Ledger is preparing for its US public offering. The French hardware wallet manufacturer for crypto-assets is targeting a $4 billion valuation during its IPO, scheduled for 2026. This announcement comes after a strategic recruitment: several executives from Circle (the USDC issuer) have joined the team to support this American expansion.

The information was confirmed on March 17, 2026 by sources close to the matter. Ledger, which now serves over 7 million users worldwide, is entering a new league. The question is no longer whether the company can grow, but how it plans to defend its position against intensifying competition in the physical wallet market.

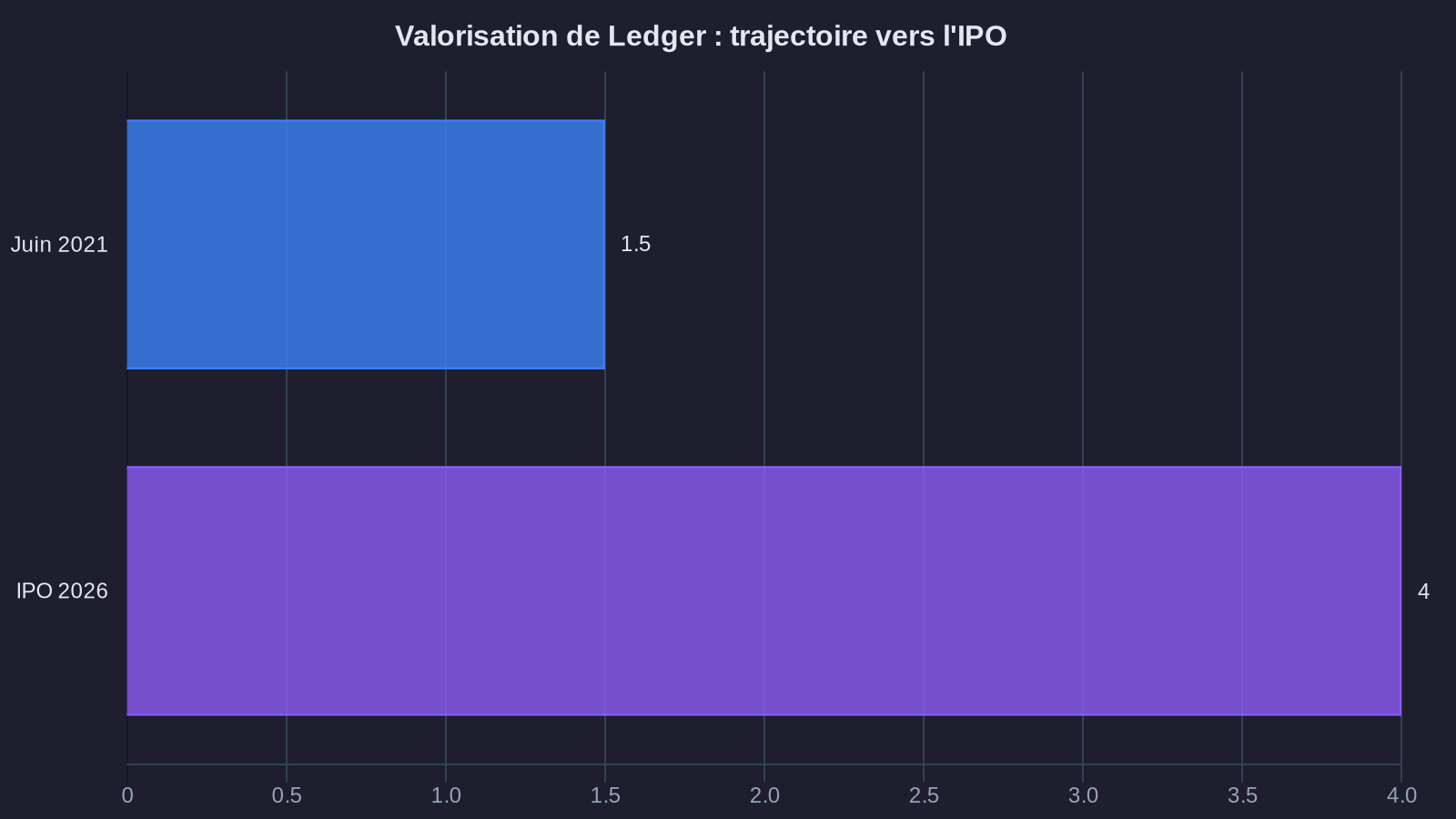

Timing an IPO in the middle of a bull cycle

Ledger is choosing a strategic moment for its IPO. Bitcoin is trading at $118,400 on March 18, 2026, up 12% over seven days. The global crypto-asset market has once again exceeded $4 trillion in capitalization. Macroeconomic conditions favor IPOs from crypto players: Coinbase sports a $68 billion valuation, up 180% since January 2025.

Ledger's last fundraising round dates back to June 2021 at a $1.5 billion valuation. By targeting $4 billion for the IPO, the company is betting on a 2.7x increase in value over five years. This multiple remains conservative compared to industry standards: Trezor, its Czech competitor, was valued at $2.2 billion during private discussions in December 2025.

Growth figures justify this ambition. Ledger posted €420 million in revenue in 2025, compared to €290 million in 2024. Gross margin reaches 68%, a level comparable to software publishers. Operating profitability has been confirmed since Q3 2024.

Circle recruitment: a clear institutional strategy

The recruitment of three Circle executives between January and March 2026 is no coincidence. Sarah Chen, former VP of Compliance at Circle, is taking the lead of Ledger's regulatory affairs. Michael Torres, ex-head of institutional partnerships, now leads B2B development. Finally, David Okonkwo joins as Chief Financial Officer, tasked with preparing the IPO.

These arrivals signal a clear strategic pivot. Ledger is no longer simply selling physical wallets to consumers. The company wants to capture the institutional market—family offices, asset managers, and enterprises that internalize custody of their crypto-assets. Circle, which manages over $40 billion in USDC circulation, knows this segment better than anyone.

Products are evolving accordingly. Ledger launched "Ledger Enterprise" in February 2026, a multi-signature custody solution for institutions. The system allows managing up to 500 wallets with customized approval rules. Pricing: $15,000 per year for the base license, plus 0.1% of assets under management beyond $50 million. Three clients have already signed, including a Swiss asset manager managing $2.3 billion in crypto.

The American market as conquering ground

Why a US IPO rather than Paris? The answer boils down to three numbers. The American market represents 42% of Ledger's sales in 2025, versus 28% for Europe and 30% for the rest of the world. American investors value crypto companies on average 40% higher than their European counterparts at equivalent revenue multiples. Finally, a Nasdaq listing facilitates future acquisitions paid in stock.

Ledger is laying the groundwork. The company opened a New York office in October 2025, with 35 employees dedicated to institutional sales and regulatory support. It obtained MSB (Money Services Business) registration with FinCEN in January 2026, mandatory to operate in most US states. The process took 14 months and mobilized two specialized law firms.

The expansion strategy doesn't stop there. Ledger is currently negotiating with three American banks to integrate its custody solutions into their crypto offerings. These discussions have progressed since the SEC clarified in November 2025 the status of non-custodial custody service providers. Banks can now offer assisted self-custody without risking reclassification as a regulated custodian.

Competition organizing against the hardware wallet leader

Trezor isn't standing still. The Czech manufacturer launched the Trezor Safe 5 in January 2026, a wallet with a color touchscreen and NFC connectivity. Price: €249, compared to €279 for the equivalent Ledger Stax. Safe 5 sales reached 180,000 units in two months, a record for Trezor. The company plans a $150 million Series B fundraising in Q2 2026.

Tangem takes a different approach. This Swiss manufacturer sells wallets in the form of NFC cards, without screen or battery. The system bets on simplicity: three identical cards form a backup set, sold for €59 per set. Tangem sold 2.1 million sets in 2025, primarily in Asia. Its post-money valuation reached $800 million in December 2025.

The threat also comes from smartphones. Samsung integrated a dedicated security module for crypto-assets into its Galaxy S26 lineup in February 2026. Apple is reportedly working on a similar feature for the iPhone 17, according to patents filed in January. These tech giants could democratize self-custody beyond the niche market of crypto enthusiasts.

Ledger nonetheless retains structural advantages. The company holds 127 patents on secure electronic signature technologies. Its proprietary operating system, BOLOS, runs on a chip certified EAL5+, the highest level of civilian security. No competitor has managed to match this certification. Penetration tests conducted by independent researchers in 2025 revealed no remotely exploitable critical vulnerabilities.

Risks of becoming a public company

An IPO changes everything. Ledger will have to publish quarterly results and justify its strategic choices each quarter to shareholders expecting growth. Margin pressure will intensify. The crypto-asset cycle remains volatile: what happens if Bitcoin drops to $60,000 and wallet sales collapse 40%, like in 2022?

The company anticipates this scenario. It's diversifying revenue beyond hardware sales. Ledger Live, the portfolio management application, now generates commissions on exchanges executed through integrated partners (Changelly, 1inch). These recurring revenues reached €78 million in 2025, representing 18.6% of total revenue. 2027 target: exceed 30% of revenue through software services.

Regulatory risk also looms. The European Union is finalizing MiCA II regulation, which could impose reporting obligations on wallet manufacturers. Estimated compliance cost: between €5 and €12 million per year depending on scenarios. In the United States, several states are discussing specific licenses for non-custodial custody solution providers. The American regulatory patchwork complicates national expansion.

What ForYield thinks about it

Ledger's IPO at $4 billion validates the maturity of the crypto infrastructure sector. For our clients, this confirms a trend observed over the past 18 months: professional custody solutions become essential once invested amounts exceed €500,000. We systematically recommend using certified hardware wallets for long-term storage and optimized tax management.

Ledger's geographic diversification (42% USA, 28% Europe) also reflects the evolution of our allocations. Our strategies now predominantly integrate American protocols (Ethereum, Solana, Avalanche) that benefit from superior liquidity and faster institutional adoption. Ledger's strengthened presence in the American market will facilitate integrating our custody flows with local platforms.

The arrival of ex-Circle executives is a positive signal. Circle masters the institutional compliance requirements we know well: asset segregation, complete audit trails, daily reconciliations. If Ledger transposes these standards to hardware custody, it will elevate the overall security level of the industry. We're closely monitoring Ledger Enterprise deployment, whose multi-signature functionalities match the needs of our family office structures.

The main risk remains dependency on market cycles. A prolonged crash would immediately affect transaction volumes and therefore Ledger's service revenues. This is why we prioritize, in our recommendations, crypto companies with predictable recurring revenues rather than those exposed solely to spot volumes. Ledger's diversification trajectory (18.6% recurring revenue in 2025, 30% target in 2027) is heading in the right direction, but remains insufficient to completely smooth cyclical exposure, as illustrated by the progressive adoption of crypto-assets in American retirement savings vehicles.