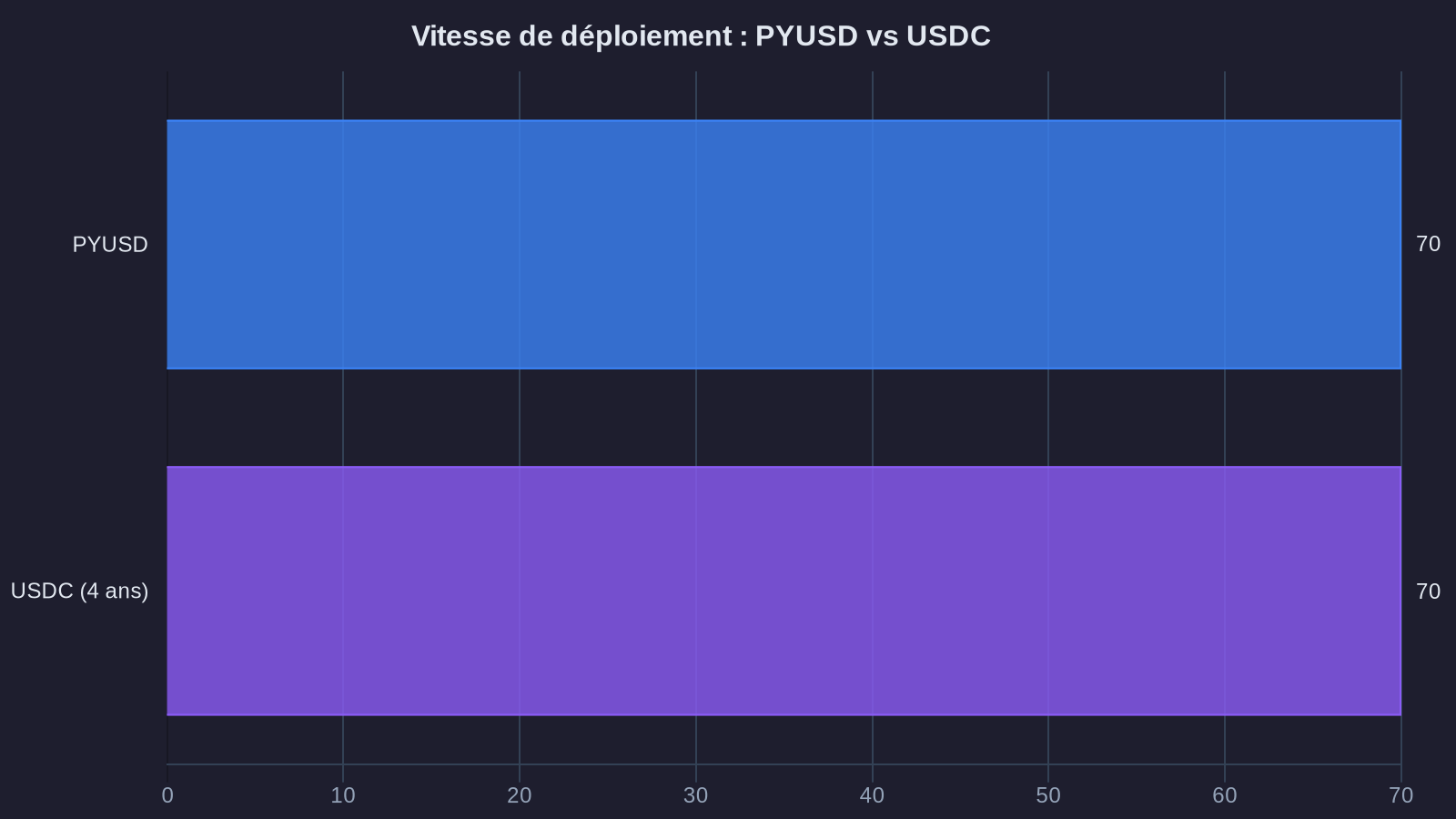

On March 17, 2025, PayPal announced the rollout of its PYUSD stablecoin across 70 markets simultaneously. An expansion at this scale is unprecedented for a crypto asset issued by a private company. For context: Circle's USDC took 4 years to reach equivalent coverage. PYUSD is doing it in mere months, marking a turning point in the global adoption of blockchain payments.

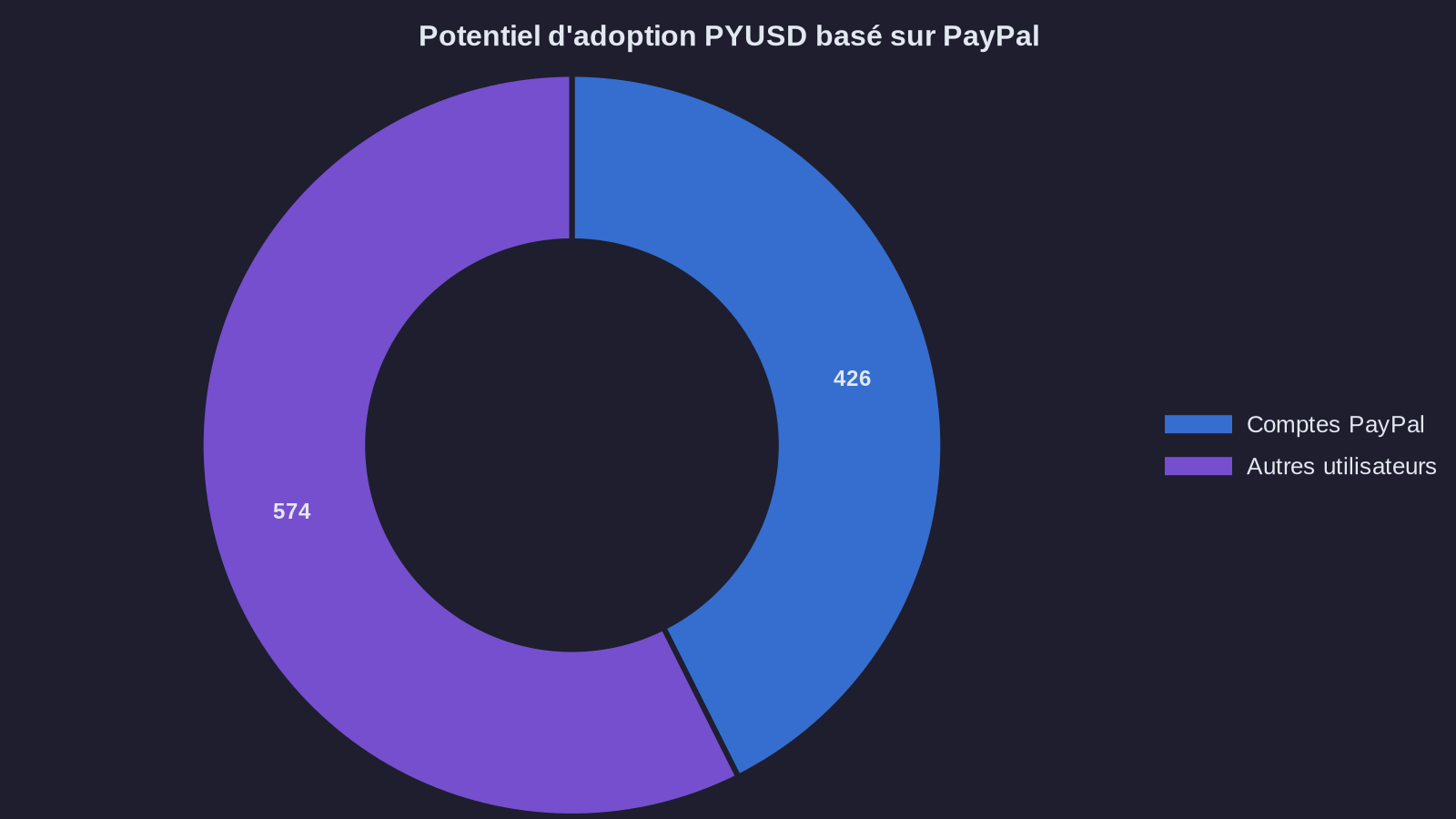

What makes this announcement strategically significant is the user base. PayPal has 426 million active accounts worldwide. Even if only a fraction adopts PYUSD, we're talking about a potential of tens of millions of users exposed to a stablecoin within a few quarters. No native crypto player has this kind of commercial firepower.

The question is no longer whether stablecoins will go mainstream. It's who will control this monetary infrastructure: traditional payments giants or decentralized protocols.

An adoption strategy different from native crypto players

PayPal isn't trying to convince crypto early adopters. The company is leveraging an existing user base already comfortable with its interface, and integrating PYUSD directly into standard payment flows. No external wallet needed, no seed phrases to manage, no incomprehensible gas fees. The average user doesn't even know they're using a stablecoin.

This approach starkly contrasts with USDC or USDT, which developed through exchanges and DeFi protocols. These stablecoins conquered the crypto market, but struggle to break out of that ecosystem. PYUSD is targeting e-commerce, international transfers, and peer-to-peer payments directly—use cases where PayPal already dominates.

The numbers speak for themselves: since its launch in August 2023, PYUSD shows a market cap of $1.2 billion as of March 18, 2025 (+340% over 6 months). That's still far from USDC's $38 billion or USDT's $140 billion, but the trajectory is clear. More importantly, PYUSD records a usage rate in real transactions above the stablecoin average: 68% of circulating supply has been moved at least once in the last 30 days, compared to 42% for USDC.

PayPal also has a regulatory advantage. The company is already licensed in most jurisdictions where it operates. It doesn't need to negotiate specific permissions to issue PYUSD, unlike Circle which must justify each new expansion to local regulators. This existing compliance infrastructure enables accelerated deployment.

The 70 markets: Geography and strategic implications

PayPal has prioritized Europe, Asia-Pacific, and Latin America. Markets where cross-border transfers are expensive (averaging between 5% and 12%) and where unbanked and underbanked populations represent enormous potential. In these regions, PYUSD isn't just a crypto gadget: it's a viable alternative to traditional banking channels.

Take the US/Philippines corridor, one of the world's most active for remittances ($35 billion in 2024). A standard transfer via Western Union or MoneyGram costs an average of 8.2% in fees. With PYUSD, PayPal is announcing capped fees of 1.5% for dollar/peso conversions, with settlement in under 10 minutes. If this model works, it destabilizes an entire sector.

Europe is equally strategic. With the gradual implementation of the MiCA regulation (Markets in Crypto-Assets), stablecoins must meet strict requirements regarding reserves, audit, and transparency. PayPal has anticipated this regulation and structures PYUSD to be compliant from day one. In contrast, Tether (USDT) faces growing uncertainties around MiCA compliance, opening an opportunity for PYUSD with European users seeking a regulated stablecoin.

In Asia, the strategy is more nuanced. PayPal remains marginal in countries like China or India, where Alipay, WeChat Pay, and UPI dominate. But in secondary markets (Vietnam, Thailand, Malaysia), where PayPal already has an established presence through e-commerce, PYUSD can establish itself as the reference stablecoin for international payments.

The challenge for decentralized stablecoins

PayPal's offensive raises an existential question for decentralized protocols: how do you compete against infrastructure that combines financial might, regulatory compliance, and massive user base?

Algorithmic or decentralized stablecoins (DAI, FRAX, etc.) rely on complex collateralization mechanisms and community governance. They offer censorship resistance and neutrality that PYUSD can never guarantee. But this decentralization comes at a cost: residual volatility, fragmented liquidity, and user experience still too technical for mainstream audiences.

DAI, MakerDAO's decentralized stablecoin, has maintained a stable market cap around $5 billion since 2023. It hasn't captured the explosive growth of the stablecoin market, which doubled over the same period. The reason: DAI remains confined to advanced DeFi users, while newcomers are turning to USDC, USDT, or now PYUSD.

The other issue is reserve centralization. PYUSD is backed by US Treasury bonds and bank deposits, audited monthly by Paxos. But PayPal retains full control over issuance, account freezing, and sanctions compliance. A PYUSD user implicitly accepts that a private company can block their funds at any time. That's acceptable for e-commerce payments, far less so for value storage or sensitive use cases.

Decentralized protocols must therefore choose their battle. Either they pursue mainstream adoption and accept compromises on decentralization (this is Circle's path with USDC, increasingly moving toward a semi-centralized model). Or they embrace their niche positioning as censorship-resistant financial infrastructure for specific use cases: protection against inflation in countries with unstable currencies, sanctions evasion, financing sensitive projects.

What ForYield thinks

PYUSD's expansion across 70 markets sends a clear signal: stablecoins are no longer a crypto niche product, but a monetary infrastructure undergoing standardization. For the portfolios we manage at ForYield, this implies a reassessment of exposures.

We're monitoring three direct impacts. First, liquidity: increased stablecoin supply strengthens market depth in crypto and facilitates arbitrage between yield farming protocols. Second, regulation: PayPal's entry legitimizes stablecoins with regulators, which could accelerate approval of new derivative products or ETF indexed on stablecoin baskets. Third, competition: if PYUSD captures significant share of trading volumes currently dominated by USDT, this could weaken Tether's position and create arbitrage opportunities between stablecoins.

We've adjusted our allocations accordingly. Some positions previously concentrated in USDC have been diversified toward PYUSD, particularly for strategies exploiting yield spreads between Ethereum and Solana protocols (PYUSD is deployed on both networks). We remain cautious on Tether, whose regulatory compliance remains unclear in Europe post-MiCA.

This week's action: if you use PayPal for international payments, test PYUSD on a real transfer. Compare fees and timing with your usual method. Real-world data beats marketing announcements.