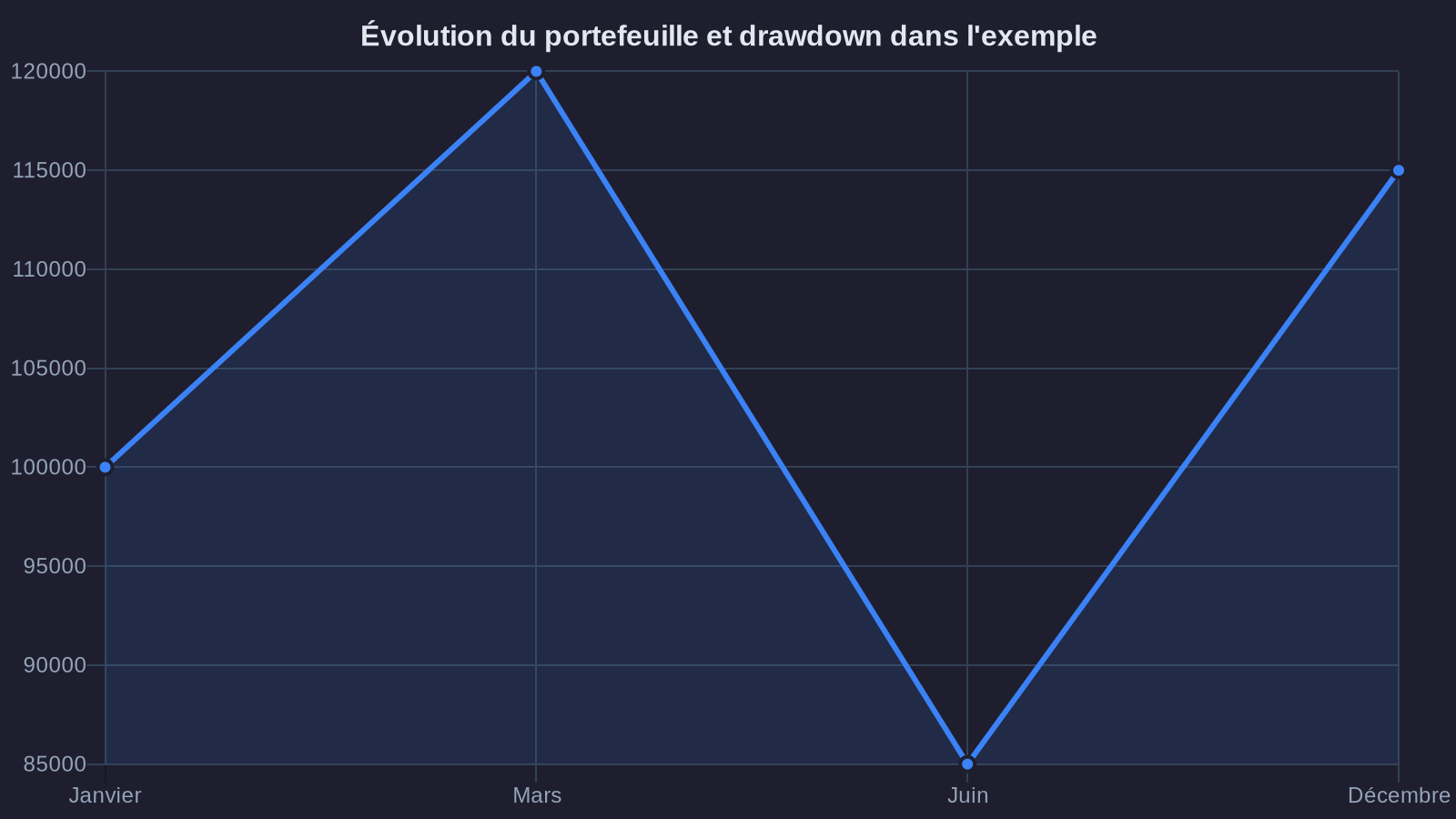

Imagine you invest €100,000 in a crypto portfolio in January. By March, your capital reaches €120,000. Excellent. Then comes a sharp correction: by June, you're down to €85,000. By December, you finish the year at €115,000. Annual return: +15%. An attractive result on paper.

Yet a crucial detail is missing from this summary: between March and June, you lost 29% of your capital from its peak. This drop is your drawdown. And it's precisely this risk management metric that most investors overlook, until their portfolio hits its first storm.

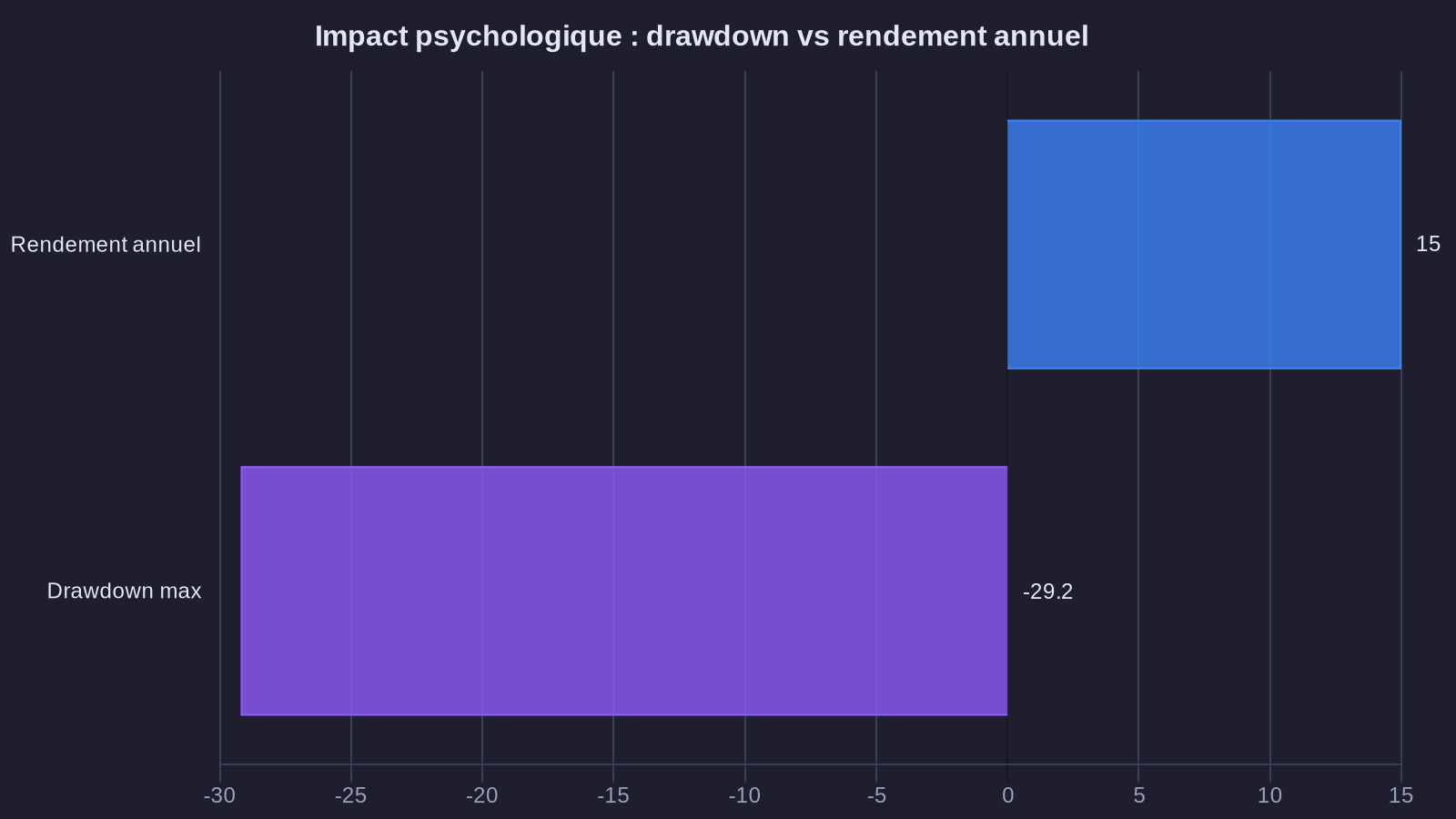

Drawdown measures the maximum loss suffered since your portfolio last peaked. If your capital drops from €120,000 to €85,000, your drawdown is 29.2%. This metric doesn't just tell you how much you lost. It reveals something far more fundamental: your actual ability to hold your positions during a crisis.

Because here's a reality that 15 years of wealth management consulting have taught me: it's not returns that make investors abandon ship. It's unanticipated drawdowns, psychologically unbearable losses, sleepless nights watching your portfolio shrink.

Why maximum drawdown matters more than annual return

Average annual returns tell an incomplete story. Let's look at two portfolios over three years:

Portfolio A:

- Year 1: +30%

- Year 2: -25%

- Year 3: +35%

- Average annual return: +13.3%

- Maximum drawdown: -25%

Portfolio B:

- Year 1: +18%

- Year 2: +12%

- Year 3: +15%

- Average annual return: +15%

- Maximum drawdown: -8%

Portfolio B shows slightly higher returns. But more importantly, it exposes you to far lower volatility. For a €100,000 investor, this means your capital never dips below €92,000, versus €75,000 in the first case. This difference is anything but trivial.

Because after a 25% decline, you need a 33% bounce-back to recover your initial capital. After a 50% crash — common in crypto — you need to double your money. The mathematics of losses are ruthless. The more you lose, the harder it becomes to get back to square one.

This is where real wealth management happens: in your ability to limit drawdowns, not just maximize returns. An investor who endures a 60% drawdown often ends up selling at the bottom, out of panic or necessity. Even if the market recovers later, they're no longer there to benefit.

Crypto vs stocks: two worlds, two levels of drawdowns

Let's compare historical drawdowns between traditional assets and crypto-assets. The numbers speak for themselves.

Stocks (S&P 500):

- Average maximum drawdown over 10 years: -15% to -20%

- Major crises (2008, 2020): -50% to -57%

- Average recovery time after crisis: 18 to 24 months

Bitcoin:

- Average maximum drawdown per cycle: -70% to -85%

- Example: November 2021 ($69,000) to November 2022 ($15,500) = -77%

- Recovery time: 24 to 36 months on average

Altcoins (outside top 10):

- Frequent drawdowns of -85% to -95%

- Many projects never reach their all-time highs again

These gaps reflect a fundamental difference in maturity. Stocks benefit from real fundamentals (revenues, profits, dividends) that cushion shocks. Crypto-assets remain largely governed by speculation, progressive adoption, and macro-economic liquidity cycles.

Concretely, for an investor who puts €50,000 into Bitcoin in November 2021, it means watching your capital drop to €11,500 by November 2022. Even with unshaken conviction, few portfolios can withstand such erosion without flinching. It's human nature.

The question isn't whether Bitcoin will rebound — it always has so far. The question is: can you psychologically and financially endure 18 months at -70%?

Building a crypto portfolio resilient to drawdowns

Accepting that you can't eliminate drawdowns is already a form of investor maturity. However, you can anticipate them, limit them, and most importantly, ensure they remain bearable.

First rule: define your personal pain threshold. Ask yourself this before investing: what maximum decline am I willing to accept without panicking or liquidating positions? If the answer is -20%, a portfolio that's 100% Bitcoin or altcoins isn't for you. If the answer is -50%, you can consider significant crypto exposure, but never exclusively.

Second lever: diversification across asset classes. A balanced portfolio split between stocks (60%), bonds or yield-bearing stablecoins (30%), and crypto-assets (10%) historically shows far lower drawdowns than a 100% crypto portfolio. In 2022, while Bitcoin plummeted 65%, such a portfolio would have limited its overall loss to around -25%. Still painful, but manageable.

Third approach: systematic rebalancing. Setting a target allocation (say 10% in crypto) and restoring it quarterly lets you mechanically sell after gains and buy after losses. This risk management discipline constrains drawdowns and forces you to take profits during upswings, when euphoria typically pushes us to overweight risky assets.

Fourth strategy, more advanced: dynamic stop-loss or volatility-based management. Some investors automatically reduce crypto exposure once historical volatility exceeds a defined threshold (for instance, 60% annualized). It demands active monitoring, but it can prevent the worst drawdown phases.

Finally, and this point is rarely discussed: an emergency liquidity reserve. A portfolio can weather a 50% drawdown if the investor separately maintains 6 to 12 months of living expenses in cash. Without this cushion, an unexpected event (job loss, surprise expense) can force a sale at the worst moment. Capital preservation begins with sound cash management.

What this means for your wealth

Drawdown isn't a technical detail reserved for professional traders. It's a measure of portfolio stress. Ignoring this metric is like piloting your portfolio without a dashboard, hoping the road stays straight. But it never does.

Before investing in a volatile asset like Bitcoin or altcoins, ask yourself three simple questions: what's the historical maximum drawdown for this asset? Am I ready to endure it without selling? Can my overall portfolio absorb it without compromising my life goals?

If the answer to any of these questions is no, then reduce your exposure. There's no glory in holding a portfolio that keeps you awake at night. There's no wisdom in maximizing theoretical returns if it translates to panic selling at -60%.

Wealth management, whether or not it includes crypto-assets, rests on balance: seeking returns, yes, but within a risk framework you control, understand, and can sustain over the long term. Drawdown is the compass showing whether you're still on the right path.

Your wealth deserves better than a basic savings account. I show you the way, backed by numbers.