In March 2025, a fault line runs through the cryptocurrency derivatives industry. On one side, the Chicago Mercantile Exchange (CME) and the Intercontinental Exchange (ICE), historic giants of regulated markets, mobilizing their lobbying teams to challenge the legality of onchain perpetual futures before the CFTC. On the other, Hyperliquid, a decentralized protocol that allows trading these same onchain perpetual contracts without a centralized intermediary. What's at stake here goes far beyond a technical or legal dispute: it's the question of who will control the infrastructure of tomorrow's financial markets.

The paradox is striking. Trading volumes on onchain perpetual swaps now reach tens of billions of dollars daily. These instruments, which allow taking positions on an asset without an expiration date, have become the flagship product of crypto finance. Yet their regulatory status remains unclear, even contested. And it's precisely this gray zone that traditional players are trying to exploit to slow down competition that bothers them.

The Hyperliquid model: decentralized derivatives without intermediaries

Hyperliquid operates according to an architecture radically different from traditional exchanges. On this protocol launched in 2023, perpetual contracts execute directly onchain via audited smart contracts. Users retain custody of their funds in their own wallet. The order book is managed in a decentralized manner. There is no central entity that can freeze accounts, change the rules mid-game, or go bankrupt taking customer deposits with it.

This approach addresses a concrete need. After FTX's collapse in November 2022, which wiped out $8 billion in customer funds, the question of asset custody became central. Institutional traders and family offices were seeking solutions that allowed them to take positions in crypto-assets without surrendering control of their funds to a third party. Hyperliquid offers precisely that: sophisticated trading tools with minimal counterparty risk exposure.

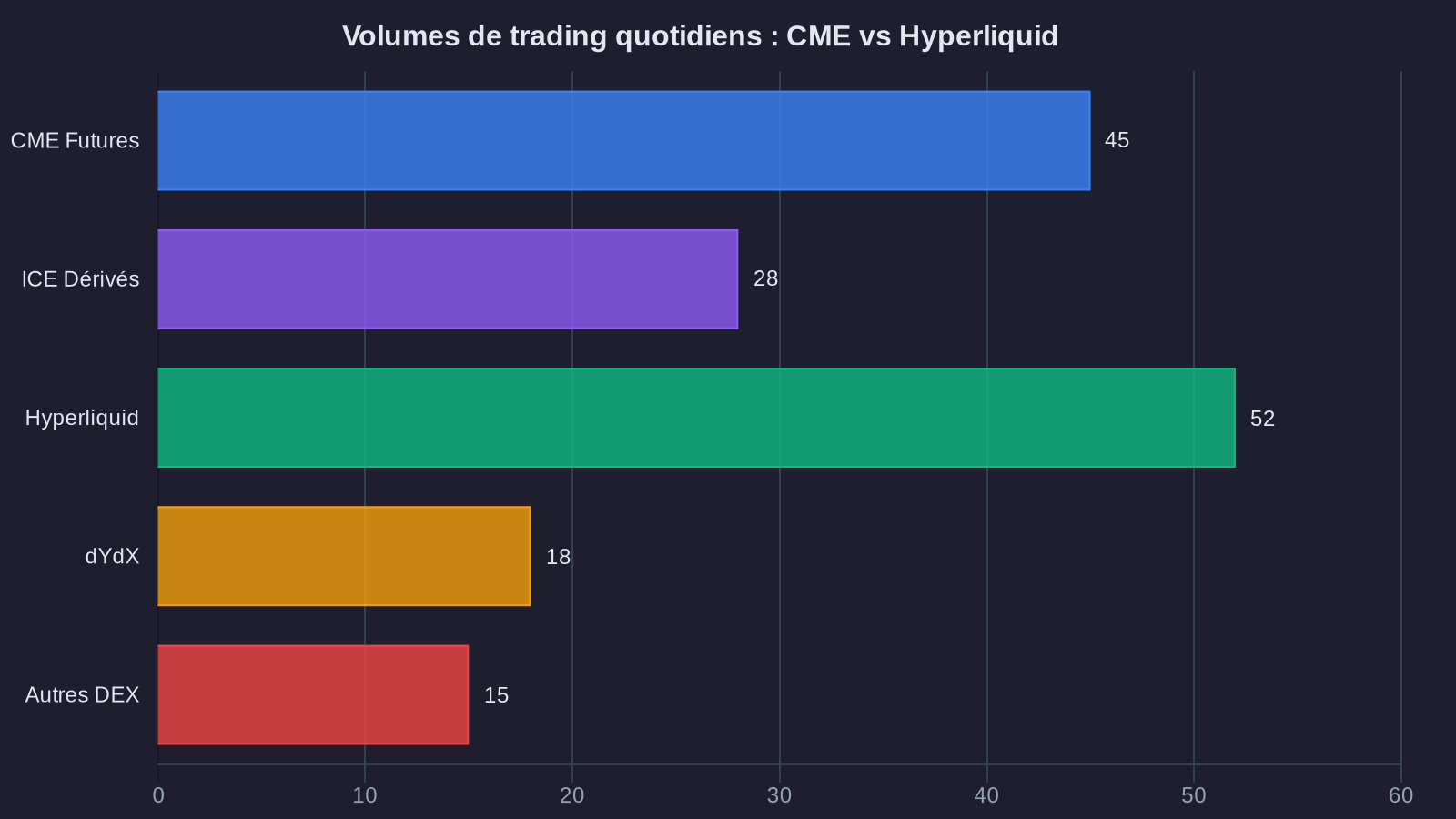

The protocol now boasts a TVL (Total Value Locked) exceeding one billion dollars and daily volumes comparable to some established centralized platforms. Trading fees are competitive, latency acceptable for most strategies, and user experience is improving rapidly. For a growing portion of the market, the decentralized option is no longer a technical compromise but an assumed strategic choice, as evidenced by certain innovative governance structures in the DeFi ecosystem.

The CME's regulatory counteroffensive via the CFTC

Faced with this surge in power, traditional exchanges aren't sitting idle. The CME has invested tens of millions in its crypto infrastructure in recent years. Its regulated Bitcoin and Ethereum futures contracts attract institutions that cannot, for compliance reasons, engage with decentralized protocols. But these volumes remain modest compared to overall crypto market activity. And above all, the business model relies on clearing, custody, and settlement fees that justify the existence of multiple intermediaries.

Hyperliquid and similar protocols challenge this model. They offer infrastructure where these intermediaries become unnecessary. The CME and ICE's response therefore operates on the regulatory front. Their legal arguments center on several axes: perpetual swaps are derivative contracts that should only be traded on platforms registered with the CFTC (Commodity Futures Trading Commission). Decentralized protocols cannot guarantee the investor protection standards, market surveillance, and anti-money laundering prevention required by regulators.

These arguments aren't without merit. The CFTC does indeed have authority over commodity derivatives markets in the United States, a category into which Bitcoin and Ethereum have been classified. The question is whether this authority extends to decentralized protocols, which by nature aren't operated by an identifiable legal entity. This is the core ambiguity: how do you regulate open source software deployed on a public blockchain, with no CEO, no headquarters, no employees in the traditional sense?

The CME's behind-the-scenes lobbying

CME representatives are multiplying meetings with members of Congress and CFTC staff. Their message is clear: decentralized derivatives protocols create systemic risks. They allow excessive leverage without adequate protective mechanisms. They escape reporting obligations that enable detection of market manipulation. And crucially, they operate from opaque jurisdictions, complicating any action if problems arise.

These concerns resonate with some regulators. Rostin Behnam, chairman of the CFTC, has repeatedly stated that crypto derivatives markets must be subject to the same standards as traditional markets. The problem is that these standards were designed for a centralized world, with clearinghouses and regulated intermediaries. Applying them as-is to decentralized protocols amounts to de facto banning them.

Hyperliquid's defense: technical transparency and decentralization

Hyperliquid doesn't have the same lobbying resources as the CME. But the protocol benefits from an active community and solid technical positioning. Its defenders advance several counterarguments. First, onchain transparency offers a level of traceability that traditional systems cannot match. Every order, every liquidation, every movement of funds is recorded publicly on the blockchain. Anyone can audit the protocol's operation in real time, without depending on an operator's goodwill.

Second, risk management mechanisms are codified in smart contracts. Collateral ratios, liquidation procedures, leverage parameters cannot be arbitrarily changed by management or a board of directors. They require a public governance vote, with a delay that allows the community to react. This rigidity may seem constraining, but it eliminates the risk of discretionary interference that caused the collapse of several centralized platforms.

Finally, the central regulatory argument: Hyperliquid doesn't control user funds. There is no deposit, no custody, no transfer of ownership to an intermediary entity. Users interact directly with a software protocol. From this perspective, banning Hyperliquid would amount to banning the use of calculation software on the grounds that some might use it to circumvent regulations. This is a legally fragile position that raises questions about freedom of expression and technological neutrality.

Unexpected allies

This battle attracts varied supporters. Digital rights advocacy groups who see in this case a test of American law's ability to adapt to decentralized technologies. Libertarian think tanks, for whom onchain protocols represent a natural limit to state regulatory power. But also traditional financial actors who perceive in this architecture an opportunity to reduce operational costs and improve capital efficiency.

Some family offices and hedge funds are beginning quietly to allocate part of their positions to protocols like Hyperliquid, attracted by the possibility of trading 24/7 without depending on a prime brokerage infrastructure. These actors aren't ideologically attached to decentralization. They're making a purely pragmatic calculation: as long as technical risks are manageable and the regulatory framework isn't definitively clarified, the decentralized option offers a competitive advantage.

What future for onchain perps regulation?

This battle is playing out on several fronts simultaneously. In the United States, Congress is debating a legislative framework for digital assets that could clarify the status of decentralized protocols. The outcome will depend largely on the balance of political power and stakeholders' ability to make their case. In Europe, MiCA regulation provides a first layer of oversight, but leaves aside the specific question of decentralized derivatives. In Singapore, Hong Kong, and Dubai, regulators are testing more pragmatic approaches that attempt to frame activity without killing innovation.

The reality is that this question will probably not be resolved by a binary answer. A hybrid model is emerging where some protocols choose to partially register with regulators by creating legal entities that operate a user interface or support service, while leaving the underlying protocol decentralized. Others, like Hyperliquid, maintain a more radical position of technical neutrality, arguing that the code is free, open source, and that its deployment falls under no particular jurisdiction.

What's certain is that volumes won't disappear. Users who've discovered the ability to trade without intermediaries, maintaining custody of their assets, won't broadly return to centralized models. Institutions that have integrated these protocols into their tech stack won't tear everything down at the first ambiguous regulatory signal. The market adapts, circumvents, innovates. Attempts at regulation through outright bans have always failed against naturally distributed technologies.

The CME and ICE understand this well. Their strategy probably isn't to make decentralized protocols disappear, but to obtain a regulatory framework that confines them to marginal status, reserved for users willing to accept a legal gray zone. This would protect the core of their business model while allowing an alternative segment to exist for early adopters and unregulated actors. It's a containment strategy, not one of eradication.

Hyperliquid and similar protocols play their part in mirror: demonstrating through use that their model works, that it's resilient, that it attracts significant volumes, and that it meets a need traditional infrastructure cannot satisfy. The more these protocols prove their technical robustness and economic relevance, the harder it becomes for regulators to ignore them or treat them as a temporary anomaly. The debate then shifts from the permitted/forbidden terrain toward how to frame a reality that's imposing itself.

This regulatory battle around Hyperliquid is just one episode of a larger transformation. Financial markets are reinventing themselves, decentralizing, dematerializing. Historic players are trying to slow this evolution to preserve their positions. New entrants are pushing to accelerate the transition. Between them, regulators are seeking a balance that protects investors without stifling innovation. The outcome of this equation will determine what finance looks like over the next decade.