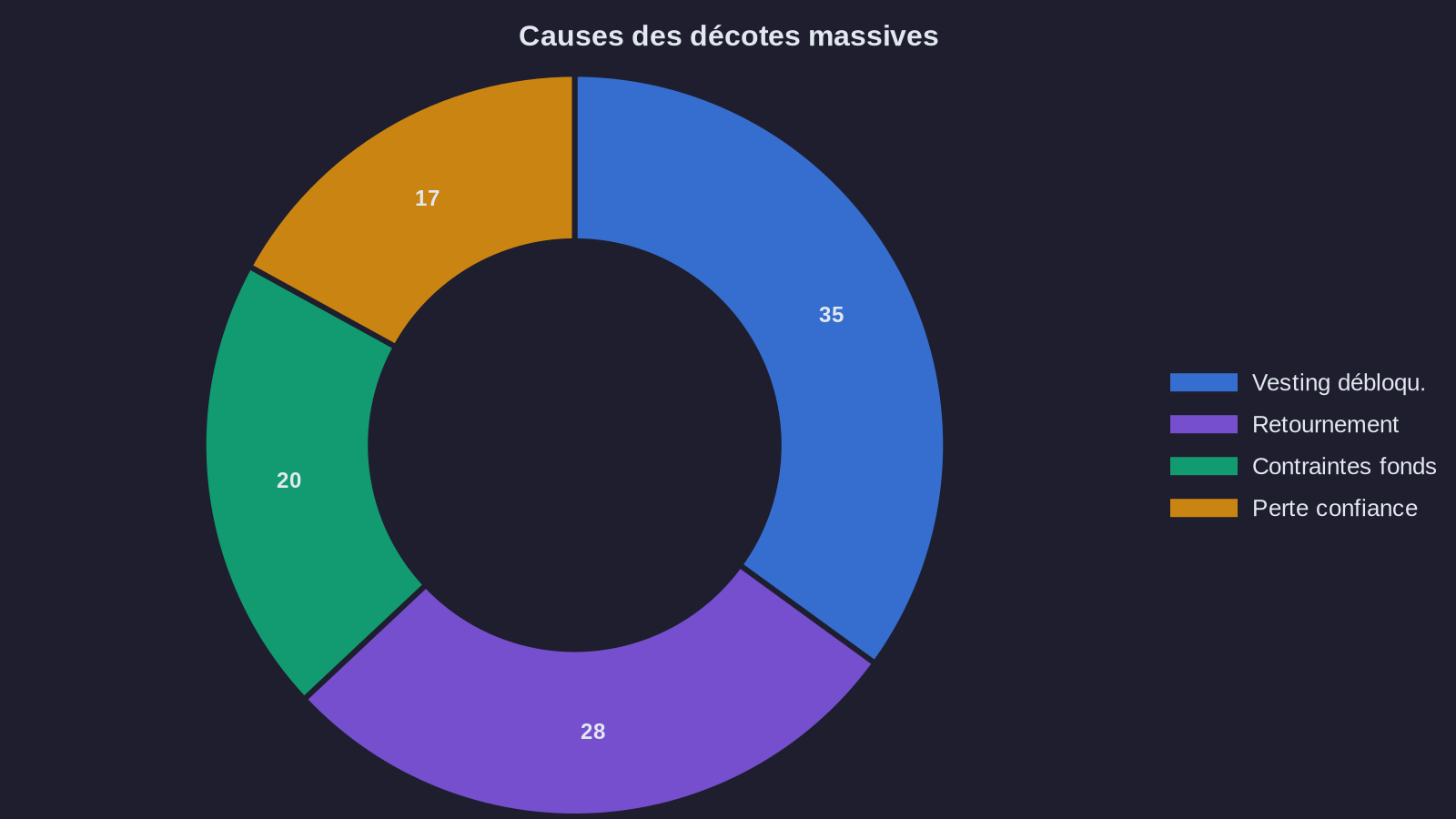

The anatomy of a discount: how do we get to 90% discounts on secondary market tokens?

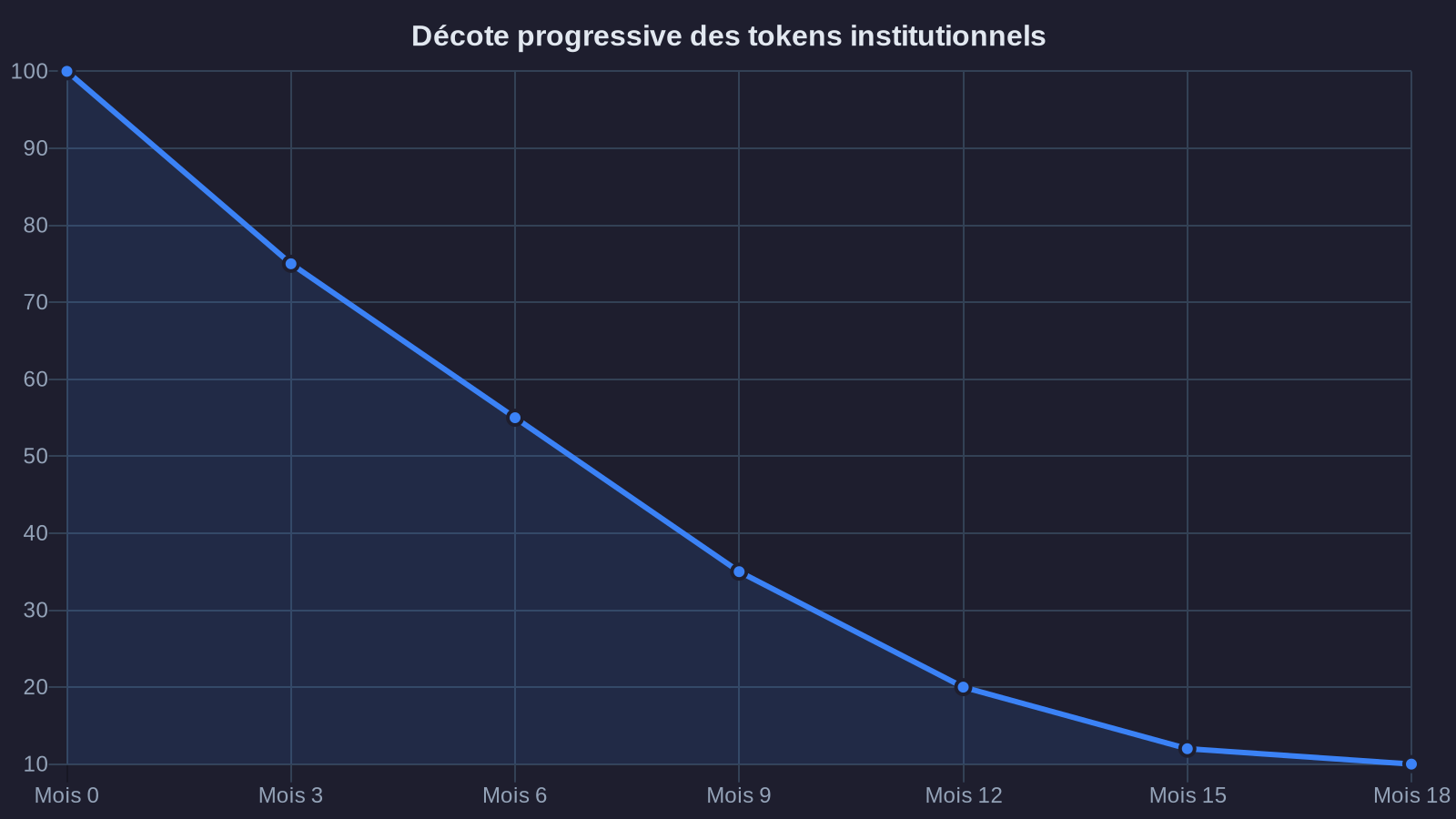

To grasp the scale of the phenomenon, we must first understand the typical lifecycle of an institutional token. A project raises funds from qualified investors during private rounds (seed, Series A, Series B), often with aggressive valuations driven by market euphoria. These tokens come with vesting periods: investors cannot resell them immediately, but gradually over several years.

The problem emerges when the market turns. Institutional investors who participated in these rounds find themselves locked in with illiquid positions acquired at valuations that are now unrealistic. Some funds, subject to liquidity constraints or investor redemptions, seek to exit before their tokens fully unlock.

This is where secondary market platforms like Securitize, tZERO, or specialized OTC brokers come in. These actors facilitate over-the-counter transactions between pressured sellers and opportunistic buyers. The imbalance between supply and demand, coupled with the absence of public liquidity, creates conditions ripe for spectacular discounts.

Let's take a concrete example: a fund participated in a funding round valuing a project at 10 billion dollars, acquiring tokens at 5 dollars each. Eighteen months later, the crypto market has crashed 70%, and the project hasn't yet launched its mainnet. The fund, facing redemption requests from its own investors, needs to raise cash. It offers its tokens at 0.50 dollars on the secondary market, a 90% discount.

The hidden risks behind the valuation arbitrage opportunity

Faced with such a discount, the temptation to position oneself is strong. After all, these projects have convinced reputable funds, possess substantial treasuries, and work with experienced teams. The reasoning seems rational: if the project succeeds, the potential for appreciation is enormous.

Several factors temper this optimism. First, the initial valuation itself is questionable. In an exuberant bull market, crypto funding rounds regularly reach multiples disconnected from any fundamentals. A pre-product project valued at several billion dollars reflects more the speculative appetite of the moment than a rigorous evaluation of economic potential.

The 90% discount could therefore simply bring the price back to a more realistic valuation, or even still overvalued. We observe this phenomenon in other sectors: think of the valuations of tech unicorns in 2021, followed by massive corrections in 2022-2023. The crypto secondary market often anticipates these readjustments.

Furthermore, ownership concentration poses a major structural risk. Tokens held by a handful of institutional investors create a permanent sword of Damocles. When vesting periods reach their end, these actors can dump considerable volumes onto the market, crushing the price. This "unlock" risk is systematically underestimated by secondary market buyers.

We see this mechanism recur consistently: a token trades at a low price for months on the secondary market, then drops another 50 to 80% upon public listing, overwhelmed by selling pressure from initial investors seeking to exit. The secondary discount provides absolutely no protection against this risk.

The illiquidity trap

Acquiring tokens on the secondary market often means accepting the same vesting constraints as the sellers. You're not buying an asset free from restrictions, but a position subject to a progressive unlock schedule. In other words, you're taking on valuation risk without enjoying liquidity.

This situation creates an asymmetric gap: the seller obtains immediate liquidity (albeit with a discount), while the buyer inherits the illiquidity. If the project disappoints or the market deteriorates further, the buyer becomes trapped with no rapid exit opportunity. The secondary market itself becomes illiquid for these "discount" positions, creating a double-penalty effect.

Implications for DeFi yield strategies

For investors structuring yield strategies on crypto-assets, these secondary market opportunities raise specific questions. The massive discount may seem attractive from a diversification or strategic participation angle. But integrating these positions into a portfolio requires particular rigor, especially against the backdrop of emerging yield alternatives in DeFi.

First, valuation itself becomes problematic. How do you mark these assets in your book? At what price: that of the last funding round, that of the secondary market, an internal valuation? The gaps can reach considerable multiplication factors. This valuation uncertainty complicates risk management and communication with investors.

Next, correlation with the broader market remains high. These tokens, however discounted, typically follow Bitcoin and Ethereum movements. When the crypto market plunges, these positions suffer the same pressure, or even amplified by their lower liquidity. The hope for decorrelation thanks to the initial discount often proves illusory.

Certain strategies can nevertheless benefit from these anomalies, but with strict safeguards. You might consider positions of limited size (1 to 3% of a diversified portfolio), in projects whose technical fundamentals and development progress are verifiable. The focus should be on the project's capacity to generate real economic value, not solely on the discount relative to perhaps fanciful valuation.

The role of on-chain data in analyzing crypto token pricing inefficiency

A rigorous approach incorporates on-chain metrics analysis when the project already has an active network. Transaction volume, growth in unique addresses, developer activity, locking in DeFi protocols: these indicators provide concrete vision of real adoption, beyond pitch deck promises.

For pre-launch projects, analysis focuses on development milestones: adherence to technical schedules, code quality (audits, GitHub activity), operationally functional partnerships versus mere announcements. This due diligence becomes all the more critical because the discount can mask warning signals that institutional investors have detected.

Toward maturation of the crypto secondary market

This phenomenon of massive discounts reflects a phase of transition in the crypto market. We're gradually moving from an ecosystem dominated by pure speculation to an environment where valuations face demands for tangible value creation. Institutional investors who overpaid during the euphoria are today digesting their allocation mistakes, as illustrated by the evolution of crypto positions among traditional financial actors.

This correction creates temporary distortions, some of which genuinely represent opportunities. But opportunity rarely lies in blindly buying everything displaying a large discount. It's found in the meticulous identification of projects whose fundamentals justify future appreciation, regardless of the price paid in previous rounds.

Secondary market platforms themselves are evolving toward greater transparency and structure. We're seeing the emergence of reporting standards, more sophisticated price discovery mechanisms, and professionalization of intermediaries. This maturation should progressively reduce the most egregious valuation gaps, while maintaining a legitimate illiquidity premium.

For actors building diversified yield strategies on crypto-assets, the secondary market represents a complementary source of exposure, provided you accept its specific constraints. Investment horizon must extend to several years, position size remain contained, and selection rest on rigorous fundamental analysis rather than on the sole appeal of the displayed discount. Entry price never guarantees investment success: the quality of the underlying asset makes the difference over time.