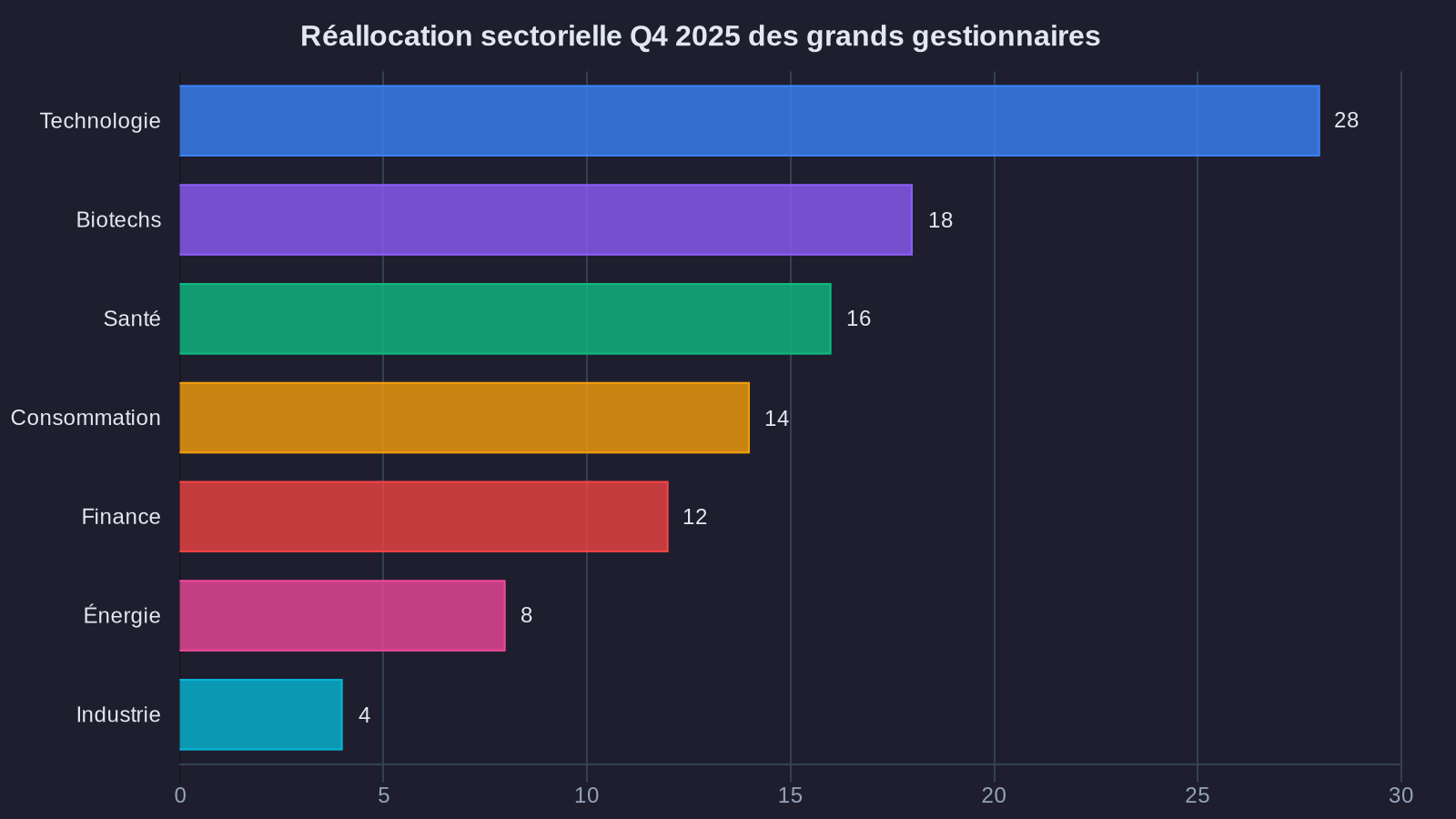

You built your asset allocation at the start of the year by overweighting financial stocks. An analysis of public positions held by the largest American asset managers in Q4 2025 reveals a troubling reality: they're making a massive retreat. Two Sigma, Wellington Management, and T. Rowe Price, which collectively manage over $2.5 trillion in assets, have all executed a major portfolio sector rotation in 2025. They're trimming financial stocks, strengthening technology holdings, and returning to biotech.

This convergence is not insignificant. When managers equipped with the best quantitative analysis tools and the most robust research teams simultaneously adjust their sector exposure, it means a fundamental macroeconomic variable has shifted. The question is no longer whether you should adjust your strategic allocation, but how to do it without destroying value in the process.

What the Q4 13F filings reveal

Form 13F filings require American asset managers to disclose their quarterly positions. This enforced transparency provides a precise snapshot of institutional capital flows. In Q4 2025, three clear trends emerge from the filings of Two Sigma, Wellington, and T. Rowe Price.

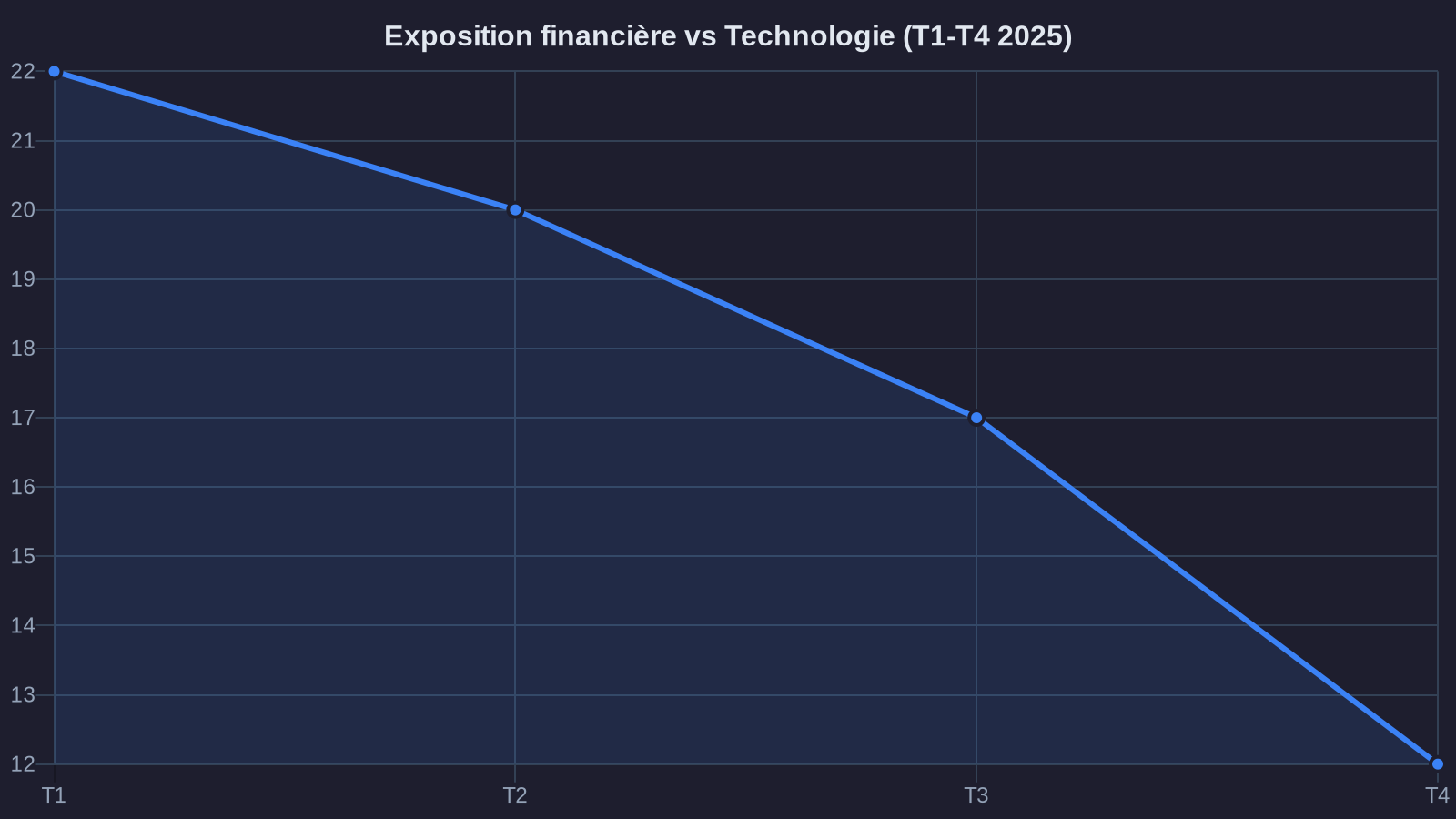

First observation: trimming positions in major U.S. banks. Two Sigma reduced its JPMorgan Chase exposure by 18%, Wellington cut its Bank of America stake by 22%, while T. Rowe Price trimmed Wells Fargo by 15%. To recap, these three institutions had enjoyed a +28% average rally between January and September 2025, driven by hopes for a steeper yield curve and credit recovery.

Second finding: a massive return to growth-oriented technology stocks. Wellington increased its Nvidia position by 34%, T. Rowe Price strengthened Microsoft by 19%, and Two Sigma boosted exposure to names like ServiceNow and Salesforce. These moves came after a -12% technical correction on the Nasdaq between August and October 2025, which had created attractive entry points on solid fundamentals.

Third element: selective rehabilitation of biotech. Wellington, historically present in this sector, more than doubled its Vertex Pharmaceuticals position. T. Rowe Price initiated a significant stake in Moderna after 18 months of absence. Two Sigma, more tactical in nature, repositioned into sector biotech ETFs after liquidating these positions in early 2024.

The macroeconomic reasons behind this 2025 sector rotation

This strategic convergence is explained by three macroeconomic factors that materialized between September and November 2025.

The first factor concerns the evolution of the yield curve. Contrary to first-half expectations, the anticipated steepening never materialized. The 2-year to 10-year spread remained stuck around 15 basis points, well below the 60-80 basis points that would have allowed banks to significantly widen net interest margins. For an institution like JPMorgan, every 10 basis point move on this spread represents roughly $800 million in annual net interest income. The absence of structural steepening therefore mechanically limits the potential for net banking income growth in 2026.

The second factor lies in the unexpected resilience of AI infrastructure demand. Capital expenditure (capex) from hyperscalers—Microsoft, Google, Amazon, Meta—for 2026 is collectively estimated at $240 billion, representing +18% versus 2025. This dynamic directly supports valuations for Nvidia, ASML, Broadcom, and the entire advanced semiconductor value chain. Quantitative managers like Two Sigma detected this persistence in order data and management guidance as early as September.

The third factor concerns biotech. FDA approvals accelerated in the second half of 2025, with 23 new molecules validated versus 16 over the same period in 2024. Several gene therapies and rare disease treatments received market authorization, creating 5-7 year revenue visibility for companies like Vertex, BioMarin, and Sarepta. This favorable regulatory dynamic, coupled with valuations that had been compressed in 2023-2024, reopened an opportunity window that Wellington, the sector's historical specialist, didn't miss.

Practical implications for your strategic asset allocation

You likely hold direct banking positions or exposure through sector ETFs. The question isn't whether to brutally liquidate these holdings—major U.S. banks remain solid enterprises with returns on equity of 12-15%—but rather to progressively rebalance your exposure.

Let's take a concrete example. You have a €200,000 portfolio with an initial 15% allocation to financials (€30,000), 40% to tech broadly (€80,000), 10% to healthcare/biotech (€20,000), and 35% diversified elsewhere. The moves observed among major managers suggest a target allocation closer to: 10% financials, 45% tech, 15% healthcare/biotech.

Practically, this would mean reducing your financial exposure by €10,000, strengthening tech by €10,000 and biotech by €10,000. But be careful: this rotation shouldn't happen all at once. Transaction fees (0.2 to 0.5% per trade depending on your broker), market impact on significant positions, and especially the tax implications of unrealized gains must be factored into your calculation.

On your profitable financial positions, a flat 30% tax applies. If your JPMorgan position shows +€4,500 in unrealized gains on €15,000 invested, selling completely will trigger €1,350 in immediate taxes. It may be preferable to trim gradually, three or four times over six months, to smooth out the tax impact and benefit from potential technical bounces that would reduce taxable gains.

For the tech portion, prioritize entry points after 5-8% corrections, which are frequent on these volatile stocks. A limit order placed 7% below the current price on Nvidia or Microsoft will capture these windows without requiring daily monitoring. For biotech, an index-based approach through a MSCI World Healthcare tech biotech ETF or Nasdaq Biotech is probably more prudent than direct stock-picking, unless you have genuine sector expertise.

Key points of caution before acting

This sector rotation observed among institutional investors is not a guarantee of future performance. It reflects a positioning at a specific point in time, based on information and models specific to them. Three elements of caution should temper your enthusiasm to replicate these moves.

First point: investment horizon. Two Sigma, a quantitative manager, operates with a tactical horizon of a few quarters. Wellington Management, with its long-term fundamental approach, reasons over 3-5 years. Your own investment horizon determines the relevance of these adjustments. If your goal is building retirement capital over 15 years, quarterly sector rotation has only marginal impact on your final returns. The consistency of contributions and discipline in maintaining strategic allocation matter infinitely more.

Second point: geographic concentration. These three managers operate essentially in the U.S. market. European sector dynamics differ. European banks, for example, haven't experienced the same rally as their American counterparts in 2025. BNP Paribas, Société Générale, and Unicredit show contained performance, with different challenges (commercial real estate exposure, Italian sovereign debt). Replicating a U.S. rotation on a European portfolio without adjustment would be a methodological error.

Third point: the opportunity cost of action. Every portfolio move incurs fees, demands analytical time, creates mental burden. If your current allocation is already well-balanced and diversified, the marginal gain from sector rotation may be less than the total cost (financial and psychological) of rebalancing. Informed inaction is sometimes the best strategy.

What this means for your wealth

The convergent moves by Two Sigma, Wellington, and T. Rowe Price in Q4 2025 signal a change in sector regime. The macroeconomic conditions supporting financials have run their course. In parallel, structural demand for AI infrastructure and biotech advances are creating identifiable new pockets of growth.

For your wealth, this doesn't justify a brutal overhaul of your allocation. However, if you're overweight in financials (beyond 15-18% of your equity exposure), a progressive trim over 6 to 9 months toward tech and biotech makes sense. Use regular contributions (monthly savings, rental income) to strengthen underweighted sectors without triggering taxes on existing positions.

Smart wealth management is never a race against time. It's a methodical, documented adjustment that accounts for your personal tax situation, your time horizon, and your risk tolerance. Institutional investors have the resources to pivot quickly. You have the advantage of being able to wait for the right entry point, without quarterly performance pressure. Use it.

Your wealth deserves better than a savings account. I'll show you the way, backed by the numbers.