On January 24, 2025, the U.S. Department of the Treasury published a regulatory proposal that could fundamentally reshape the role of stablecoin issuers. Going forward, Circle, Tether, and their competitors will be required to actively monitor suspicious transactions and report any potentially illicit activity to authorities. In other words, stablecoin issuers would be subject to the same compliance obligations as traditional banking institutions.

This development is far from trivial. It marks a paradigm shift in how American regulators approach digital assets: stablecoins are no longer viewed as simple technical tokens, but as full-fledged monetary instruments requiring surveillance equivalent to that of standard bank accounts.

For European players familiar with the MiCA framework, this American approach to stablecoin regulation raises a central question: how far should the responsibility of issuers extend in the fight against money laundering and terrorist financing?

Banking obligations applied to stablecoins: what the U.S. Treasury proposes

The proposal from the Financial Crimes Enforcement Network (FinCEN), the Treasury agency responsible for combating financial crime, imposes specific obligations on stablecoin issuers derived from the Bank Secrecy Act, American anti-money laundering legislation in effect since 1970.

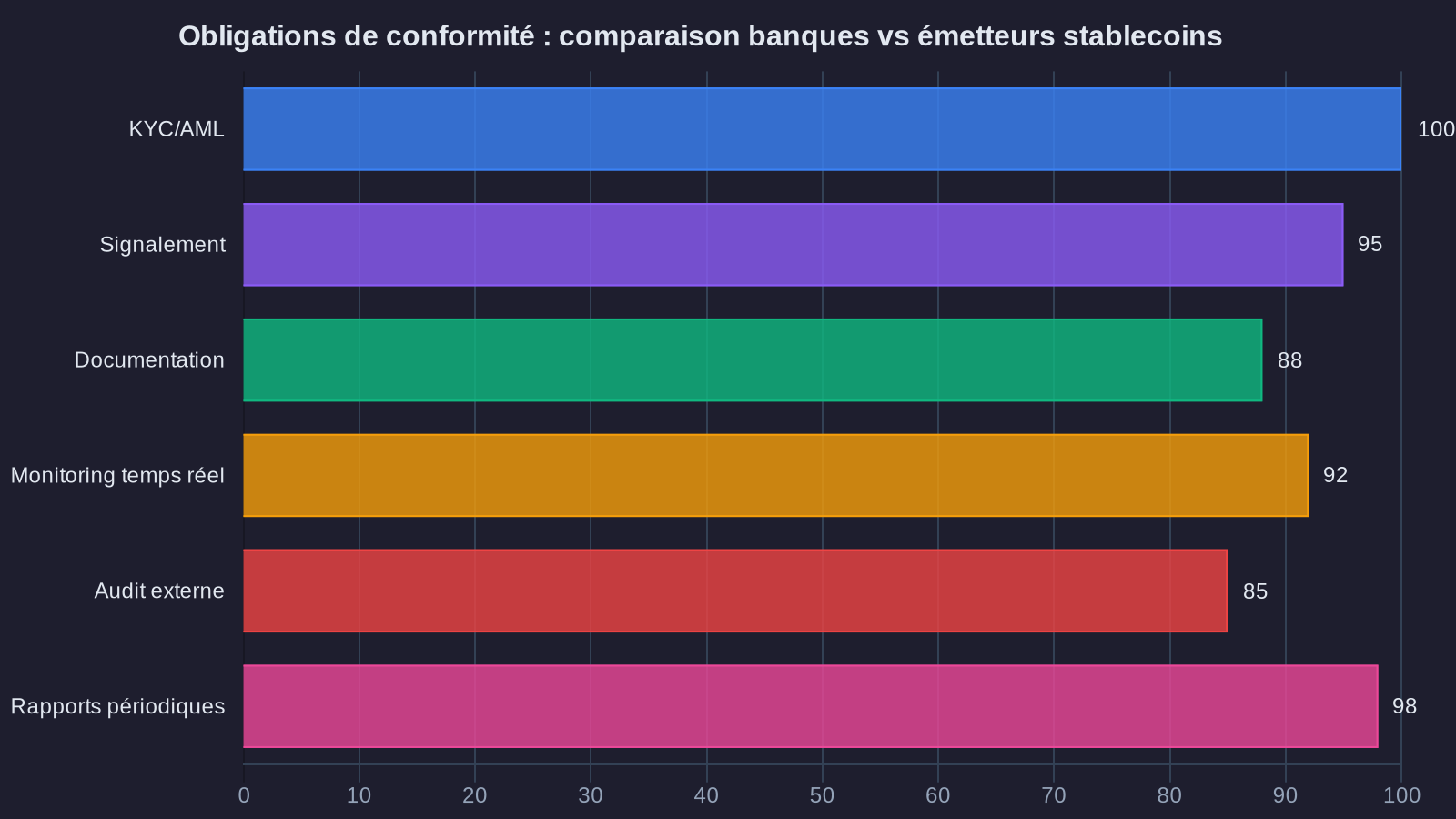

Specifically, issuers will need to implement a comprehensive AML compliance program for crypto that includes three mandatory pillars. First, the collection of user information when stablecoins are issued or redeemed. This is not merely basic identity verification, but due diligence comparable to what's required when opening a standard bank account: identification documents, proof of address, proof of funds origin for significant amounts.

Second, continuous real-time transaction monitoring. Issuers will need to analyze stablecoin flows to detect suspicious patterns: transaction splitting to evade reporting thresholds, repeated movements to high-risk jurisdictions, abnormal volumes on a given account. Exactly as a bank's compliance team would do.

Finally, mandatory reporting to authorities. Any transaction deemed suspicious must be subject to a Suspicious Activity Report (SAR) transmitted to FinCEN. These reports feed into financial intelligence databases and can trigger investigations. We're far from a simple technical infrastructure role: issuers become de facto active auxiliaries in financial surveillance.

A decentralized infrastructure facing centralized obligations: the technical challenge

The most complex aspect of this regulation stems from the very nature of blockchain. Stablecoins like USDC or USDT circulate on public, permissionless blockchains: Ethereum, Solana, Polygon. Once issued, a stablecoin can be transferred from wallet to wallet without the issuer's intervention. How can you effectively monitor what's beyond your direct control?

Issuers argue that they really only see two moments: initial issuance, when a user buys stablecoin in exchange for dollars, and final redemption, when they request the reverse conversion. In between, the stablecoin can pass through hundreds of intermediate addresses, be exchanged on decentralized platforms, transit through smart contracts or cross-chain bridges. All of this activity occurs without any centralized entity having the slightest control.

The industry contends that imposing continuous monitoring would be equivalent to asking the European Central Bank to monitor every physical euro transaction conducted in the eurozone. The analogy has its limits, but it well illustrates the technical challenge: stablecoins are designed to be freely transferable, like digital banknotes.

Some players are nonetheless considering technical solutions. Blockchain analytics tools, developed by companies like Chainalysis or Elliptic, enable real-time tracking of stablecoin flows and identification of addresses associated with known illicit activities. These tools could theoretically be integrated into issuers' compliance systems. But this assumes generalized monitoring of all blockchain transactions, which immediately raises privacy and decentralization concerns.

The MiCA precedent and transatlantic divergences in stablecoin regulation

In Europe, the MiCA regulation, which has been progressively coming into force since 2024, already imposes strict obligations on stablecoin issuers. Article 67 of MiCA requires, notably, a minimum capital of 350,000 euros, a reserve of liquid assets corresponding to 100% of stablecoins in circulation, and compliance with anti-money laundering rules defined by the AMLD6 directive.

The fundamental difference with the American approach lies in the scope of surveillance. MiCA requires issuers to verify the identity of their direct customers and monitor issuance and redemption operations. But the European regulation does not go so far as to require active monitoring of all secondary blockchain transactions. The responsibility for this surveillance rests instead with exchanges and crypto-asset service providers (PSAN), who are themselves subject to strict KYC/AML obligations.

Concretely, if you buy USDC on a regulated French platform, that platform verifies your identity. If you then transfer that USDC to your personal wallet, then to a DeFi platform, the issuer has no knowledge of it. Only the originating platform can potentially detect an anomaly at the time of the initial withdrawal.

The American approach goes further by asking issuers themselves to monitor the entire transaction chain. It's a difference in philosophy: Europeans favor distributed surveillance among multiple regulated actors, while Americans want to concentrate this responsibility on the issuer itself.

Stakes for investors and professional users

Should this regulation enter into force, the consequences for stablecoin users will be tangible. First, expect strengthened KYC procedures when buying or redeeming stablecoins. Issuers will need to collect more information, verify the source of funds for significant amounts, and potentially refuse certain transactions deemed risky.

Next, some activities that are common today could become more complex. The use of stablecoins via non-custodial wallets (where you hold your own private keys) could face close scrutiny. Transfers to decentralized platforms or DeFi protocols could trigger alerts, not because they're illegal, but because they present an increased money laundering risk according to authorities' criteria.

For businesses using stablecoins as a means of international payment or cash management, this also means increased traceability. Every fund movement could be analyzed and potentially reported if amounts or counterparties match risk criteria. Exactly like a SWIFT transfer, with the difference that blockchain offers complete transparency of flows.

Another likely consequence: market consolidation. Only issuers capable of massive investment in compliance infrastructure will be able to continue operating on the American market. This will mechanically favor already-established players like Circle and Tether, which have the necessary resources, at the expense of newcomers.

Between investor protection and over-regulation risk

This Treasury proposal comes in a particular political context. The Trump administration, back in power as of January 2025, has shown an ambivalent stance on digital assets: on one hand, a desire to foster innovation and American competitiveness against China and Europe; on the other, persistent mistrust of illicit uses and strong Congressional pressure for stricter regulation.

Supporters of this regulation, notably within FinCEN and the Department of Justice, believe it's essential to prevent large-scale money laundering. Stablecoins currently represent over $150 billion in market capitalization and are used daily for millions of transactions. Without adequate surveillance, they could become a preferred vehicle for circumventing international sanctions or financing criminal activities.

Opponents, primarily from the crypto industry and certain libertarian circles, denounce a security drift that would distort the very essence of digital assets. Imposing the same obligations on stablecoin issuers as on banks would amount to eliminating any comparative advantage: high compliance costs, extended processing times, and above all, loss of the technological neutrality that is blockchain's strength.

The debate remains open, and the public consultation period launched by FinCEN will likely refine certain aspects of the proposal. But one thing is certain: the era of unregulated stablecoins is coming to an end, in the United States as elsewhere.

Key takeaway

If you use stablecoins in a professional capacity or for significant amounts, prepare now for a more restrictive regulatory environment. Verify that your internal procedures for documenting financial flows are up to date. Systematically keep supporting documentation of fund sources when you buy or redeem stablecoins.

If you operate from Europe, ensure that your stablecoin issuer has proper MiCA authorization or equivalent. Unregulated issuers risk being quickly pushed out of the market, and you could lose access to your funds in case of sudden closure.

Finally, keep in mind that regulatory compliance is not optional: it has become a sine qua non condition for operating sustainably in the crypto ecosystem. Players who anticipate these developments will be better positioned than those who passively wait to be forced to adapt.

For any questions regarding the tax treatment of your stablecoin transactions or your disclosure obligations, consult your accountant or specialized adviser without fail. Regulatory and tax stakes are now too complex to be managed without professional support.

```